Panera Bread 2005 Annual Report Download - page 32

Download and view the complete annual report

Please find page 32 of the 2005 Panera Bread annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

22 -

23

23 -

24

24 -

25

25 -

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

|

|

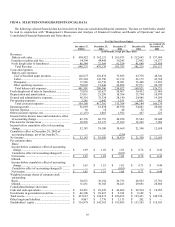

26

Valuation of Goodwill

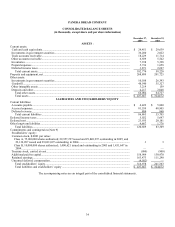

We record goodwill related to the excess of the purchase price over the fair value of net assets acquired. At December 27, 2005

and December 25, 2004, our goodwill balance was $48.5 million and $35.3 million, respectively. Annually, and whenever an event or

circumstance indicates it is more likely than not our goodwill has been impaired, management assesses the carrying value of our

recorded goodwill. We perform our impairment assessment by comparing discounted cash flows from acquired businesses with the

carrying value of the underlying net assets inclusive of goodwill. In performing this analysis, management considers such factors as

current results, trends, future prospects and other economic factors. No event has been identified indicating an impairment in the value

of our goodwill.

Self-Insurance

We are self-insured for a significant portion of our workers’ compensation, group health (beginning in 2005), and general, auto,

and property liability insurance for up to $0.5 million of individual claims, depending on the category of loss. We also purchase

aggregate stop-loss and/or layers of loss insurance in many categories of loss. At December 27, 2005 and December 25, 2004, self-

insurance reserves were $8.9 million and $3.5 million, respectively. We utilize third party actuarial experts’ estimates of expected

losses based on statistical analyses of historical industry data as well as our own estimates based on our actual historical data to

determine required self-insurance reserves. These assumptions are closely reviewed, monitored, and adjusted when warranted by

changing circumstances. Actual experience related to number of claims and cost per claim could be more or less favorable than

estimated resulting in expense reduction or increase.

Lease Obligation

We recognize rent expense on a straight-line basis over the reasonably assured lease period. Certain of our lease agreements

provide for scheduled rent increases during the lease terms or for rental payments commencing at a date other than the date of initial

occupancy. We include any rent escalations and construction and other rent holidays in our straight-line rent expense. In addition, we

record landlord allowances for normal tenant improvements as deferred rent, which is included in accrued expenses or deferred rent in

the consolidated balance sheets based on their short-term or long-term nature. These landlord allowances are amortized over the

reasonably assured lease term as a reduction of rent expense. Also, leasehold improvements are amortized using the straight-line

method over the shorter of their estimated useful lives or the related reasonably assured lease term. See Note 2 to the Consolidated

Financial Statements for further information on our accounting for leases.

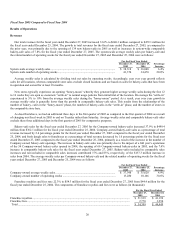

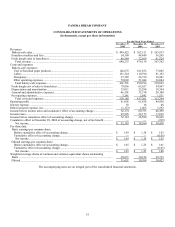

Liquidity and Capital Resources

Cash and cash equivalents were $24.5 million at December 27, 2005 compared with $29.6 million at December 25, 2004. Our

principal requirements for cash are capital expenditures for the development of new bakery-cafes, for maintaining or remodeling

existing bakery-cafes, for purchasing existing franchise-operated bakery-cafes, for developing, remodeling and maintaining fresh

dough facilities, and for enhancements of information systems and other infrastructure capital investments. For the fiscal year ended

December 27, 2005, we met our requirements for capital with cash from operations.

We had working capital of $15.9 million at December 27, 2005 and $2.5 million at December 25, 2004. The increase in working

capital from December 25, 2004 to December 27, 2005 resulted primarily from an increase in current investments in government

securities of $34.2 million, an increase in trade and other receivables of $7.9 million, and a decrease in accounts payable of $1.4

million partially offset by an increase in accrued expenses of $32.7 million. The increase in accrued expenses of $32.7 million was

primarily due to the following: $7.6 million increase in payroll and incentive compensation accruals, $6.1 million increase in capital

expenditures accrual, $5.5 million increase in unredeemed gift card accrual, $5.3 million increase in insurance accruals, which was

mainly driven by the change in our medical insurance coverage from fully insured prior to 2005 to self-insured in 2005, and $6.2

million increase in other accruals, which were mainly driven by our growth and the timing of payments at year end. We have

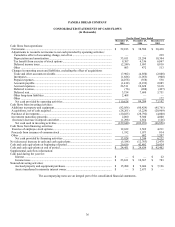

experienced no liquidity difficulties and have historically been able to finance our operations through internally generated cash flow.

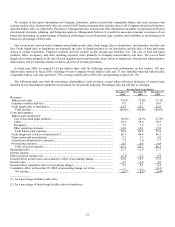

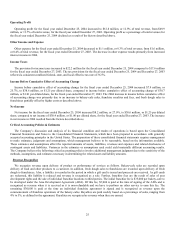

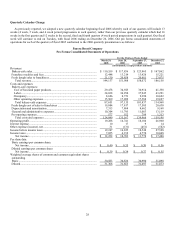

The components of our cash flow were as follows (in thousands):

For the Fiscal Year Ended

Cash provided by (used in):

December 27,

2005

December 25,

2004

December 27,

2003

Operating Activities............................................................................................................ $ 110,628 $ 84,284 $ 73,102

Investing Activities............................................................................................................. $ (129,640) $ (102,291) $ (66,856)

Financing Activities............................................................................................................ $ 13,824 $ 5,244 $ 6,232