Nordstrom 2002 Annual Report Download - page 35

Download and view the complete annual report

Please find page 35 of the 2002 Nordstrom annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

25 -

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

-

47

-

48

-

49

-

50

-

51

-

52

|

|

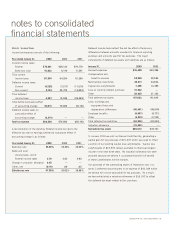

notes to consolidated

financial statements

NORDSTROM INC. AND SUBSIDIARIES 33

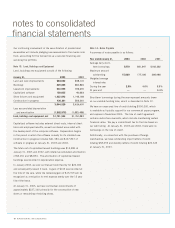

The following table illustrates the sensitivity in the fair market value

estimates of the retained interests given independent changes in

assumptions as of January 31, 2003:

+10% +20% -10% -20%

Gross Yield $1,207 $2,414 $(1,207) $(2,414)

Interest Expense

on Issued Classes (76) (152) 76 152

Card Holders Payment Rate (99) (296) 207 384

Charge Offs (531) (1,059) 533 1,069

Discount Rate (337) (673) 339 680

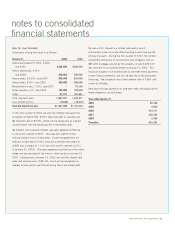

The following table summarizes certain income, expenses and cash

flows received from and paid to the master note trust.

Year ended January 31, 2003 2002 2001

Principal collections reinvested

in new receivables $824,715 $669,582 $485,422

Gains on sales of receivables 8,290 3,147 5,356

Income earned on

retained interests 10,786 6,711 9,035

Cash flows from retained assets:

Retained interests 28,100 11,916 10,050

Servicing fees 5,407 8,440 8,121

Interest income earned on the retained interests is included in

service charge income and other on the consolidated statements

of earnings.

The total principal balance of the VISA receivables was $323,101

and $258,075 as of January 31, 2003 and 2002. Gross credit

losses were $18,580 and $17,050 for the years ended January 31,

2003 and 2002, and receivables past due for more than 30 days

were $8,519 and $8,170 at January 31, 2003 and 2002.

The following table illustrates default projections using net credit

losses as a percentage of average outstanding receivables in

comparison to actual performance:

Year ended January 31, 2004 2003 2002

Original projection 6.16% 7.66% 5.99%

Actual N/A 6.59% 6.62%

Under the terms of the trust agreement, we may be required to

fund certain amounts upon the occurrence of specific events.

The securitization agreements set a maximum percentage of

receivables that can be associated with employee accounts.

As of January 31, 2003, this maximum was exceeded by $1,500.

It is possible that we may be required to repurchase these

receivables. Aside from this instance, we do not believe any

additional funding will be required.

Our continued involvement in the securitization of VISA receivables

will include recording gains/losses on sales in accordance with SFAS

No. 140 and recognizing income on retained assets as prescribed

by EITF 99-20 “Recognition of Interest Income and Impairment on

Purchased and Retained Beneficial Interests in Securitized Financial

Assets,” holding subordinated, non-subordinated and residual

interests in the trust, and servicing the portfolio.

Note 12: Receivable-backed Securities

In 2001, we issued $300 million of receivable-backed

securities supported by substantially all of our private label

credit card receivables. This transaction is accounted for as

a secured financing.

Total principal receivables of the securitized portfolio at

January 31, 2003 and 2002 were approximately $609,784

and $625,516, and receivables more than 30 days past due were

approximately $16,973 and $19,301. Net charged off receivables

for the years ending January 31, 2003 and 2002 were $29,555

and $28,134. The private label receivables also serve as collateral

for a variable funding facility with a limit of $200,000. Interest

on the facility varies based on the actual cost of commercial paper

plus specified fees. Nothing was outstanding on this facility at

January 31, 2003 or 2002.