Nike 2012 Annual Report Download - page 30

Download and view the complete annual report

Please find page 30 of the 2012 Nike annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

20 -

21

21 -

22

22 -

23

23 -

24

24 -

25

25 -

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

|

|

PART II

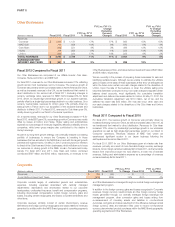

Managing transactional exposures

Transactional exposures are managed on a portfolio basis within our foreign

currency risk management program. We manage these exposures by taking

advantage of natural offsets and currency correlations that exist within the

portfolio and may also elect to use currency forward and option contracts to

hedge the remaining effect of exchange rate fluctuations on probable

forecasted future cash flows, including certain product cost exposures,

non-functional currency denominated external sales and other costs

described above. These are accounted for as cash flow hedges in

accordance with the accounting standards for derivatives and hedging,

except for hedges of the embedded derivatives component of the product

costs exposure as discussed below. As of May 31, 2012, there were

outstanding currency forward contracts with maturities up to 24 months. The

fair value of outstanding currency forward contracts at May 31, 2012 and

2011 was $183 million and $28 million in assets and $32 million and $136

million in liabilities, respectively. The effective portion of the changes in fair

value of these instruments is reported in other comprehensive income (“OCI”),

a component of shareholders’ equity, and reclassified into earnings in the

same financial statement line item and in the same period or periods during

which the related hedged transactions affect consolidated earnings. The

ineffective portion is immediately recognized in earnings as a component of

other expense (income), net. Ineffectiveness was not material for the years

ended May 31, 2012, 2011 and 2010.

Certain currency forward contracts used to manage the foreign exchange

exposure of non-functional currency denominated monetary assets and

liabilities subject to re-measurement and the embedded derivative contracts

discussed above are not formally designated as hedging instruments under

the accounting standards for derivatives and hedging. Accordingly, changes

in fair value of these instruments are immediately recognized in other expense

(income), net and are intended to offset the foreign currency impact of the

re-measurement of the related non-functional currency denominated asset or

liability or the embedded derivative contract being hedged. The fair value of

undesignated instruments was $55 million and $9 million in assets and $20

million and $17 million in liabilities at May 31, 2012 and 2011, respectively.

Refer to Note 6 — Fair Value Measurements and Note 16 – Risk Management

and Derivatives in the accompanying Notes to the Consolidated Financial

Statements for additional description of how the above financial instruments

are valued and recorded.

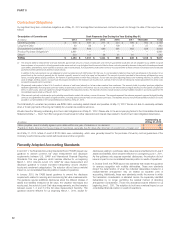

Translational exposures

Many of our foreign subsidiaries operate in functional currencies other than

the U.S. Dollar. Fluctuations in currency exchange rates create volatility in our

reported results as we are required to translate the balance sheets,

operational results and cash flows of these subsidiaries into U.S. Dollars for

consolidated reporting. The translation of foreign subsidiaries’ non-U.S. Dollar

denominated balance sheets into U.S. Dollars for consolidated reporting

results in a cumulative translation adjustment to OCI within shareholders’

equity. In the translation of our consolidated statements of income, a weaker

U.S. Dollar in relation to foreign functional currencies benefits our consolidated

earnings whereas a stronger U.S. Dollar reduces our consolidated earnings.

The impact of foreign exchange rate fluctuations on the translation of our

consolidated revenues was a benefit (detriment) of approximately $268 million

and $(28) million for the years ended May 31, 2012 and 2011, respectively.

The impact of foreign exchange rate fluctuations on the translation of our

income before income taxes was a benefit (detriment) of approximately $74

million and $(16) million for the years ended May 31, 2012 and 2011,

respectively.

Managing translational exposures

To minimize the impact of translating foreign currency denominated revenues

and expenses into U.S. Dollars for consolidated reporting, certain foreign

subsidiaries use excess cash to purchase U.S. Dollar denominated

available-for-sale investments. The variable future cash flows associated with

the purchase and subsequent sale of these U.S. Dollar denominated

securities at non-U.S. Dollar functional currency subsidiaries creates a foreign

currency exposure that qualifies for hedge accounting under the accounting

standards for derivatives and hedging. We utilize forward contracts and/or

options to mitigate the variability of the forecasted future purchases and sales

of these U.S. Dollar investments. The combination of the purchase and sale of

the U.S. Dollar investment and the hedging instrument has the effect of

partially offsetting the year-over-year foreign currency translation impact on

net earnings in the period the investments are sold. Hedges of

available-for-sale investments are accounted for as cash flow hedges. The fair

value of instruments used in this manner at May 31, 2012 and 2011 was $27

million and $1 million in assets and $3 million and $21 million in liabilities,

respectively. The effective portion of the changes in fair value of these

instruments is reported in OCI and reclassified into earnings in other expense

(income), net in the period during which the hedged available-for-sale

investment is sold and affects earnings. Any ineffective portion is immediately

recognized in earnings as a component of other expense (income), net. The

impact of ineffective hedges was not material for any period presented.

The combination of translation of foreign currency-denominated profits from

our international businesses and the year-over-year change in foreign

currency related gains and losses included in other expense (income), net had

an insignificant impact on our income before income taxes for the year ended

May 31, 2012 and had a unfavorable impact of approximately $33 million for

the year ended May 31, 2011.

Refer to Note 6 — Fair Value Measurements and Note 16 — Risk

Management and Derivatives in the accompanying Notes to the Consolidated

Financial Statements for additional description of how the above financial

instruments are valued and recorded.

Net investments in foreign subsidiaries

We are also exposed to the impact of foreign exchange fluctuations on our

investments in wholly-owned foreign subsidiaries denominated in a currency

other than the U.S. Dollar, which could adversely impact the U.S. Dollar value

of these investments and therefore the value of future repatriated earnings.

We hedge certain net investment positions in Euro-functional currency foreign

subsidiaries to mitigate the effects of foreign exchange fluctuations on these

net investments. In accordance with the accounting standards for derivatives

and hedging, the effective portion of the change in fair value of the forward

contracts designated as net investment hedges is recorded in the cumulative

translation adjustment component of accumulated other comprehensive

income. Any ineffective portion is immediately recognized in earnings as a

component of other expense (income), net. The impact of ineffective hedges

was not material for any period presented. To minimize credit risk, we have

structured these net investment hedges to be generally less than six months

in duration. Upon maturity, the hedges are settled based on the current fair

value of the forward contracts with the realized gain or loss remaining in OCI.

There were no outstanding net investment hedges as of May 31, 2012. At

May 31, 2011, the fair value was $23 million in liabilities. Cash flows from net

investment hedge settlements totaled $22 million and $(23) million for the

years ended May 31, 2012 and 2011, respectively.

30