Lumber Liquidators 2010 Annual Report Download - page 37

Download and view the complete annual report

Please find page 37 of the 2010 Lumber Liquidators annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

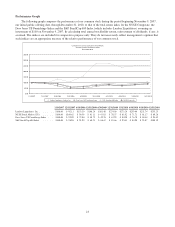

|

|

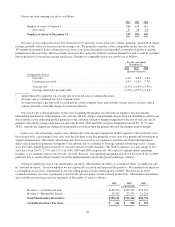

were received directly at the store, up from 16.4% in 2009. In the second half of 2010, these direct shipments

represented 23.8% of our unit purchases, up from 14.7% in the second half of 2009.

• Our efforts to expand and regionalize our assortment of Bellawood products resulted in 2010 per unit finishing

costs generally higher than those in 2009, primarily due to greater demand for products which are less efficient to

finish.

In aggregate, sales mix shifts were neutral to gross margin, including:

• Gross margin benefited from our continued efforts to broaden the assortment and strengthen the in-stock positions

of moldings and accessories, as well as laminates and certain engineered hardwoods, particularly the premium

products. These product lines generally carry a higher than average gross margin.

• Gross margin was adversely impacted by a strengthening in consumer demand for certain hardwoods, particularly

those at the entry level, which generally carry higher than average retail price points, but lower than average gross

margins.

• Liquidation deals, used as promotional opportunities to generate incremental traffic, have generally yielded lower

gross margins in 2010 than in 2009, and in each year, those gross margins have been lower than average.

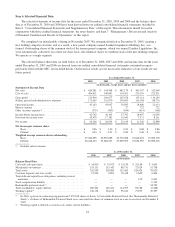

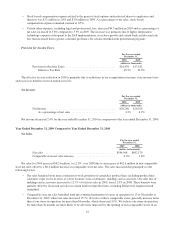

Operating Income and Operating Margin.

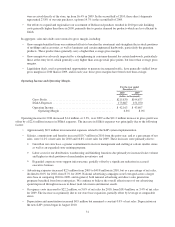

For the year ended

December 31,

2010 2009

(dollars in thousands)

Gross Profit .............................................. $215,830 $194,677

SG&A Expenses .......................................... 173,667 151,070

Operating Income ......................................... $ 42,163 $ 43,607

Operating Margin ..................................... 6.8% 8.0%

Operating income for 2010 decreased $1.4 million, or 3.3%, over 2009 as the $21.2 million increase in gross profit was

offset by a $22.6 million increase in SG&A expenses. The increase in SG&A expenses was principally due to the following

factors:

• Approximately $0.9 million in incremental expenses related to the SAP system implementation.

• Salaries, commissions and benefits increased $10.7 million in 2010 from the prior year, and as a percentage of net

sales, were 11.2% of net sales for 2010 and 10.8% of net sales for 2009. These increases were primarily due to:

OGrowth in our store base, a greater commitment to in-store management and staffing at certain smaller stores,

as well as an expanded store training program;

OLabor costs for our distribution, warehousing and finishing functions due primarily to increased sales volume

and higher in-stock positions of merchandise inventories; and

OExpanded corporate store-support infrastructure, partially offset by a significant reduction in accrued

executive bonuses.

• Advertising expenses increased $2.5 million from 2009 to $49.8 million in 2010, but as a percentage of net sales,

declined to 8.0% for 2010, from 8.7% for 2009. National advertising campaigns were leveraged across a larger

store base in comparing 2010 to 2009, and in general, both national advertising and direct sales generation

programs benefited from lower unit prices. We continue to believe the overall effectiveness of our advertising

spend improved through increases in direct mail, television and internet search.

• Occupancy costs increased to $22.2 million, or 3.6% of net sales for 2010, from $18.4 million, or 3.4% of net sales

for 2009. The increase was primarily due to our store base expansion, partially offset by leverage at comparable

stores.

• Depreciation and amortization increased $0.9 million but remained a constant 0.9% of net sales. Depreciation on

the new SAP system began in August 2010.

31