Columbia Sportswear 2003 Annual Report Download - page 46

Download and view the complete annual report

Please find page 46 of the 2003 Columbia Sportswear annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

|

|

COLUMBIA SPORTSWEAR COMPANY

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS—(Continued)

Selling, general and administrative expense:

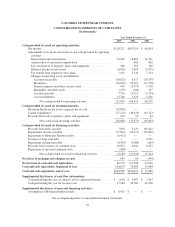

Selling, general and administrative expense consists of commissions, advertising, other selling costs,

personnel related costs, planning, receiving finished goods, warehousing, depreciation and other general

operating expenses.

Shipping and handling costs:

Shipping and handling fees billed to customers are recorded as revenue. The direct costs associated with

shipping goods to customers are recorded as cost of sales. Inventory planning, receiving and handling costs are

recorded as a component of selling, general, and administrative expenses. Handling costs were $22,461,000,

$16,798,000 and $16,341,000 for the years ended 2003, 2002 and 2001, respectively. Inventory planning and

receiving costs were $11,073,000, $9,979,000 and $8,781,000 for the years ended 2003, 2002 and 2001,

respectively.

Foreign currency translation:

The assets and liabilities of the Company’s foreign subsidiaries have been translated into U.S. dollars using

the exchange rates in effect at period end, and the net sales and expenses have been translated into U.S. dollars

using average exchange rates in effect during the period. The foreign currency translation adjustments are

included as a separate component of accumulated other comprehensive income (loss) in shareholders’ equity and

are not currently adjusted for income taxes as they relate to indefinite net investments in non-U.S. operations.

Fair value of financial instruments:

Based on borrowing rates currently available to the Company for bank loans with similar terms and

maturities, the fair value of the Company’s long-term debt approximates the carrying value. Furthermore, the

carrying value of all other financial instruments potentially subject to valuation risk (principally consisting of

cash and cash equivalents, accounts receivable and accounts payable) also approximate fair value because of

their short-term maturities.

Derivatives:

The Company accounts for derivatives in accordance with SFAS No. 133, “Accounting for Derivative

Instruments and Hedging Activities,” as amended by SFAS No. 137, “Accounting for Derivative Instruments and

Hedging Activities – Deferral of the Effective Date of SFAS No. 133” and SFAS No. 138, “Accounting for

Certain Derivative Instruments and Certain Hedging Activities – an Amendment of SFAS No. 133.”

Substantially all foreign currency derivatives entered into by the Company qualify for and are designated as

foreign-currency cash flow hedges, including those hedging foreign currency denominated firm commitments.

Changes in fair values of outstanding cash flow hedge derivatives that are highly effective are recorded in

other comprehensive income, until earnings are affected by the variability of cash flows of the hedged

transaction. In most cases amounts recorded in other comprehensive income will be released to earnings some

time after maturity of the related derivative. The consolidated statement of operations classification of effective

hedge results is the same as that of the underlying exposure. Results of hedges of product costs are recorded in

cost of sales when the underlying hedged transaction affects earnings. Unrealized derivative gains and losses

recorded in current and non-current assets and liabilities and amounts recorded in other comprehensive income

are non-cash items and therefore are taken into account in the preparation of the consolidated statement of cash

flows based on their respective balance sheet classifications.

41