Columbia Sportswear 2003 Annual Report Download - page 44

Download and view the complete annual report

Please find page 44 of the 2003 Columbia Sportswear annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

|

|

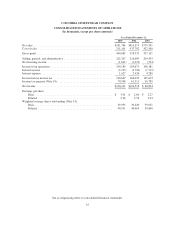

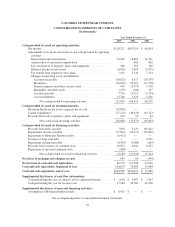

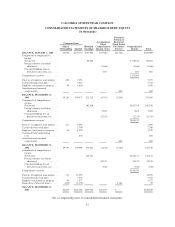

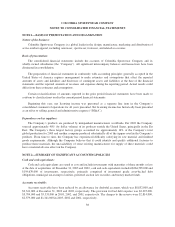

COLUMBIA SPORTSWEAR COMPANY

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS—(Continued)

Inventories:

Inventories are carried at the lower of cost or market. Cost is determined using the first-in, first-out method.

The Company periodically reviews its inventories for excess, close-out or slow moving items and makes

provisions as necessary to properly reflect inventory value.

Property, plant, and equipment:

Property, plant, and equipment are stated at cost. Depreciation of buildings, machinery and equipment,

furniture and fixtures and amortization of leasehold improvements is provided using the straight-line method

over the estimated useful lives of the assets. The principal estimated useful lives are: buildings, 30 years;

machinery and equipment, 3-10 years; and furniture and fixtures, 5-15 years. Leasehold improvements are

amortized over the lesser of the estimated useful life of the improvement or the remaining term of the underlying

lease.

The interest-carrying costs of capital assets under construction are capitalized based on the Company’s

weighted average borrowing rates. Capitalized interest was $226,000, $1,000,000 and $792,000 in 2003, 2002

and 2001, respectively.

Intangible assets:

The Company adopted Statement of Financial Accounting Standards (“SFAS”) No. 142, “Goodwill and

Other Intangible Assets,” effective January 1, 2002. In accordance with SFAS No. 142, certain intangible assets

with indefinite useful lives are no longer being amortized and are periodically evaluated for impairment. Certain

intangible assets that are determined to have finite lives continue to be amortized over their useful lives.

The following table summarizes the Company’s identifiable intangible assets balance (in thousands):

December 31, 2003 December 31, 2002

Carrying

Amount

Accumulated

Amortization

Carrying

Amount

Accumulated

Amortization

Intangible assets subject to amortization:

Patents .......................................... $ 1,200 $(63) $ — $—

Intangible assets not subject to amortization:

Trademarks and trade names ......................... $21,971 $6,971

Goodwill ........................................ 12,157 —

$34,128 $6,971

The increase in intangible assets from December 31, 2002 to December 31, 2003 is solely due to the

Mountain Hardwear acquisition (Note 3). Amortization expense for intangible assets subject to amortization is

estimated to be $84,000 in each of 2004, 2005, 2006, 2007 and 2008.

Impairment of long-lived and intangible assets:

In accordance with SFAS No. 142, goodwill and intangible assets with indefinite useful lives are no longer

amortized but instead are measured for impairment at least annually or when events indicate that an impairment

exists. The Company reviews and tests its goodwill and intangible assets for impairment in the fourth quarter of

each year and when events or changes in circumstances indicate that the carrying amount of such assets may be

impaired. Determination of fair value is based on estimated discounted future cash flows resulting from the use

39