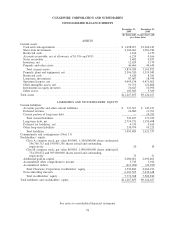

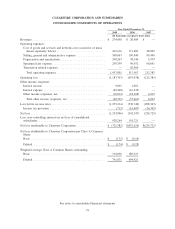

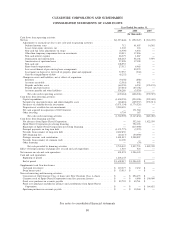

Clearwire 2009 Annual Report Download - page 82

Download and view the complete annual report

Please find page 82 of the 2009 Clearwire annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

86 -

87

87 -

88

88 -

89

89 -

90

90 -

91

91 -

92

92 -

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

|

|

I

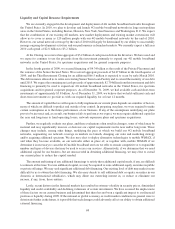

nterest R

a

te Ris

k

Our pr

i

mary

i

nterest rate r

i

s

ki

s assoc

i

ate

d

w

i

t

h

our

i

nvestment port

f

o

li

o. Our

i

nvestment port

f

o

li

o

i

spr

i

mar

il

y

c

omprised of mone

y

market mutual funds, United States

g

overnment and a

g

enc

y

issues and other debt securities.

Our

i

nvestment port

f

o

li

o

h

as a we

igh

te

d

avera

g

e matur

i

t

y

o

f

3 mont

h

san

d

a mar

k

et

yi

e

ld

o

f

0.08% as o

f

D

ecember 31, 2009. Our primary interest rate risk exposure is to a decline in interest rates which would result in a

decline in interest income. Due to the current market yield, a further decline in interest rates would have a de

minimi

s

i

mpact on earn

i

n

g

s

.

F

oreign Currenc

y

Exc

h

ange Rate

s

We are expose

d

to

f

ore

i

gn currency exc

h

ange rate r

i

s

k

as

i

tre

l

ates to our

i

nternat

i

ona

l

operat

i

ons. We current

ly

do not hed

g

e our currenc

y

exchan

g

e rate risk and, as such, we are exposed to fluctuations in the value of th

e

U

nited States dollar a

g

ainst other currencies. Our international subsidiaries and equit

y

investees

g

enerall

y

use th

e

c

urrency o

f

t

h

e

j

ur

i

s

di

ct

i

on

i

nw

hi

c

h

t

h

ey res

id

e, or

l

oca

l

currency, as t

h

e

i

r

f

unct

i

ona

l

currency. Assets an

dli

a

bili

t

i

es

are trans

l

ate

d

at exc

h

an

g

e rates

i

ne

ff

ect as o

f

t

h

e

b

a

l

ance s

h

eet

d

ate an

d

t

h

e resu

l

t

i

n

g

trans

l

at

i

on a

dj

ustments are

r

ecorded within accumulated other com

p

rehensive income (loss). Income and ex

p

ense accounts are translated at the

average monthly exchange rates during the reporting period. The effects of changes in exchange rates between the

d

es

ig

nate

df

unct

i

ona

l

currenc

y

an

d

t

h

e currenc

yi

nw

hi

c

h

a transact

i

on

i

s

d

enom

i

nate

d

are recor

d

e

d

as

f

ore

ig

n

c

urrenc

y

transact

i

on

g

a

i

ns (

l

osses) an

d

recor

d

e

di

nt

h

e conso

lid

ate

d

statement o

f

operat

i

ons. We

b

e

li

eve t

h

at t

he

fluctuation of forei

g

n currenc

y

exchan

g

e rates did not have a material impact on our consolidated financial

s

tatements.

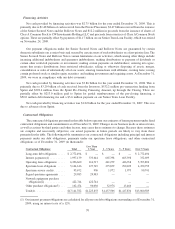

C

re

d

it Ris

k

At December 31, 2009, we held available-for-sale short-term and long-term investments with a fair value an

d

c

arrying value of

$

2.19 billion and a cost of

$

2.19 billion, comprised of United States government and agency issue

s

an

d

ot

h

er

d

e

b

t secur

i

t

i

es. We re

g

u

l

ar

ly

rev

i

ew t

h

e carr

yi

n

g

va

l

ue o

f

our s

h

ort-term an

dl

on

g

-term

i

nvestments an

d

i

dentify and record losses when events and circumstances indicate that declines in the fair value of such assets below

our accounting basis are other-than-temporary. The estimated fair values of certain of our investments are subject to

sig

n

ifi

cant

fl

uctuat

i

ons

d

ue to vo

l

at

ili

t

y

o

f

t

h

e cre

di

t mar

k

ets

i

n

g

enera

l

, compan

y

-spec

ifi

cc

i

rcumstances, c

h

an

g

e

s

i

n

g

eneral economic conditions and use of mana

g

ement

j

ud

g

ment when observable market prices and parameters

are not fully available

.

O

ther debt securities are variable rate debt instruments whose interest rates are normally reset approximatel

y

e

ver

y

30 or 90

d

a

y

st

h

rou

gh

an auct

i

on process. A port

i

on o

f

our

i

nvestments

i

not

h

er

d

e

b

t secur

i

t

i

es represent

i

nterests

i

nco

ll

atera

li

ze

dd

e

b

to

blig

at

i

ons, w

hi

c

h

we re

f

er to as CDOs, supporte

dby

pre

f

erre

d

equ

i

t

y

secur

i

t

i

es o

f

i

nsurance companies and financial institutions with stated final maturity dates in 2033 and 2034. As of Decem

-

ber 31, 2009 the total fair value and carr

y

in

g

value of our securit

y

interests in CDOs was

$

13.2 million and our cos

t

was

$

9.0 million. We also own other debt securities that are Auction Rate Market Preferred securities issued b

y

a

m

onoline insurance compan

y

and these securities are perpetual and do not have a final stated maturit

y

. In Jul

y

2009,

th

e

i

ssuer’s cre

di

t rat

i

ng was

d

owngra

d

e

d

to CC an

d

Caa2

b

y Stan

d

ar

d

& Poor’s an

d

Moo

d

y’s rat

i

ng serv

i

ces

,

r

espect

i

ve

ly

,an

d

t

h

e tota

lf

a

i

rva

l

ue an

d

carr

yi

n

g

va

l

ue o

f

our Auct

i

on Rate Mar

k

et Pre

f

erre

d

secur

i

t

i

es was wr

i

tte

n

down to $0 as of December 31, 2009. Current market conditions do not allow us to estimate when the auctions for

our ot

h

er

d

e

b

t secur

i

t

i

es w

ill

resume,

if

ever, or

if

a secon

d

ary mar

k

et w

ill d

eve

l

op

f

or t

h

ese secur

i

t

i

es. As a resu

l

t,

our ot

h

er

d

e

b

t secur

i

t

i

es are c

l

ass

ifi

e

d

as

l

ong-term

i

nvestments

.

7

2