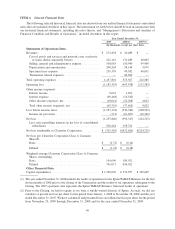

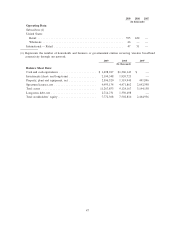

Clearwire 2009 Annual Report Download - page 51

Download and view the complete annual report

Please find page 51 of the 2009 Clearwire annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

|

|

account t

h

e NOL

d

e

d

uct

i

ons an

d

ot

h

er tax

b

ene

fi

ts reasona

bl

y expecte

d

to

b

eava

il

a

bl

etoC

l

earw

i

re. See t

he

s

ections titled “Risk Factors — Mandator

y

tax distributions ma

y

deprive Clearwire Communications of funds tha

t

are required in its business” and “Certain Relationships and Related Transactions, and Director Independence”

b

eg

i

nn

i

ng on pages 38 an

d

127, respect

i

ve

l

y, o

f

t

hi

s report.

Sales of certain former Clearwire assets by Clearwire Communications may trigger taxable gain t

o

C

learwire.

I

f Clearwire Communications sells, in a taxable transaction, an Old Clearwire asset that had built-in

g

ain at th

e

t

ime of its contribution to Clearwire Communications, then, under Section 704(c) of the Code, the tax gain on th

e

s

a

l

eo

f

t

h

e asset

g

enera

lly

w

ill b

ea

ll

ocate

dfi

rst to C

l

earw

i

re

i

n an amount up to t

h

e rema

i

n

i

n

g

(unamort

i

ze

d)

p

ort

i

on o

f

t

h

e

b

u

il

t-

i

n

g

a

i

nont

h

eO

ld

C

l

earw

i

re asset. Un

d

er t

h

e Operat

i

n

g

A

g

reement, un

l

ess C

l

earw

i

r

e

Communications has a bona fide non-tax business need (as defined in the Operatin

g

A

g

reement), Clearwire

Commun

i

cat

i

ons w

ill

not enter

i

nto a taxa

bl

esa

l

eo

f

O

ld

C

l

earw

i

re assets t

h

at are

i

ntang

ibl

e property an

d

t

h

a

t

would cause Clearwire to be allocated under Section 704(c) more than

$

10 million of built-in

g

ains durin

g

an

y

3

6-month

p

eriod. For this

p

ur

p

ose, Clearwire Communications will have a bona fide non-tax business need with

r

espect to t

h

esa

l

eo

f

O

ld

C

l

earw

i

re assets,

if

(1) t

h

e taxa

bl

esa

l

eo

f

t

h

eO

ld

C

l

earw

i

re assets w

ill

serve a

b

ona

fid

e

b

us

i

ness nee

d

o

f

C

l

earw

i

re Commun

i

cat

i

ons’ w

i

re

l

ess

b

roa

db

an

db

us

i

ness an

d(

2

)

ne

i

t

h

er t

h

e taxa

bl

esa

l

e nor t

he

r

einvestment or other use of the proceeds is si

g

nificantl

y

motivated b

y

the desire to obtain increased income tax

b

ene

fi

ts

f

or t

h

e mem

b

ers or to

i

mpose

i

ncome tax costs on C

l

earw

i

re. Accor

di

ng

l

y, C

l

earw

i

re may recogn

i

ze

b

u

il

t-

i

n gain on the sale of Old Clearwire assets (1) in an amount up to

$

10 million, in any 36-month period, and (2) in

g

reater amounts, if the standard of bona fide non-tax business need is satisfied. If Clearwire Communications sells

O

ld Clearwire assets with unamortized built-in gain, then Clearwire is likely to be allocated a share of the taxable

i

ncome o

f

C

l

earw

i

re Commun

i

cat

i

ons t

h

at excee

d

s

i

ts proport

i

onate econom

i

c

i

nterest

i

nC

l

earw

i

re Commun

i-

c

at

i

ons, an

d

ma

yi

ncur a mater

i

a

lli

a

bili

t

yf

or taxes. However, su

bj

ect to t

h

eex

i

st

i

n

g

an

d

poss

ibl

e

f

uture

li

m

i

tat

i

ons

on the use of Clearwire’s NOLs under Section 382 and Section 384 of the Code, Clearwire’s NOLs are generally

e

xpecte

d

to

b

eava

il

a

bl

etoo

ff

set, to t

h

e extent o

f

t

h

ese NOLs,

i

tems o

fi

ncome an

dg

a

i

na

ll

ocate

d

to C

l

earw

i

re

by

C

l

earw

i

re Commun

i

cat

i

ons. See t

h

e sect

i

on t

i

t

l

e

d

“R

i

s

k

Factors — T

h

ea

bili

t

y

o

f

C

l

earw

i

re to use

i

ts net operat

i

n

g

losses to offset its income and

g

ain is sub

j

ect to limitation If use of its NOLs is limited, there is an increased

lik

e

lih

oo

d

t

h

at C

l

earw

i

re Commun

i

cat

i

ons w

ill b

e requ

i

re

d

to ma

k

e a tax

di

str

ib

ut

i

on to C

l

earw

i

re”

b

eg

i

nn

i

ng on

p

age 39 o

f

t

hi

s report. C

l

earw

i

re Commun

i

cat

i

ons

i

s requ

i

re

d

to ma

k

e

di

str

ib

ut

i

ons to C

l

earw

i

re

i

n amounts

n

ecessar

y

to pa

y

all taxes reasonabl

y

determined b

y

Clearwire to be pa

y

able with respect to its distributive share o

f

th

e taxa

bl

e

i

ncome o

f

C

l

earw

i

re Commun

i

cat

i

ons, a

f

ter ta

ki

ng

i

nto account t

h

e NOL

d

e

d

uct

i

ons an

d

ot

h

er tax

b

ene

fi

ts reasona

bl

y expecte

d

to

b

eava

il

a

bl

etoC

l

earw

i

re. See t

h

e sect

i

ons t

i

t

l

e

d

“R

i

s

k

Factors — Man

d

atory tax

distributions ma

y

deprive Clearwire Communications of funds that are required in its business” and “Certain

Re

l

at

i

ons

hi

ps an

d

Re

l

ate

d

Transact

i

ons, an

d

D

i

rector In

d

epen

d

ence”

b

eg

i

nn

i

ng on pages 38 an

d

127, respect

i

ve

l

y,

o

f

t

hi

s report

.

S

p

rint an

d

t

h

e Investors ma

y

s

h

i

f

ttoC

l

earwire t

h

e tax

b

ur

d

en o

f

a

dd

itiona

lb

ui

l

t-in gain t

h

roug

ha

h

olding company exchange.

Un

d

er t

h

e Operat

i

n

g

A

g

reement, Spr

i

nt or an Investor ma

y

a

ff

ect an exc

h

an

g

eo

f

C

l

earw

i

re Commun

i

cat

i

ons

Class B Common Interests and Class B Common Stock for Class A Common Stock b

y

transferrin

g

to Clearwire a

h

o

ldi

ng company t

h

at owns t

h

eC

l

earw

i

re Commun

i

cat

i

ons C

l

ass B Common Interests an

d

C

l

ass B Common Stoc

k

i

n a transact

i

on

i

nten

d

e

d

to

b

e tax-

f

ree

f

or Un

i

te

d

States

f

e

d

era

li

ncome tax purposes (w

hi

c

h

t

h

e Operat

i

n

g

Ag

reement refers to as a holdin

g

compan

y

exchan

g

e). In particular, if Clearwire, as the mana

g

in

g

member o

f

C

l

earw

i

re Commun

i

cat

i

ons,

h

as approve

d

a taxa

bl

esa

l

e

b

yC

l

earw

i

re Commun

i

cat

i

ons o

ff

ormer Spr

i

nt assets t

h

a

t

are

i

ntang

ibl

e property an

d

t

h

at wou

ld

cause Spr

i

nt to

b

ea

ll

ocate

d

un

d

er Sect

i

on 704(c) o

f

t

h

eCo

d

e more t

h

an

$10 million of built-in

g

ain durin

g

an

y

36-month period, then, durin

g

a specified 15-business-da

y

period, Clearwire

Commun

i

cat

i

ons w

ill b

e prec

l

u

d

e

df

rom enter

i

ng

i

nto any

bi

n

di

ng contract

f

or t

h

e taxa

bl

esa

l

eo

f

t

h

e

f

ormer Spr

i

nt

assets, an

d

Spr

i

nt w

ill h

ave t

h

er

i

g

h

t to trans

f

er C

l

earw

i

re Commun

i

cat

i

ons C

l

ass B Common Interests an

d

C

l

ass

B

Common Stock to one or more holdin

g

companies, and to transfer those holdin

g

companies to Clearwire in holdin

g

c

ompany exchanges. In any holding company exchange, Clearwire will succeed to all of the built-in gain and other

t

ax c

h

aracter

i

st

i

cs assoc

i

ate

d

w

i

t

h

t

h

e trans

f

erre

d

C

l

earw

i

re Commun

i

cat

i

ons C

l

ass B Common Interests,

i

nc

l

u

di

ng

(1)

i

nt

h

e case o

f

a trans

f

er

by

Spr

i

nt, an

y

rema

i

n

i

n

g

port

i

on o

f

t

h

e

b

u

il

t-

i

n

g

a

i

nex

i

st

i

n

g

at t

h

e

f

ormat

i

on o

f

4

1