Vonage 2008 Annual Report Download - page 50

Download and view the complete annual report

Please find page 50 of the 2008 Vonage annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

|

|

Net Operatin

g

Loss Carryforwards

A

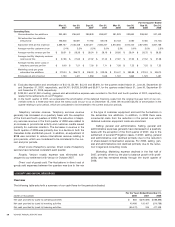

s of December 31, 2008, we had net operating loss carryfor

-

wards for U.S. federal and state tax purposes of $765,748 and

$

726,521, respectively, expiring at various times from years end

-

i

ng 2020 t

h

roug

h

2028.

I

na

ddi

t

i

on, we

h

a

d

net operat

i

ng

l

oss

carryforwards for Canadian tax purposes of $56,161 expirin

g

t

hrough 2027. We also had net operating loss carry

f

orwards

f

o

r

United Kingdom tax purposes of

$

33,409 with no expiration date.

Under

S

ection 382 of the Internal Revenue

C

ode, if a cor

p

o

-

r

ation under

g

oes an “ownership chan

g

e”

(g

enerally defined as

a

greater than 50% change (by value) in its equity ownership over

a

t

hree-year period

)

, the corporation’s ability to use its pre-change

of control net operatin

g

loss carry forward and other pre-chan

g

e

t

ax attributes against its post-change income may be limited. The

S

ection 382 limitation is applied annually so as to limit the use o

f

our pre-chan

g

e net operatin

g

loss carryforwards to an amoun

t

t

hat generally equals the value o

f

our stock immediately be

f

or

e

t

he ownership change multiplied by a designated federal long-

t

erm tax-exempt rate.

I

na

ddi

t

i

on, we ma

yb

ea

bl

eto

i

ncrease t

he

b

ase Section 382 limitation amount during the first five years fol-

l

ow

i

ng t

h

e owners

hi

pc

h

ange to t

h

e extent

i

t rea

li

zes

b

u

il

t-

i

nga

i

ns

d

ur

i

n

g

t

h

at t

i

me per

i

o

d

.

Ab

u

il

t-

i

n

g

a

i

n

g

enera

ll

y

i

s

g

a

i

nor

i

ncom

e

attributable to an asset that was held at the date o

f

the ownership

change and that had a fair market value in excess of the tax basis

at the date of the ownership chan

g

e.

S

ection 382 provides that

an

y

unused Section 382 limitation amount can be carried forward

and aggregated with the following year’s available net operatin

g

l

osses. Due to the cumulative impact of our equity issuances over

t

he three year period ended April 2005, a chan

g

eo

f

ownership

occurred upon the issuance of our previously outstanding

S

er-

i

es E Preferred

S

tock at the end of A

p

ril 2005. As a result,

$

171,147 of the total U.S. net operatin

g

losses will be subject t

o

an annual base limitation of

$

39

,

374. As noted above

,

we believe

we may be able to increase the base

S

ection 382 limitation fo

r

b

uilt-in

g

ains durin

g

the

f

irst

f

ive years

f

ollowin

g

the ownershi

p

change

.

S

hare-Based

C

ompensation

Prior to the adoption of SFAS 123(R), we accounted fo

r

s

hare-based awards to employees and directors using th

e

i

ntr

i

ns

i

cva

l

ue met

h

o

di

n accor

d

ance w

i

t

h APB

25, as a

ll

owe

d

u

nder Statement of Financial Accountin

g

Standards No. 123

,

A

ccounting for

S

tock-Based

C

ompensation, or

S

FA

S

123. Unde

r

th

e

i

ntr

i

ns

i

cva

l

ue met

h

o

d

,nos

h

are-

b

ase

d

com

p

ensat

i

o

n

expense

f

or employee stock options had been reco

g

nized in our

r

esults of o

p

erations in

p

rior

p

eriods unless the exercise

p

rice o

f

th

e stoc

k

opt

i

ons

g

rante

d

to emp

l

oyees an

ddi

rectors was

l

ess

t

han the

f

air market value o

f

the underlyin

g

common stock at th

e

date o

f

grant. In accordance with the modi

f

ied prospective tran-

s

ition method that we used in adoptin

gS

FA

S

123

(

R

)

, the con-

s

olidated

f

inancial statements prior to 2006 have not bee

n

r

estated to re

f

lect, and do not include, the

p

ossible im

p

act o

f

S

FA

S

123

(

R

)

.

Recent Accountin

g

Pronouncement

s

I

n June 2008, the Financial Accounting Standards Boar

d

(

“FA

S

B”

)

ratified Emer

g

in

g

Issues Task Force Issue No. 07-5,

“

Determinin

g

Whether an Instrument (or an Embedded Feature) Is

I

ndexed to an Entity’s Own Stock” (“EITF 07-5”). EITF 07-5 pro

-

vid

es t

h

at an ent

i

ty s

h

ou

ld

use a two step approac

h

to eva

l

uat

e

w

hether an equit

y

-linked financial instrument (or embedded fea-

ture) is indexed to its own stock, including evaluating the

i

nstrument

’

s cont

i

n

g

ent exerc

i

se an

d

sett

l

ement prov

i

s

i

ons.

I

ta

l

s

o

c

lari

f

ies on the impact o

ff

orei

g

n currency denominated strike

p

rices and market-based employee stock option valuatio

n

i

n

s

tr

u

m

e

nt

so

nth

ee

v

a

l

ua

ti

o

n. EITF

0

7-

5

i

se

ff

ec

tiv

e

f

o

rfi

scal

years be

g

innin

g

a

f

ter December 15, 2008. The adoption o

f

EITF

07-5 will not have an im

p

act on our consolidated

f

inancial

p

osition

a

nd results of o

p

erations.

In May 2008, the FA

S

B issued

S

tatement of Financia

l

Accountin

g

Standards No. 162 (“SFAS No. 162”), “The Hierarch

y

o

f Generally Accepted Accounting Principles.

”

S

FA

S

No. 16

2

i

dentifies the sources of accountin

g

principles and the framewor

k

f

or selectin

g

the principles used in the preparation o

ff

inancia

l

s

tatements that are presented in con

f

ormity with generally

a

ccepted accountin

g

principles.

S

FA

S

No. 162 becomes effective

6

0 days followin

g

the Securities and Exchan

g

e Commission’s

a

pproval of the Public Company Accounting Oversight Boar

d

a

mendments to AU

S

ection 411,

“

The Meanin

g

of Present Fairl

y

i

n

C

onformit

y

With Generall

y

Accepted Accountin

g

Principles.

”

W

e

d

o not ex

p

ect that the ado

p

tion of SFAS No. 162 will have a

material im

p

act on our consolidated financial statements.

In A

p

ril 2008, the FA

S

B issued F

S

P No. 142-3

(

“F

S

P 142-3”

)

,

“Determination of the Useful Life of Intan

g

ible Assets.” FSP 142-3

a

mends the

f

actors an entity should consider in developing

renewal or extension assumptions used in determinin

g

the useful

l

ife of reco

g

nized intan

g

ible assets under FASB Statement

No. 142, “Goodwill and Other Intangible Assets.” This new guid-

a

nce app

li

es prospect

i

ve

l

yto

i

ntan

gibl

e assets t

h

at are acqu

i

re

d

i

ndividually or with a

g

roup o

f

other assets in business combina-

tions and asset ac

q

uisitions. FSP 142-3 is effective for financia

l

s

tatements issued for fiscal years and interim periods be

g

innin

g

a

fter December 15, 2008. Earl

y

adoption is prohibited. Since thi

s

g

uidance will be applied prospectively, on adoption, there will b

e

no im

p

act to our current consolidated financial statements

.

In March 2008, the FA

S

B affirmed the consensus of FA

S

B

S

taff Position (FSP) Accountin

g

Principles Board Opinion No. 14-

1

(

APB 14-1

)

,Accounting for Convertible Debt Instruments That

Ma

y

Be

S

ettled in

C

ash upon

C

onversion

(

Includin

g

Partial

C

as

h

Settlement

)

,

w

hi

c

h

app

li

es to a

ll

convert

ibl

e

d

e

b

t

i

nstruments t

h

at

have a net settlement

f

eature

;

which means that such convertibl

e

d

e

b

t

i

nstruments,

b

yt

h

e

i

r terms, may

b

e sett

l

e

d

e

i

t

h

er w

h

o

ll

yor

p

artiall

y

in cash upon conversion. FSP APB 14-1 requires issuer

s

of

convertible debt instruments that ma

y

be settled wholl

y

or

p

artially in cash upon conversion to separately account for th

e

l

iabilit

y

and equit

y

components in a manner re

f

lective o

f

the issu-

e

r’s nonconvertible debt borrowing rate. Previous guidance

p

rovided for accounting for this type of convertible debt instru-

ment entirel

y

as debt. F

S

P APB 14-1 is effective for financia

l

s

tatements issued

f

or

f

iscal years beginning a

f

ter December 15,

2008 and interim periods within those fiscal years. The adoptio

n

o

fF

S

P APB 14-1 will not have an impact on our financia

l

st

a

t

emen

t

s.

In Februar

y

2008, the FASB issued FASB FSP 157-2, which

d

elayed the effective date of

S

FA

S

No. 157 for all nonfinancia

l

a

ssets and non

f

inancial liabilities, except those that are reco

g

-

nized or disclosed at

f

air value in the

f

inancial statements on a

recurring basis

(

at least annually

)

, until fiscal years beginning after

November 15, 2008, and interim periods within those

f

iscal

y

ears.

T

hese non

f

inancial items include assets and liabilities such a

s

42

VO

NA

G

E ANN

U

AL REP

O

RT 2008