Office Depot 2004 Annual Report Download - page 52

Download and view the complete annual report

Please find page 52 of the 2004 Office Depot annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

|

|

OFFICE DEPOT, INC.

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS

50 |Office Depot 2004 Annual Report

accounts, such as receivables and payables, are included as

a component of operating expenses, though historically these

amounts have been immaterial.

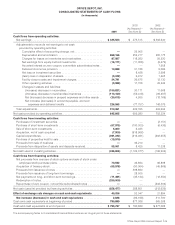

Cash Equivalents: All short-term highly liquid securities

with maturities of three months or less from the date of acquisi-

tion are classified as cash equivalents. Cash and cash equiva-

lents consist of funds held in general checking accounts and

money market accounts.

Short-term Investments: Investments in debt and auction

rate securities are classified as available-for-sale and are

reported at fair market value, based on quoted market prices

using the specific identification method. Unrealized gains and

losses, net of applicable income taxes, are reported as a com-

ponent of other comprehensive income. Interest earned on

these funds is used to purchase additional units. The historical

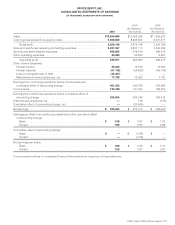

cost and fair value of this investment was $161.1 million and

$100.2 million at December 25, 2004 and December 27, 2003,

respectively. There were no unrealized losses at either period.

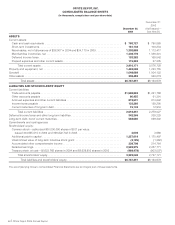

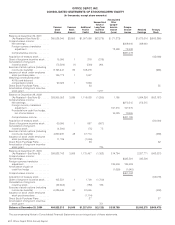

Receivables: Trade receivables, net, totaled $871.7 million

and $797.7 million at December 25, 2004 and December 27,

2003, respectively. An allowance for doubtful accounts has

been recorded to reduce receivables to an amount expected

to be collectible from customers. The allowance recorded at

December 25, 2004 and December 27, 2003 was $38.0 million

and $34.2 million, respectively. Receivables generated through

a private label credit card program are transferred to financial

services companies, a portion of which have recourse to

Office Depot.

Our exposure to credit risk associated with trade receiv-

ables is limited by having a large customer base that extends

across many different industries and geographic regions.

However, receivables may be adversely affected by an eco-

nomic slowdown in the U.S. or internationally.

Other receivables are $432.2 million and $314.7 million as

of December 25, 2004 and December 27, 2003, respectively,

of which $356.8 and $284.7 are amounts due from vendors

under purchase rebate, cooperative advertising and various

other marketing programs. These vendor receivables are net of

collection allowances of $11.0 million and $17.5 million at

December 25, 2004 and December 27, 2003, respectively.

Merchandise Inventories: Inventories are stated at the

lower of cost or market value. The weighted average method is

used to determine the cost of a majority of our inventory and the

first-in-first-out method is used for international operations.

Income Taxes: Income tax expense is recognized at appli-

cable U.S. or international tax rates. Certain revenue and

expense items may be recognized in one period for financial

statement purposes and in a different period’s income tax

return. The tax effects of such differences are reported as

deferred income taxes.

Historically, earnings of foreign subsidiaries have been the

source for overseas expansion. Because these earnings have

NOTE A—Summary of Significant Accounting Policies

Nature of Business: Office Depot, Inc. is a global supplier

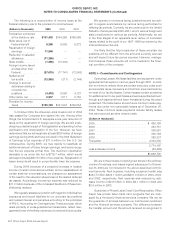

of office products and services, with sales in 21 countries out-

side the United States and Canada under the Office Depot®,

Viking Office Products®, Viking Direct®, 4Sure.com®,

Guilbert®, and NiceDay™ brand names. Products and services

are offered through wholly owned retail stores, contract

business-to-business sales relationships, commercial catalogs

and multiple web sites.

Basis of Presentation: The consolidated financial statements

of Office Depot, Inc. and its subsidiaries have been prepared

in accordance with accounting principles generally accepted

in the United States of America. All intercompany transactions

have been eliminated in consolidation. Non-controlling invest-

ments in joint ventures selling office products and services in

Mexico and Israel are accounted for using the equity method.

Their results are included in miscellaneous income (expense),

net in the Consolidated Statements of Earnings.

Discontinued Operations: In August 2002, we announced

our decision to sell the Australian operations and completed the

sale in January 2003 with no significant impact on net earnings.

This business has been reported as a discontinued operation.

Australia’s sales and pre-tax loss, respectively, were $80.9 mil-

lion and $(1.0) million for 2002. The impact on basic earnings

per share was $(0.01) for 2002.

Fiscal Year: Fiscal years are based on a 52- or 53-week

period ending on the last Saturday in December. All periods

presented consist of 52 weeks. Fiscal year 2005 will include

53 weeks.

Estimates and Assumptions: Preparation of these financial

statements in conformity with accounting principles generally

accepted in the United States of America requires management

to make estimates and assumptions that affect amounts

reported in the financial statements and related notes. Actual

results may differ from those estimates.

Foreign Currency: Assets and liabilities of international oper-

ations are translated into U.S. dollars using the exchange rate

at the balance sheet date. Revenues and expenses are trans-

lated at average monthly exchange rates. Translation adjust-

ments resulting from this process are recorded in stockholders’

equity as a component of other comprehensive income.

Monetary assets and liabilities denominated in a currency

other than a consolidated entity’s functional currency result in

transaction gains or losses from the remeasurement at spot

rates at the end of the period. Foreign currency gains and

losses that relate to non-operational accounts, such as cash and

investments, are recorded in miscellaneous income (expense),

net in the Consolidated Statements of Earnings. During 2003,

approximately $11.8 million was recognized as a foreign cur-

rency gain resulting from holding euro investments in a dollar

functional currency subsidiary in advance of an acquisition (see

Note D). Foreign currency gains and losses on operational