Medtronic 2014 Annual Report Download - page 84

Download and view the complete annual report

Please find page 84 of the 2014 Medtronic annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

86 -

87

87 -

88

88 -

89

89 -

90

90 -

91

91 -

92

92 -

93

93 -

94

94 -

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

|

|

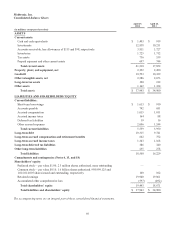

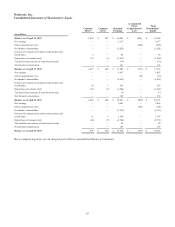

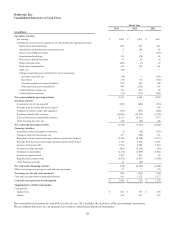

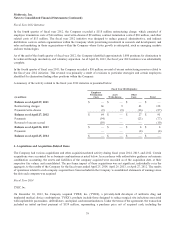

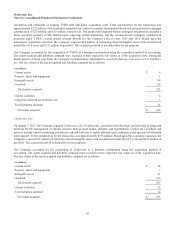

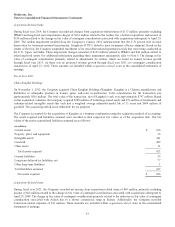

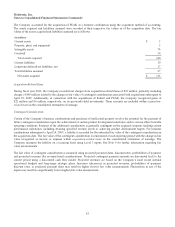

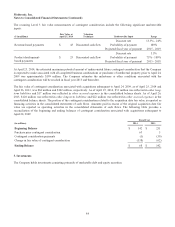

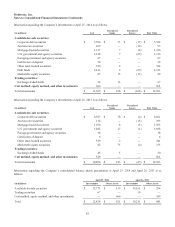

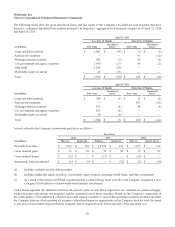

Medtronic, Inc.

Notes to Consolidated Financial Statements (Continued)

entity to disclose both gross and net information about instruments and transactions eligible for offset in the balance sheet as

well as instruments and transactions executed under a master netting or similar arrangement and was issued to enable users of

financial statements to understand the effects or potential effects of those arrangements on its financial position. The Company

retrospectively adopted this accounting guidance in the first quarter of fiscal year 2014. The required disclosures are included in

Note 9. Since the accounting guidance only requires disclosure, its adoption did not have a material impact on the Company’s

consolidated financial statements.

In July 2012, the FASB updated the accounting guidance related to annual and interim indefinite-lived intangible asset

impairment testing. The updated accounting guidance allows entities to first assess qualitative factors before performing a

quantitative assessment of the fair value of indefinite-lived intangible assets. If it is determined on the basis of qualitative

factors that the fair value of indefinite-lived intangible assets is more likely than not less than the carrying amount, the existing

quantitative impairment test is required. Otherwise, no further impairment testing is required. The Company adopted this

accounting guidance in the first quarter of fiscal year 2014 and its adoption did not have a material impact on the Company’s

consolidated financial statements.

In February 2013, the FASB expanded the disclosure requirements with respect to changes in accumulated other comprehensive

income (AOCI). Under this new guidance, companies are required to disclose the amount of income (or loss) reclassified out of

AOCI to each respective line item on the statements of earnings where net income is presented. The guidance allows companies

to elect whether to disclose the reclassification either in the notes to the financial statements or parenthetically on the face of the

financial statements. In the first quarter of fiscal year 2014, the Company prospectively adopted this guidance. The required

disclosures are included in Note 16. Since the accounting guidance only impacts disclosure requirements, its adoption did not

have a material impact on the Company’s consolidated financial statements.

Not Yet Adopted

In March 2013, the FASB issued amended guidance on a parent company’s accounting for the CTA recorded in AOCI

associated with a foreign entity. The amendment requires a parent to release into net income the CTA related to its investment in

a foreign entity when it either sells a part or all of its investment, or no longer holds a controlling financial interest, in a

subsidiary or group of assets within a foreign entity. This accounting guidance is effective for the Company beginning in the

first quarter of fiscal year 2015. Subsequent to adoption, this amended guidance would impact the Company’s financial position

and results of operations prospectively in the instance of an event or transaction described above.

In July 2013, the FASB issued amended guidance on the financial statement presentation of an unrecognized tax benefit when a

net operating loss carryforward, similar tax loss, or tax credit carryforward exists. The guidance requires an unrecognized tax

benefit, or a portion of an unrecognized tax benefit, to be presented as a reduction of a deferred tax asset when a net operating

loss carryforward, similar tax loss, or tax credit carryforward exists, with certain exceptions. This accounting guidance is

effective prospectively for the Company beginning in the first quarter of fiscal year 2015. The adoption is not expected to have a

material impact on the Company’s consolidated financial statements.

In April 2014, the FASB issued amended guidance for reporting discontinued operations. The amended guidance changes the

criteria for determining when the results of operations are to be reported as discontinued operations and expands the related

disclosure requirements. The guidance defines a discontinued operation as a disposal of a component or group of components

that is disposed of or classified as held for sale which is a strategic shift that has, or will have, a major effect on financial

position and results of operations. This accounting guidance is effective prospectively for the Company beginning in the first

quarter of fiscal year 2016, with early adoption permitted. The adoption is not expected to have a material impact on the

Company’s consolidated financial statements.

In May 2014, the FASB issued amended revenue recognition guidance to clarify the principles for recognizing revenue from

contracts with customers. The guidance requires an entity to recognize revenue to depict the transfer of goods or services to

customers in an amount that reflects the consideration to which an entity expects to be entitled in exchange for those goods or

services. The guidance also requires expanded disclosures relating to the nature, amount, timing, and uncertainty of revenue and

cash flows arising from contracts with customers. Additionally, qualitative and quantitative disclosures are required about

customer contracts, significant judgments and changes in judgments, and assets recognized from the costs to obtain or fulfill a

contract. This accounting guidance is effective for the Company beginning in the first quarter of fiscal year 2018 using one of

76