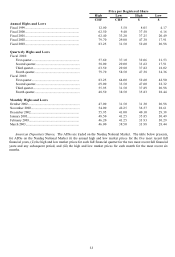

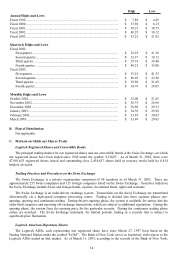

Logitech 2003 Annual Report Download - page 49

Download and view the complete annual report

Please find page 49 of the 2003 Logitech annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

|

|

36

shareholder preemptive rights, except to the extent that these preemptive rights have been excluded or limited by the

shareholders.

In addition, U.S. securities laws may restrict the ability of U.S. ADS holders to participate in Logitech rights

offerings, share dividends or warrant dividends in the event that Logitech is unable or chooses not to register these

securities under U.S. securities laws and cannot rely on an exemption from registration. Logitech is not currently

planning any rights offering or to issue any share or warrant dividends, or any similar transaction. Logitech may

choose to do so in the future and there can be no assurance that it will be feasible to include U.S. persons in the

transaction. If Logitech does issue these type of securities in the future, it may issue them to the Depositary, which

may sell the securities for the benefit of the holders of Logitech ADSs. There can be no assurance as to the value, if

any, the Depositary would receive upon the sale of these securities.

There are no legislative or other legal provisions currently in effect in Switzerland or arising under Logitech’s

articles of incorporation restricting the export or import of capital, or that affect the remittance of dividends, interest

or other payments to nonresident holders of Logitech securities. Cash dividends payable in Swiss francs on shares

and ADSs may be officially transferred from Switzerland and converted into any other convertible currency. There

are no limitations imposed by Swiss laws or Logitech’s articles on the right of non-Swiss residents to hold or vote the

shares or ADSs.

E. Taxation

The following is a summary of certain Swiss tax matters that may be relevant with respect to the acquisition,

ownership and disposition of registered shares or ADSs (which are evidenced by ADSs).

This summary addresses laws in Switzerland currently in effect, as well as the 1997 Convention (entered into

force on December 1997) between the United States of America and the Swiss Confederation for the Avoidance of

Double Taxation with Respect to Taxes on Income (the "Treaty"), both of which are subject to change (or changes in

interpretation), possibly with retroactive effect.

For purposes of the Treaty and the Internal Revenue Code of 1986, as amended (the “Code”), United States

Holders of ADSs are treated as the owners of the registered shares corresponding to such ADSs. Accordingly, the

Swiss tax consequences discussed below also generally apply to United States holders of registered shares.

Swiss Taxation

Gain on Sale

Under current Swiss law, a holder of registered shares or ADSs who (i) is a non-resident of Switzerland, (ii)

during the taxable year has not engaged in a trade or business through a permanent establishment within Switzerland

and (iii) is not subject to taxation by Switzerland for any other reason, will be exempted from any Swiss federal,

cantonal or municipal income or other tax on gains realized during the year on the sale of registered shares or ADSs.

Stamp, Issue and Other Taxes

Switzerland generally does not impose stamp, registration or similar taxes on the sale of registered shares or

ADSs by a holder thereof unless such sale or transfer occurs through or with a Swiss securities dealer (as defined in

the Swiss Stamp Duty Law).

Withholding Tax

Under present Swiss law, any dividends paid in respect of registered shares will be subject to the Swiss

Anticipatory Tax at the rate of 35%, and the Company will be required to withhold tax at such rate from any dividend

payments made to a holder of registered shares. Such dividend payments may qualify for reduction of or refund of

the Swiss Anticipatory Tax by reason of the provisions of a double tax treaty between Switzerland and the country of

residence or incorporation of a holder, and in such cases such holder will be entitled to claim a refund of all or a

portion of such tax in accordance with such treaty. The Treaty provides for a mechanism whereby a United States

resident or United States corporations can generally seek a refund of the Swiss Anticipatory Tax paid on dividends in

respect of registered shares, to the extent such withholding exceeds 15%. A United States corporation that holds

more than 10% of the share capital of a Swiss company can seek a refund of the Swiss Anticipatory Tax paid on

dividends to the extent such withholding tax exceeds 5% under the double tax treaty.