Tesco 2013 Annual Report Download - page 21

Download and view the complete annual report

Please find page 21 of the 2013 Tesco annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

11 -

12

12 -

13

13 -

14

14 -

15

15 -

16

16 -

17

17 -

18

18 -

19

19 -

20

20 -

21

21 -

22

22 -

23

23 -

24

24 -

25

25 -

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

|

|

17

Tesco PLC Annual Report and Financial Statements 2013

OVERVIEW BUSINESS REVIEW PERFORMANCE REVIEW GOVERNANCE FINANCIAL STATEMENTS

Group strategy

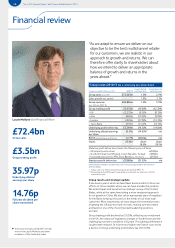

1. To grow the UK core

UK like-for-like (inc. VAT, exc. petrol) UK trading profit Definition

The profit generated from the UK business

in its retail operations.

Performance

UK profits declined, reflecting the £1 billion

investment into the UK business to improve

the shopping trip for customers.

09/10 10/11 11/12 12/13

2.6% 1.0% 0.0% (0.3)%

Definition

The growth in sales from stores that have

been open for at least a year.

Performance

We aim to continue improving like-for-like

sales in 2013/14 through our ‘Building

a Better Tesco’ plan. We expect the plan

to continue delivering stronger like-for-like

sales in 2013/14.

09/10 10/11

£2,413m £2,504m

11/12 12/13

£2,478m £2,272m

Customer rating of overall

shopping experience as

excellent or good

79%

3% improvement

on last year

Source: Marketing Sciences.

Definition

Percentage of customer ratings,

measured in exit interviews.

Performance

79% of customers find their shopping

experience excellent or good, and 98%

find it reasonable, good or excellent.

Through our UK Plan we have been

improving customers’ shopping

experiences and this focus will continue

in 2013/14.

Growth in UK online sales

+10%

Definition

The year-on-year sales growth from

total tesco.com and online telecoms.

Performance

Our online businesses are performing

well and we are pleased with the UK

sales growth. Our largest online

business, grocery home shopping, saw

increased sales growth of 12.8%, driven

in part by the success of our Grocery

Click & Collect roll-out and the launch of

our Delivery Saver subscription scheme.

2. To be an outstanding international retailer in stores and online

International trading profit

09/10 10/11

£749m

£946m∆

11/12 12/13

£1,266m†

£990m

Definition

The profit generated from our international

businesses in their retail operations.

Performance

International trading profits declined, due to the

c.£(100) million impact of regulatory restrictions

in South Korea and challenging economic

conditions, particularly in Europe.

∆ Re-presented to exclude Japan.

† The 2011/12 figure including the US was £1,113 million.

Proportion of customers pleased with their

shopping trip

≥ 95%

in 6 markets

Growth in international

online sales

+46.5%

Definition

The year-on-year sales growth from our

international online businesses.

Performance

We are pleased with the growth in online sales

across the Group. We now have online grocery

businesses in eight of our international markets,

so would expect to see sizeable growth. We

generated over £3 billion sales online for the

Group as a whole for the first time.

Definition

The number of markets where at least 95%

of customers asked were very or fairly satisfied

with their overall shopping experience – the top

two ratings.

Performance

In six of our markets at least 95% of customers

are very or fairly satisfied with their overall

shopping experience, compared to eight*

markets last year. We have seen a dip in some

of our Central European markets and we have

customer plans in place to improve the

shopping trip in all markets.

* Re-presented to exclude the US.

Source: Country customer satisfaction tracker and

Country image tracker.