TCF Bank 2004 Annual Report Download - page 13

Download and view the complete annual report

Please find page 13 of the 2004 TCF Bank annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

3 -

4

4 -

5

5 -

6

6 -

7

7 -

8

8 -

9

9 -

10

10 -

11

11 -

12

12 -

13

13 -

14

14 -

15

15 -

16

16 -

17

17 -

18

18 -

19

19 -

20

20 -

21

21 -

22

22 -

23

23 -

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

|

|

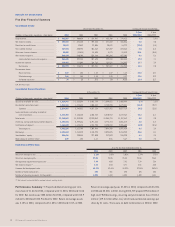

2004 Annual Report 11

0403020100

Card Revenue

(millions of dollars)

$28.8

$37.6

$47.2

$53.0

$63.3

We listen to our customers and as a result, put emphasis on conven-

ience in banking. TCF is “The Leader in Convenience Banking,” and we

use our premier convenience services to attract a large, economically

diverse and growing customer base. We provide convenience by being

open longer hours, seven days a week and open on most holidays. TCF

offers a large supermarket branch network, complemented by tradi-

tional branches, providing customers with alternative locations to

conduct their banking. TCF’s free online banking services, extensive

ATM network, automated telephone service, and Internet banking pro-

vide even more convenient options – meeting customers needs.

Strategically adding new branches where they can best support and

increase our customer base, introducing new products and services,

and enhancing our existing products and services, are strategies that

have worked well for TCF over the last decade.

TCF places emphasis on what it defines as Power Assets (higher-yielding

consumer loans, commercial loans and leasing assets) and Power

Liabilities (lower-cost checking, savings, money market and certificate

of deposit accounts). A principal strategy of TCF’s Power Assets is to

lend on a secured basis. Our strong credit quality is evidence that this

important strategy is working; TCF has one of the lowest charge-off

ratios in the banking industry. TCF’s Power Liabilities are the founda-

tion of our business and are proven profit drivers at TCF. By focusing on

both Power Assets and Power Liabilities, we recognize the important

contributions to overall profitability by both the liability and asset side

of the balance sheet. By earning at least one percent on each side of

the balance sheet, we can generate a total return on assets greater

than two percent.

TCF’s superior earnings performance allows us to regularly buy back

our own stock. In evaluating potential acquisitions, we look at the

stock buy back opportunity as an acquisition alternative that may

provide superior returns. Investing in our own stock has been good for

TCF and its shareholders.

Simple, straightforward, and enduring strategies, which are based on

a well-grounded philosophy coupled with successful execution and

solid management, have made TCF one of the top performing banks in

the United States.

De Novo Expansion

TCF continues to be committed to de novo expansion in both our branch

network and in our development of new products and services. Each

of these components play a fundamental and complementary role –

to add new branches supporting our growing customer base and to

“We listen to our customers

and as a result, put emphasis

on convenience in banking.”