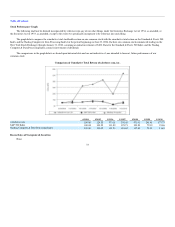

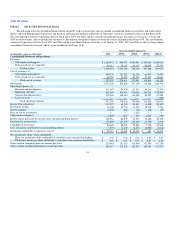

Salesforce.com 2009 Annual Report Download - page 31

Download and view the complete annual report

Please find page 31 of the 2009 Salesforce.com annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

21 -

22

22 -

23

23 -

24

24 -

25

25 -

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

|

|

Table of Contents

stock, but would not constitute a "fundamental change" that permits holders to require us to purchase their Notes under the indenture.

We may not have the ability to raise the funds necessary to re-pay the Notes.

There can be no assurance that we will have sufficient financial resources, or will be able to arrange financing, to pay the fundamental change purchase

price if holders submit their Notes for purchase by us upon the occurrence of a fundamental change or to pay the amount of cash due if holders surrender their

Notes for conversion. In addition, agreements governing any future debt may restrict our ability to make each of the required cash payments even if we have

sufficient funds to make them. Furthermore, our ability to purchase the Notes or to pay cash upon the conversion of the Notes may be limited by law or

regulatory authority. In addition, if we fail to purchase the Notes, to pay interest due on, or to pay the amount of cash due upon conversion, we will be in

default under the indenture. Our inability to pay for the Notes that are tendered for purchase or upon conversion could result in receiving substantially less

than the principal amount of the Notes.

The fundamental change provisions may delay or prevent an otherwise beneficial takeover attempt of us.

The fundamental change purchase rights, which will allow note holders to require us to purchase all or a portion of their Notes upon the occurrence of a

fundamental change and the provisions requiring an increase to the conversion rate for conversions in connection with a make-whole fundamental change may

in certain circumstances delay or prevent a takeover of us and the removal of incumbent management that might otherwise be beneficial to investors.

The convertible note hedge and warrant transactions may affect the trading price of the Notes and the market price of our common stock.

We entered into privately negotiated convertible note hedge transactions with the hedge counterparties concurrently with the issuance of the Notes. We

also entered into privately negotiated warrant transactions with the hedge counterparties. Taken together, the convertible note hedge transactions and the

warrant transactions are expected, but not guaranteed, to reduce the potential dilution with respect to our common stock upon conversion of the Notes.

As the hedge counterparties and their respective affiliates modify their hedge positions from time to time by entering into or unwinding various over-

the-counter derivative transactions with respect to our common stock, and/or by purchasing or selling shares of our common stock or the Notes in privately

negotiated transactions and/or open market transactions, their activities could adversely affect the market price of our common stock and the trading price of

the Notes.

We are subject to counterparty risk with respect to the convertible note hedge transactions.

The hedge counterparties are financial institutions or affiliates of financial institutions, and we will be subject to the risk that these hedge counterparties

may default under the convertible note hedge transactions. Our exposure to the credit risk of the hedge counterparties will not be secured by any collateral.

Recent global economic conditions have resulted in the actual or perceived failure or financial difficulties of many financial institutions. If one or more of the

hedge counterparties to one or more of our convertible note hedge transactions becomes subject to insolvency proceedings, we may become an unsecured

creditor in those proceedings with a claim equal to our exposure at the time under those transactions. Our exposure will depend on many factors but,

generally, the increase in our exposure will be correlated to the increase in our stock price and in the volatility of our stock. In addition, upon a default by one

of the hedge counterparties, we may suffer adverse tax consequences and dilution with respect to our common stock. We can provide no assurances as to the

financial stability or viability of any of the hedge counterparties.

28