Salesforce.com 2006 Annual Report Download - page 69

Download and view the complete annual report

Please find page 69 of the 2006 Salesforce.com annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

|

|

Table of Contents

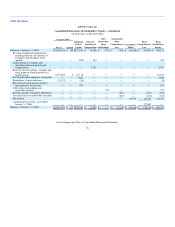

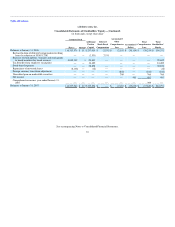

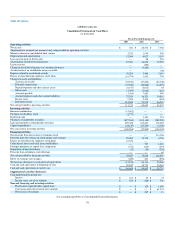

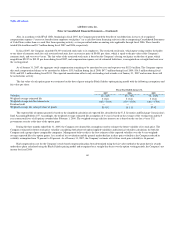

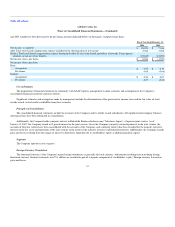

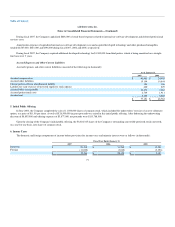

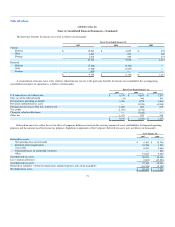

salesforce.com, inc.

Notes to Consolidated Financial Statements—(Continued)

Revenue Recognition

The Company derives its revenues from two sources: (1) subscription revenues, which are comprised of subscription fees from customers accessing its

on-demand application service, and from customers purchasing additional support beyond the standard support that is included in the basic subscription fee;

and (2) related professional services and other revenue. Other revenues consist primarily of training fees. Because the Company provides its application as a

service, the Company follows the provisions of SEC Staff Accounting Bulletin No. 104, Revenue Recognition and Emerging Issues Task Force Issue No.

00-21, Revenue Arrangements with Multiple Deliverables. The Company recognizes revenue when all of the following conditions are met:

• There is persuasive evidence of an arrangement;

• The service has been provided to the customer;

• The collection of the fees is reasonably assured; and

• The amount of fees to be paid by the customer is fixed or determinable.

The Company's arrangements do not contain general rights of return.

Subscription and support revenues are recognized ratably over the contract terms beginning on the commencement date of each contract. Amounts that

have been invoiced are recorded in accounts receivable and in deferred revenue or revenue, depending on whether the revenue recognition criteria have been

met.

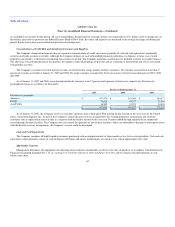

Professional services and other revenues, when sold with subscription and support offerings, are accounted for separately when these services have

value to the customer on a standalone basis and there is objective and reliable evidence of fair value of each deliverable. When accounted for separately,

revenues are recognized as the services are rendered for time and material contracts, and when the milestones are achieved and accepted by the customer for

fixed price contracts. The majority of the Company's consulting contracts are on a time and material basis. Training revenues are recognized after the services

are performed. For revenue arrangements with multiple deliverables, the Company allocates the total customer arrangement to the separate units of accounting

based on their relative fair values, as determined by the price of the undelivered items when sold separately. For revenue arrangements with multiple

deliverables, such as an arrangement that includes subscription, premium support, consulting or training services, the Company allocates the total amount the

customer will pay to the separate units of accounting based on their relative fair values, as determined by the price of the undelivered items when sold

separately.

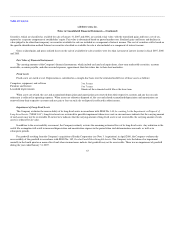

In determining whether the consulting services can be accounted for separately from subscription and support revenues, the Company considers the

following factors for each consulting agreement: availability of the consulting services from other vendors, whether objective and reliable evidence for fair

value exists for the undelivered elements, the nature of the consulting services, the timing of when the consulting contract was signed in comparison to the

subscription service start date, and the contractual dependence of the subscription service on the customer's satisfaction with the consulting work. If a

consulting arrangement does not qualify for separate accounting, the Company recognizes the consulting revenue ratably over the remaining term of the

subscription contract. Additionally, in these situations, the Company defers only the direct costs of the consulting arrangement and amortizes those costs over

the same time period as the consulting revenue is recognized. As of January 31, 2007 and 2006, the deferred cost on the accompanying consolidated balance

sheet totaled $5,232,000 and $1,686,000, respectively. These deferred costs are included in prepaid and other current assets and other assets.

66