Salesforce.com 2006 Annual Report Download - page 67

Download and view the complete annual report

Please find page 67 of the 2006 Salesforce.com annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

|

|

Table of Contents

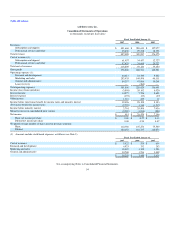

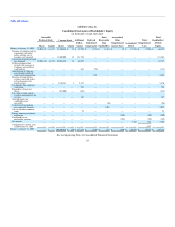

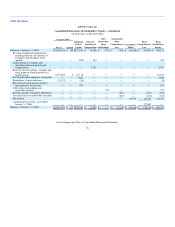

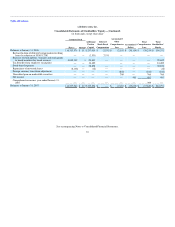

salesforce.com, inc.

Notes to Consolidated Financial Statements—(Continued)

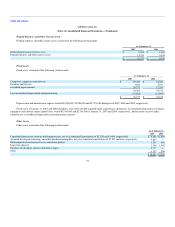

Software and Website Development Costs

The Company follows the guidance of Emerging Issues Task Force ("EITF") Issue No. 00-2, Accounting for Web Site Development Costs ("EITF

00-2"), and EITF Issue No. 00-3, Application of AICPA Statement of Position 97-2 to Arrangements That Include the Right to Use Software Stored on

Another Entity's Hardware ("EITF 00-3"). EITF 00-2 sets forth the accounting for website development costs based on the website development activity.

EITF 00-3 sets forth the accounting for software in a hosting arrangement. As such, the Company follows the guidance set forth in Statement of Position 98-1,

Accounting for the Cost of Computer Software Developed or Obtained for Internal Use ("SOP 98-1"), in accounting for the development of its on-demand

application service. SOP 98-1 requires companies to capitalize qualifying computer software costs, which are incurred during the application development

stage and amortize them over the software's estimated useful life of three years.

The Company capitalized $4,826,000, $1,352,000 and $465,000 in internal use software during fiscal 2007, 2006, and 2005, respectively. Amortization

expense totaled $750,000, $443,000 and $396,000 during fiscal 2007, 2006 and 2005, respectively.

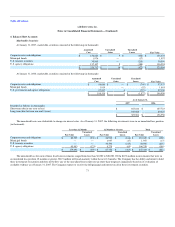

Comprehensive Income (Loss)

Comprehensive income consists of net income and other comprehensive income, which includes certain changes in equity that is excluded from net

income. Specifically, cumulative foreign currency translation and unrealized gains and losses on marketable securities adjustments, net of tax, are included in

accumulated other comprehensive loss. Comprehensive income has been reflected in stockholders' equity.

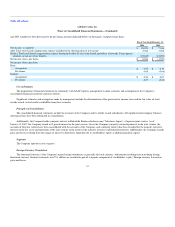

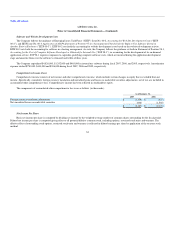

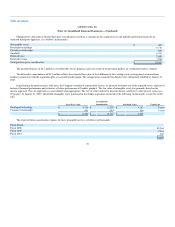

The components of accumulated other comprehensive loss were as follows (in thousands):

As of January 31,

2007 2006

Foreign currency translation adjustments $ (1,379) $ (537)

Net unrealized losses on marketable securities (808) (1,568)

$ (2,187) $ (2,105)

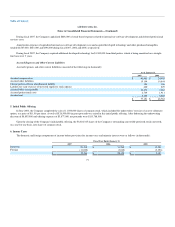

Net Income Per Share

Basic net income per share is computed by dividing net income by the weighted-average number of common shares outstanding for the fiscal period.

Diluted net income per share is computed giving effect to all potential dilutive common stock, including options, restricted stock units and warrants. The

dilutive effect of outstanding stock options, restricted stock units and warrants is reflected in diluted earnings per share by application of the treasury stock

method.

64