Saks Fifth Avenue 2008 Annual Report Download - page 80

Download and view the complete annual report

Please find page 80 of the 2008 Saks Fifth Avenue annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

86 -

87

87 -

88

88 -

89

89 -

90

90 -

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

|

|

SAKS INCORPORATED & SUBSIDIARIES

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS—(Continued)

(In thousands, except per share amounts)

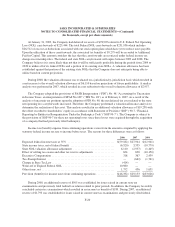

As of January 31, 2009, the Company had two potential commitments tied to the value of its common stock.

First, the Company may be required to deliver shares and/or cash to holders of the convertible notes described in

Note 6 prior to the stated maturity date of said notes based on the value of the Company’s common stock.

Second, in connection with the issuance of the convertible notes, the Company bought and sold call options to

limit the potential dilution from conversion of the notes. The Company may be required to deliver shares and/or

cash to the holders of the call options based on the value of the Company’s common stock.

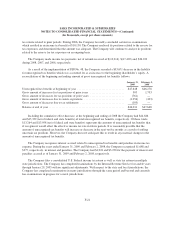

In the normal course of business, the Company purchases merchandise under purchase commitments; enters

into contractual commitments with real estate developers and construction companies for new store construction

and store remodeling; and maintains contracts for various information technology, telecommunications,

maintenance and other services. Commitments for purchasing merchandise generally do not extend beyond six

months and may be cancelable several weeks prior to the vendor shipping the merchandise. Contractual

commitments for the construction and remodeling of stores are typically lump sum or cost plus construction

contracts. Contracts to purchase various services are generally less than one to two year commitments and are

cancelable within several weeks notice.

From time to time the Company has issued guarantees to landlords under leases of stores operated by its

subsidiaries. Certain of these stores were sold in connection with the SDSG and NDSG transactions. If the

purchasers fail to perform certain obligations under the leases guaranteed by the Company, the Company could

have obligations to landlords under such guarantees. Based on the information currently available, management

does not believe that its potential obligations under these lease guarantees would be material.

LEGAL CONTINGENCIES

Vendor Litigation

On December 8, 2005 Adamson Apparel, Inc. filed a purported class action lawsuit against the Company in

the United States District Court for the Northern District of Alabama. In its complaint the plaintiff asserted

breach of contract claims and alleged that the Company improperly assessed chargebacks, timely payment

discounts, and deductions for merchandise returns against members of the plaintiff class. The lawsuit sought

compensatory and incidental damages and restitution. On June 8, 2008, the parties entered into a settlement

agreement which was approved by the United States Bankruptcy Court for the Central District of California on

July 30, 2008. Pursuant to the settlement, on August 18, 2008 the Company paid the plaintiff $370 in settlement

of the claims (of which the Company was reimbursed approximately $118 from an unrelated third party), at

which time the lawsuit was formally dismissed.

Other

The Company is involved in legal proceedings arising from its normal business activities and has accruals

for losses where appropriate. Management believes that none of these legal proceedings will have a material

adverse effect on the Company’s consolidated financial position, results of operations, or liquidity.

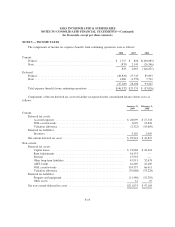

INCOME TAXES

The Company is routinely under audit by federal, state or local authorities in the areas of income taxes and

the remittance of sales and use taxes. These audits include questioning the timing and amount of deductions and

F-26