Proctor and Gamble 2011 Annual Report Download - page 8

Download and view the complete annual report

Please find page 8 of the 2011 Proctor and Gamble annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

2 -

3

3 -

4

4 -

5

5 -

6

6 -

7

7 -

8

8 -

9

9 -

10

10 -

11

11 -

12

12 -

13

13 -

14

14 -

15

15 -

16

16 -

17

17 -

18

18 -

19

19 -

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

|

|

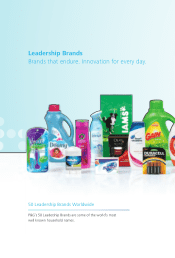

Strategic Choices Create a Winning Portfolio

We continue to take steps to strengthen P&G’s portfolio of

businesses, which enables us to focus on our greatest growth

opportunities. Two years ago, we exited our pharmaceuticals

business. This was an industry where the innovation model did

not play to P&G’s strengths, where there was little go-to-market

synergy with the rest of P&G’s businesses, and where branding

was inherently difficult and less relevant. We felt that exiting

pharmaceuticals would allow us to focus our efforts on consumer-

oriented health care, where we can more clearly apply our

Company’s strengths and where there are strong economic

and demographic tailwinds.

We are advancing this over-the-counter (OTC) focus with the

intent to form a joint venture with Teva Pharmaceutical Industries,

which we announced earlier this year. We will maintain our

North America OTC business, which generates % of our total

OTC sales. We will gain access to Teva’s manufacturing scale as

the largest prescription drug manufacturer in the world, to their

library of molecules including several prescription-to-OTC switch

portfolios, to their highly effective regulatory capabilities, and to

best-in-class pharmacy coverage in many markets. Teva will

further strengthen its position with major pharmacy customers

around the world and leverage P&G’s consumer understanding

and brand-building strengths. This partnership will allow both

companies to significantly accelerate entry into additional OTC

categories and markets.

Negotiations continue to progress well as we work to close the

transaction by the end of this calendar year.

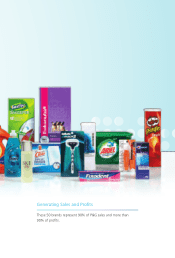

We closed the Ambi Pur acquisition and have completed a

successful integration. Through a combination of the acquisition

and organic expansions of the Febreze brand, we have grown

And, most recently, through a disciplined approach and two

rounds of negotiations, we agreed to divest Pringles to

Diamond Foods. This transaction is expected to close by the

end of calendar and will complete P&G’s exit from the

food and beverage business.

Strengthening our business portfolio is an ongoing process. We

continually evaluate the strength of our portfolio by assessing

category attractiveness across three dimensions: industry

attractiveness (market size, growth and structural economics),

competitive position (share, profitability versus industry, brand

equity/consumer purchase intent versus competition), and

portfolio fit (ability to apply the Company’s core capabilities of

brand building innovation, consumer understanding, go to

market and scale). Based on this evaluation, we believe that our

current portfolio is the strongest it has been in many years and

provides a highly strategic platform for market leadership and

sustainable growth.

These are the cornerstones of P&G’s growth strategy and our

ability to create sustainable shareholder value: innovation that

improves everyday life in every part of the world… fueled by

productivity that frees up resources to invest…in a portfolio

of businesses and brands designed for growth.

Growth Challenges

As we executed the Company’s growth strategy this past year,

we faced a number of extremely challenging external head-

winds—two of which are most important and most likely to

continue in the year ahead.

We are facing rapid and significant increases in commodity costs.

Materials and energy costs were up more than $. billion

before tax for the fiscal year. We’re taking a holistic approach

to manage these cost increases.

ō We’re turning up the dial on our productivity and

cost-savings initiatives, as indicated previously.

ō We’re creating alternative product formulations and

developing materials that use renewable feedstocks.

ō We’re reducing our dependency on commodity and

energy costs through our own and our suppliers’

sustainability efforts.

ō We’re increasing prices where necessary, coupled

with innovation where possible, to deliver the best

consumer value.

We expect commodity costs to continue escalating in the year

ahead and will remain highly disciplined to ensure we can offset

increases as fully as possible while continuing to invest in growth

and create shareholder value.

Developed markets are growing slower than expected. These

markets—principally North America, Western Europe and

Japan—account for about two-thirds of our sales. Their under-

performance reduced total Company growth by one percentage

point in fiscal year .

6The Procter & Gamble Company

our Air Care presence from markets to nearly markets.