Proctor and Gamble 2002 Annual Report Download - page 39

Download and view the complete annual report

Please find page 39 of the 2002 Proctor and Gamble annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

-

51

-

52

|

|

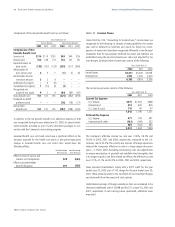

37The Procter & Gamble Company and Subsidiaries

At inception, the Company formally designates and documents the

financial instrument as a hedge of a specific underlying exposure. The

Company formally assesses, both at inception and at least quarterly on

an ongoing basis, whether the financial instruments used in hedging

transactions are effective at offsetting changes in either the fair value or

cash flows of the related underlying exposure. Fluctuations in the

derivative value are generally offset by changes in the fair value or cash

flows of the exposures being hedged. This offset is driven by the high

degree of effectiveness between the exposure being hedged and the

hedging instrument. Any ineffective portion of an instrument’s change

in fair value is immediately recognized in earnings.

Credit Risk

The Company has established strict counterparty credit guidelines and

enters into transactions only with financial institutions of investment

grade or better. Counterparty exposures are monitored daily and

downgrades in credit rating are reviewed immediately. Credit risk

arising from the inability of a counterparty to meet the terms of the

Company’s financial instrument contracts is generally limited to the

amounts, if any, by which the counterparty’s obligations exceed the

obligations of the Company. It is the Company’s policy to enter into

financial contracts with a diverse group of creditworthy counterparties.

Therefore, the Company does not expect to incur material credit losses

on its risk management or other financial instruments.

Interest Rate Management

The Company’s policy is to manage interest cost using a mix of

fixed- and variable-rate debt. To manage this risk in a cost efficient

manner, the Company enters into interest rate swaps in which the

Company agrees to exchange, at specified intervals, the difference

between fixed and variable interest amounts calculated by reference to

an agreed-upon notional principal amount.

Interest rate swaps that meet specific conditions under SFAS No. 133

are accounted for as fair value hedges. Accordingly, the changes in the

fair value of these agreements are immediately recorded in earnings.

The mark-to-market values of both the fair value hedging instruments

and the underlying debt obligations are recorded as equal and

offsetting gains and losses in the interest expense component of the

income statement. The fair value of the Company’s interest rate swap

agreements was approximately $231 at June 30, 2002 and $125 at

June 30, 2001. All existing fair value hedges are 100% effective. As a

result, there is no impact to earnings due to hedge ineffectiveness.

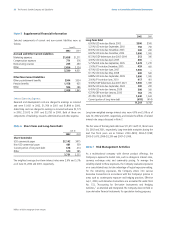

Foreign Currency Management

The Company manufactures and sells its products in a number of

countries throughout the world and, as a result, is exposed to

movements in foreign currency exchange rates. The purpose of the

Company‘s foreign currency hedging program is to reduce the risk

caused by short-term changes in exchange rates.

The Company primarily utilizes forward exchange contracts and

purchased options with maturities of less than 18 months and currency

swaps with maturities up to five years. These instruments are intended

to offset the effect of exchange rate fluctuations on forecasted sales,

inventory purchases, intercompany royalties and intercompany loans

denominated in foreign currencies. The fair value of these instruments at

June 30, 2002 and 2001 were $60 and $94 in assets and $29 and $101

in liabilities, respectively. The effective portions of the changes in fair

value for these contracts, which have been designated as cash flow

hedges, are reported in Other Comprehensive Income (OCI) and

reclassified in earnings in the same financial statement line item and in

the same period or periods during which the hedged transactions affect

earnings. The ineffective portion, which is not material for any year

presented, is immediately recognized in earnings. Qualifying cash flow

hedges currently recorded in OCI are not considered material.

The Company also utilizes the same instruments for purposes that do

not meet the requirements for hedge accounting treatment. In these

cases, the change in value offsets the foreign currency impact of inter-

company financing transactions and income from international opera-

tions. The fair value of these instruments at June 30, 2002 and 2001

was $93 in 2002 and $126 in 2001 in assets and $25 in 2002 and $6

in 2001 in liabilities, respectively. The gain or loss on these instruments

is immediately recognized in earnings. The net impact included in

marketing, research, administrative and other expense was a $31 and

$24 after-tax gain in 2002 and 2001, respectively.

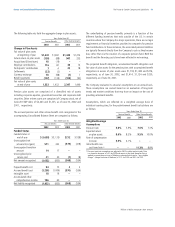

Net Investment Hedging

The Company hedges its net investment position in major currencies and

generates foreign currency interest payments that offset other transac-

tional exposures in these currencies. To accomplish this, the Company

borrows directly in foreign currency and designates a portion of foreign

currency debt as a hedge of net investments. In addition, certain foreign

currency interest rate swaps are designated as hedges of the Company’s

related foreign net investments. Under SFAS No. 133, changes in the fair

value of these instruments are immediately recognized in OCI, to offset

the change in the value of the net investment being hedged. Currency

effects of these hedges reflected in OCI were a $397 after-tax loss in

2002 and a $460 after-tax gain in 2001. Accumulated net balances

were $180 and $577 in 2002 and 2001, respectively.

Commodity Price Management

Raw materials used by the Company are subject to price volatility

caused by weather, supply conditions, political and economic variables

and other unpredictable factors. To manage the volatility related to

Notes to Consolidated Financial Statements

Millions of dollars except per share amounts