Home Depot 2010 Annual Report Download - page 43

Download and view the complete annual report

Please find page 43 of the 2010 Home Depot annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

|

|

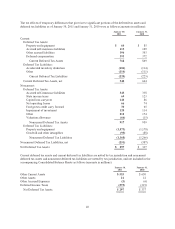

are included in Cost of Sales. The interchange fees charged to the Company for the customers’ use of the cards

and the profit sharing with the third-party administrator are included in Selling, General and Administrative

expenses (“SG&A”). The sum of the three is referred to by the Company as “the cost of credit” of the private

label credit card program.

In addition, certain subsidiaries of the Company extend credit directly to customers in the ordinary course of

business. The receivables due from customers were $42 million and $38 million as of January 30, 2011 and

January 31, 2010, respectively. The Company’s valuation reserve related to accounts receivable was not material

to the Consolidated Financial Statements of the Company as of the end of fiscal 2010 or 2009.

Merchandise Inventories

The majority of the Company’s Merchandise Inventories are stated at the lower of cost (first-in, first-out) or

market, as determined by the retail inventory method. As the inventory retail value is adjusted regularly to reflect

market conditions, the inventory valued using the retail method approximates the lower of cost or market. Certain

subsidiaries, including retail operations in Canada, Mexico and China, and distribution centers, record

Merchandise Inventories at the lower of cost or market, as determined by a cost method. These Merchandise

Inventories represent approximately 20% of the total Merchandise Inventories balance. The Company evaluates

the inventory valued using a cost method at the end of each quarter to ensure that it is carried at the lower of cost

or market. The valuation allowance for Merchandise Inventories valued under a cost method was not material to

the Consolidated Financial Statements of the Company as of the end of fiscal 2010 or 2009.

Independent physical inventory counts or cycle counts are taken on a regular basis in each store and distribution

center to ensure that amounts reflected in the accompanying Consolidated Financial Statements for Merchandise

Inventories are properly stated. During the period between physical inventory counts in stores, the Company

accrues for estimated losses related to shrink on a store-by-store basis based on historical shrink results and

current trends in the business. Shrink (or in the case of excess inventory, “swell”) is the difference between the

recorded amount of inventory and the physical inventory. Shrink may occur due to theft, loss, inaccurate records

for the receipt of inventory or deterioration of goods, among other things.

Income Taxes

Income taxes are accounted for under the asset and liability method. The Company provides for federal, state and

foreign income taxes currently payable, as well as for those deferred due to timing differences between reporting

income and expenses for financial statement purposes versus tax purposes. Deferred tax assets and liabilities are

recognized for the future tax consequences attributable to temporary differences between the financial statement

carrying amounts of existing assets and liabilities and their respective tax bases. Deferred tax assets and liabilities

are measured using enacted income tax rates expected to apply to taxable income in the years in which those

temporary differences are expected to be recovered or settled. The effect of a change in income tax rates is

recognized as income or expense in the period that includes the enactment date.

The Company recognizes the effect of income tax positions only if those positions are more likely than not of

being sustained. Recognized income tax positions are measured at the largest amount that is greater than 50%

likely of being realized. Changes in recognition or measurement are reflected in the period in which the change

in judgment occurs.

The Company and its eligible subsidiaries file a consolidated U.S. federal income tax return. Non-U.S.

subsidiaries and certain U.S. subsidiaries, which are consolidated for financial reporting purposes, are not eligible

to be included in the Company’s consolidated U.S. federal income tax return. Separate provisions for income

taxes have been determined for these entities. The Company intends to reinvest substantially all of the unremitted

earnings of its non-U.S. subsidiaries and postpone their remittance indefinitely. Accordingly, no provision for

U.S. income taxes for these non-U.S. subsidiaries was recorded in the accompanying Consolidated Statements of

Earnings.

37