GE 2009 Annual Report Download - page 74

Download and view the complete annual report

Please find page 74 of the 2009 GE annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

|

|

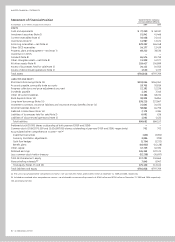

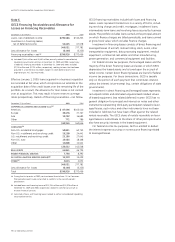

72 GE 2009 ANNUAL REPORT

INVESTMENTS IN SUBSIDIARIES AND FORMERLY CONSOLIDATED

SUBSIDIARIES. Upon a change in control that results in either

consolidation or deconsolidation of a subsidiary, the fair value

measurement of our previous equity investment or retained

noncontrolling stake in the former subsidiary, respectively, are

valued using an income approach, a market approach, or a com-

bination of both approaches as appropriate. In applying these

methodologies, we rely on a number of factors, including actual

operating results, future business plans, economic projections,

market observable pricing multiples of similar businesses and

comparable transactions, and possible control premium. These

investments are included in Level 3.

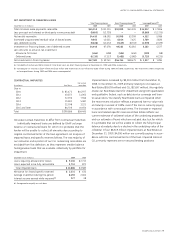

Accounting Changes

The FASB has made the Accounting Standards Codification (ASC)

effective for financial statements issued for interim and annual

periods ending after September 15, 2009. The ASC combines all

previously issued authoritative GAAP into one codified set of

guidance organized by subject area. In these financial statements,

references to previously issued accounting standards have been

replaced with the relevant ASC references. Subsequent revisions

to GAAP by the FASB will be incorporated into the ASC through

issuance of Accounting Standards Updates (ASU).

We adopted ASC 820, Fair Value Measurements and Disclosures,

in two steps; effective January 1, 2008, we adopted it for all

financial instruments and non-financial instruments accounted

for at fair value on a recurring basis and effective January 1,

2009, for all non-financial instruments accounted for at fair value

on a non-recurring basis. This guidance establishes a new frame-

work for measuring fair value and expands related disclosures.

See Note 21.

Effective January 1, 2008, we adopted ASC 825, Financial

Instruments. Upon adoption, we elected to report $172 million of

commercial mortgage loans at fair value in order to recognize

them on the same accounting basis (measured at fair value

through earnings) as the derivatives economically hedging these

loans. See Note 21.

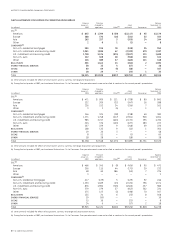

On January 1, 2009, we adopted an amendment to ASC 805,

Business Combinations. This amendment significantly changed the

accounting for business acquisitions both during the period of the

acquisition and in subsequent periods. Among the more signifi-

cant changes in the accounting for acquisitions are the following:

• Acquired in-process research and development (IPR&D) is

accounted for as an asset, with the cost recognized as the

research and development is realized or abandoned. IPR&D

was previously expensed at the time of the acquisition.

• Contingent consideration is recorded at fair value as an element

of purchase price with subsequent adjustments recognized in

operations. Contingent consideration was previously accounted

for as a subsequent adjustment of purchase price.

• Subsequent decreases in valuation allowances on acquired

deferred tax assets are recognized in operations after the

measurement period. Such changes were previously consid-

ered to be subsequent changes in consideration and were

recorded as decreases in goodwill.

• Transaction costs are expensed. These costs were previously

treated as costs of the acquisition.

• Upon gaining control of an entity in which an equity method

or cost basis investment was held, the carrying value of that

investment is adjusted to fair value with the related gain or

loss recorded in earnings. Previously, this fair value adjustment

would not have been made.

In April 2009, the FASB amended ASC 805 and changed the

previous accounting for assets and liabilities arising from contin-

gencies in a business combination. We adopted this amendment

retrospectively effective January 1, 2009. The amendment requires

pre-acquisition contingencies to be recognized at fair value, if

fair value can be determined or reasonably estimated during

the measurement period. If fair value cannot be determined or

reasonably estimated, the standard requires measurement based

on the recognition and measurement criteria of ASC 450,

Contingencies.

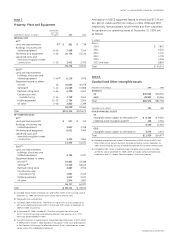

On January 1, 2009, we adopted an amendment to ASC 810

that requires us to make certain changes to the presentation of

our financial statements. This amendment requires us to classify

earnings attributable to noncontrolling interests (previously

referred to as “minority interest”) as part of consolidated net

earnings ($216 million and $641 million for 2009 and 2008,

respectively) and to include the accumulated amount of noncon-

trolling interests as part of shareowners’ equity ($7,845 million

and $8,947 million at December 31, 2009 and 2008, respectively).

The net earnings amounts we have previously reported are now

presented as “Net earnings attributable to the Company” and,

as required, earnings per share continues to reflect amounts

attributable only to the Company. Similarly, in our presentation

of shareowners’ equity, we distinguish between equity amounts

attributable to GE shareowners and amounts attributable to the

noncontrolling interests — previously classified as minority inter-

est outside of shareowners’ equity. Beginning January 1, 2009,

dividends to noncontrolling interests ($548 million in 2009) are

classified as financing cash flows. In addition to these financial

reporting changes, this guidance provides for significant changes

in accounting related to noncontrolling interests; specifically,

increases and decreases in our controlling financial interests in

consolidated subsidiaries will be reported in equity similar to

treasury stock transactions. If a change in ownership of a con-

solidated subsidiary results in loss of control and deconsolidation,

any retained ownership interests are remeasured with the gain

or loss reported in net earnings.

Effective January 1, 2009, we adopted ASC 808, Collaborative

Arrangements, that requires gross basis presentation of revenues

and expenses for principal participants in collaborative arrange-

ments. Our Technology Infrastructure and Energy Infrastructure

segments enter into collaborative arrangements with manufac-

turers and suppliers of components used to build and maintain

certain engines, aeroderivatives, and turbines, under which GE

and these participants share in risks and rewards of these product

programs. Adoption of the standard had no effect as our historical

presentation had been consistent with the new requirements.

We adopted amendments to ASC 320, Investments — Debt and

Equity Securities, and recorded a cumulative effect adjustment to

increase retained earnings as of April 1, 2009, of $62 million.