Costco 2004 Annual Report Download - page 23

Download and view the complete annual report

Please find page 23 of the 2004 Costco annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

13 -

14

14 -

15

15 -

16

16 -

17

17 -

18

18 -

19

19 -

20

20 -

21

21 -

22

22 -

23

23 -

24

24 -

25

25 -

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

|

|

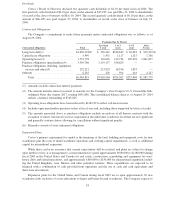

Revenue Recognition

The Company recognizes sales, net of estimated returns, at the time customers take possession of merchan-

dise or receive services. When the Company collects payment from customers prior to the transfer of ownership

of merchandise or the performance of services, the amount received is recorded as deferred revenue on the con-

solidated balance sheets until the sale or service is completed. The Company provides for estimated sales returns

based on historical returns levels.

Merchandise Inventories

Merchandise inventories are valued at the lower of cost or market as determined primarily by the retail

method of accounting and are stated using the last-in, first-out (LIFO) method for substantially all U.S. merchan-

dise inventories. Merchandise inventories for all foreign operations are primarily valued by the retail method of

accounting, and are stated using the first-in, first-out (FIFO) method. The Company believes the LIFO method

more fairly presents the results of operations by more closely matching current costs with current revenues. The

Company records an adjustment each quarter, if necessary, for the expected annual effect of inflation, and these

estimates are adjusted to actual results determined at year-end. The Company considers in its calculation of the

LIFO cost the estimated net realizable value of inventory in those inventory pools where deflation exists and re-

cords a write down of inventory where estimated net realizable value is less than LIFO inventory.

The Company provides for estimated inventory losses between physical inventory counts on the basis of a

percentage of sales. The provision is adjusted periodically to reflect the trend of the actual physical inventory

count results, which generally occur in the second and fourth fiscal quarters.

Inventory cost, where appropriate, is reduced by estimates of vendor rebates when earned or as the Com-

pany progresses towards earning those rebates provided they are probable and reasonably estimable. Other

consideration received from vendors is generally recorded as a reduction of merchandise costs upon completion

of contractual milestones, terms of agreement, or other systematic and rational approach.

Impairment of long-lived assets and warehouse closing costs

The Company periodically evaluates its long-lived assets for indicators of impairment. Management’s judg-

ments are based on market and operational conditions at the present time. Future events could cause management

to conclude that impairment factors exist, requiring an adjustment of these assets to their then-current fair market

value.

The Company provides estimates for warehouse closing costs when it is appropriate to do so based on the

applicable accounting principles generally accepted in the United States. Future circumstances may result in the

Company’s actual future closing costs or the amount recognized upon the sale of the property to differ sub-

stantially from the original estimates.

Insurance/Self Insurance Liabilities

The Company uses a combination of insurance and self-insurance mechanisms to provide for the potential

liabilities for workers’ compensation, general liability, property insurance, director and officers’ liability, vehicle

liability and employee health care benefits. Liabilities associated with the risks that are retained by the Company

are not discounted and are estimated, in part, by considering historical claims experience and outside expertise,

demographic factors, severity factors and other actuarial assumptions. The estimated accruals for these liabilities

could be significantly affected if future occurrences and claims differ from these assumptions and historical

trends.

Recent Accounting Pronouncements

In March 2004, the Financial Accounting Standards Board’s (FASB) Emerging Issues Task Force (EITF)

reached a consensus on EITF Issue No. 03-1, “The Meaning of Other-Than-Temporary Impairment and Its

Application to Certain Investments,” (EITF 03-1). The guidance prescribes a three-step model for determining

21