CVS 1998 Annual Report Download - page 20

Download and view the complete annual report

Please find page 20 of the 1998 CVS annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

10 -

11

11 -

12

12 -

13

13 -

14

14 -

15

15 -

16

16 -

17

17 -

18

18 -

19

19 -

20

20 -

21

21 -

22

22 -

23

23 -

24

24 -

25

25 -

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

|

|

18

CVS Corporation

In June 1998, the Financial Accounting Standards Board

issued Statement of Financial Accounting Standards No.

133, “Accounting for Derivative Instruments and Hedging

Activities.” This statement requires companies to record

derivative instruments on their balance sheet at fair value

and establishes new accounting practices for hedge instru-

ments. This statement is effective for years beginning after

June 15, 1999. We are in the process of determining what

impact, if any, this pronouncement will have on our consoli-

dated financial statements.

Discriminatory Pricing Litigation Against

Drug Manufacturers and Wholesalers

The Company is a party to two lawsuits that have been filed

against various pharmaceutical manufacturers and

wholesalers:

•The first lawsuit is a class action that alleges that

manufacturers and wholesalers conspired to fix

and/or stabilize the price of the prescription drugs

sold to retail pharmacies in violation of the Sherman

Antitrust Act. In this lawsuit, CVS is a member of

the plaintiff class.

•The second lawsuit was filed by individual chain

pharmacies, including Revco, as plantiffs. This

lawsuit alleges unlawful price discrimination against

retail pharmacies by manufacturers and wholesalers

in violation of the Robinson-Patman Act, and asserts

a conspiracy in violation of the Sherman Act. CVS

became a party to this lawsuit when it acquired

Revco.

With respect to the first lawsuit, fifteen defendants have

agreed to settlements totaling $720 million. The class

plaintiffs were not able to reach settlements with the four

remaining defendants. As a result, a trial of the claims was

commenced in September 1998. The trial resulted in a

directed verdict in favor of the remaining defendents. The

court has yet to approve a formula for distributing the

settlement proceeds to class members. While we believe

that our portion of the distribution could be significant, we

cannot predict an exact dollar amount at this time.

With respect to the second lawsuit, a few settlements have

been reached to date and the case is expected to go to trial in

the latter part of 1999. Our portion of any settlement or

judgment in this lawsuit could also be significant, but we

cannot predict an exact dollar amount at this time.

We further believe that our cash on hand and cash provided

by operations, together with our ability to obtain additional

short-term and long-term financing, will be sufficient to

cover our future working capital needs, capital expenditures

and debt service requirements. Please read the “Cautionary

Statement Concerning Forward-Looking Statements”

section below.

Capital Expenditures

Our capital expenditures totaled $502.3 million in 1998.

This compares to $341.6 million in 1997 and $328.9 million

in 1996. During 1998, we opened 184 new stores, relocated

198 existing stores and closed 156 stores. During 1999, we

expect that our capital expenditures will total approximately

$450-$500 million. This currently includes a plan to open

140 new stores, relocate 300 existing stores and close 130

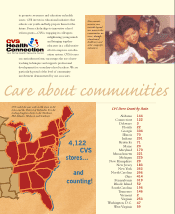

stores. As of December 31, 1998, we operated 4,122 stores

in 24 states and the District of Columbia. This compares to

4,094 stores as of December 31, 1997.

Goodwill

In connection with various acquisitions that were accounted

for as purchase transactions, we recorded goodwill, which

represented the excess of the purchase price we paid over

the fair value of the net assets we acquired. The goodwill we

recorded in these transactions is being amortized on a

straight-line basis, generally over periods of 40 years.

We evaluate goodwill for impairment whenever events or

changes in circumstances suggest that the carrying amount

may not be recoverable. Under these conditions, we would

compare our estimated future cash flows to our carrying

amounts. If our carrying amounts exceeded our expected

future cash flows, we would consider the goodwill to be

impaired and we would record an impairment loss. We do

not currently believe that any of our goodwill is impaired.

Recent Accounting Pronouncements

In March 1998, the American Institute of Certified Public

Accountants issued Statement of Position 98-1, “Accounting

for the Costs of Computer Software Developed or Obtained

for Internal Use,” effective for fiscal years beginning after

December 15, 1998. This statement defines which costs

incurred to develop or purchase internal-use software

should be capitalized and which costs should be expensed.

We are in the process of determining what impact, if any,

this pronouncement will have on our consolidated financial

statements.

Management’s Discussion and Analysis of Financial