Brother International 2012 Annual Report Download - page 30

Download and view the complete annual report

Please find page 30 of the 2012 Brother International annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

20 -

21

21 -

22

22 -

23

23 -

24

24 -

25

25 -

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

|

|

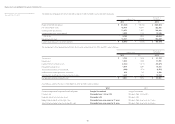

29

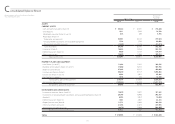

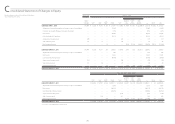

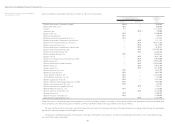

Notes to Consolidated Financial Statements

Brother Industries, Ltd. and Consolidated Subsidiaries

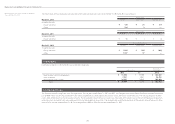

Year ended March 31, 2012 (2) Investments in Unconsolidated Subsidiaries and Associated Companies

Investments in two unconsolidated subsidiaries (two in 2011) and six associated companies (six in 2011) are accounted for by the equity method.

Investments in the remaining unconsolidated subsidiaries and associated companies are stated at cost. If these companies had been consolidated or accounted for by

the equity method, the effect on the consolidated financial statements would not have been material.

Accordingly, income from the unconsolidated subsidiaries and associated companies is recognized when the Group receives dividends. Unrealized intercompany

profits, if any, have not been eliminated in the consolidated financial statements.

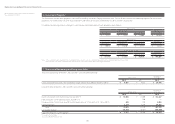

(3) Unification of Accounting Policies Applied to Foreign Subsidiaries for the Consolidated Financial Statements

On May 17, 2006, the Accounting Standards Board of Japan (the “ASBJ”) issued ASBJ Practical Issues Task Force (PITF) No.18, “Practical Solution on Unification of Accounting

Policies Applied to Foreign Subsidiaries for the Consolidated Financial Statements.” PITF No.18 prescribes: (1) the accounting policies and procedures applied to a parent

company and its subsidiaries for similar transactions and events under similar circumstances should in principle be unified for the preparation of the consolidated financial

statements, (2) financial statements prepared by foreign subsidiaries in accordance with either International Financial Reporting Standards or the generally accepted

accounting principles in the United States tentatively may be used for the consolidation process, (3) however, the following items should be adjusted in the consolidation

process so that net income is accounted for in accordance with Japanese GAAP, unless they are not material: 1) amortization of goodwill; 2) scheduled amortization of

actuarial gain or loss of pensions that has been directly recorded in the equity; 3) expensing capitalized development costs of research and development (R&D); 4) cancella-

tion of the fair value model of accounting for property, plant, and equipment and investment properties and incorporation of the cost model accounting; and 5) exclusion

of minority interests from net income, if included.

(4) Unification of Accounting Policies Applied to Associated Companies for the Equity Method

In March 2008, the ASBJ issued ASBJ Statement No.16, “Accounting Standard for Equity Method of Accounting for Investments” and ASBJ PITF No.24, “Practical Solution on

Unification of Accounting Policies Applied to Associated Companies for the Equity Method.” The new standard requires adjustments to be made to conform the associate’s

accounting policies for similar transactions and events under similar circumstances to those of the parent company when the associate’s financial statements are used in

applying the equity method unless it is impracticable to determine such adjustments. In addition, financial statements prepared by foreign associated companies in accor-

dance with either International Financial Reporting Standards or the generally accepted accounting principles in the United States tentatively may be used in applying the

equity method if the following items are adjusted so that net income is accounted for in accordance with Japanese GAAP, unless they are not material: 1) amortization of

goodwill; 2) scheduled amortization of actuarial gain or loss of pensions that has been directly recorded in the equity; 3) expensing capitalized development costs of R&D;

4) cancellation of the fair value model accounting for property, plant, and equipment and investment properties and incorporation of the cost model accounting;

and 5) exclusion of minority interests from net income, if contained.

(5) Business Combination

In October 2003, the Business Accounting Council issued a Statement of Opinion, “Accounting for Business Combinations,” and in December 2005, the ASBJ issued ASBJ

Statement No.7, “Accounting Standard for Business Divestitures” and ASBJ Guidance No.10, “Guidance for Accounting Standard for Business Combinations and Business

Divestitures.” The accounting standard for business combinations allows companies to apply the pooling of interests method of accounting only when certain specific

criteria are met such that the business combination is essentially regarded as a uniting-of-interests. For business combinations that do not meet the uniting-of-interests

criteria, the business combination is considered to be an acquisition and the purchase method of accounting is required. This standard also prescribes the accounting for

combinations of entities under common control and for joint ventures.

In December 2008, the ASBJ issued a revised accounting standard for business combinations, ASBJ Statement No.21, “Accounting Standard for Business Combinations.”

Major accounting changes under the revised accounting standard are as follows: (1) The revised standard requires accounting for business combinations only by

the purchase method. As a result, the pooling of interests method of accounting is no longer allowed. (2) The previous accounting standard required R&D costs to be

charged to income as incurred. Under the revised standard, in-process R&D costs acquired in the business combination are capitalized as an intangible asset. (3) The previ-

ous accounting standard provided for a bargain purchase gain (negative goodwill) to be systematically amortized over a period not exceeding 20 years. Under the revised

standard, the acquirer recognizes the bargain purchase gain in profit or loss immediately on the acquisition date after reassessing and confirming that all of the assets

acquired and all of the liabilities assumed have been identified after a review of the procedures used in the purchase allocation. This standard was applicable to business

combinations undertaken on or after April 1, 2010.