AT&T Uverse 2007 Annual Report Download - page 76

Download and view the complete annual report

Please find page 76 of the 2007 AT&T Uverse annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

86 -

87

-

88

|

|

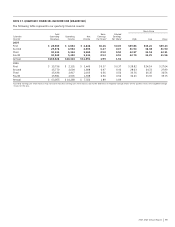

Notes to Consolidated Financial Statements (continued)

Dollars in millions except per share amounts

74

| 2007 AT&T Annual Report

A one percentage-point change in the assumed combined

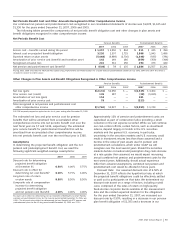

medical and dental cost trend rate would have the following

effects:

One Percentage- One Percentage-

Point Increase Point Decrease

Increase (decrease) in total

of service and interest

cost components $ 438 $ (351)

Increase (decrease) in accumulated

postretirement benefit obligation 4,314 (3,583)

For the majority of our labor contracts that contain an annual

dollar value cap for the purpose of determining contributions

required from nonmanagement retirees who retire during the

term of the labor contract, we have waived the cap during the

relevant contract periods and thus not collected contributions

from those retirees, and we have similarly waived the cap for

nonmanagement retirees who retired prior to inception of the

labor contract. Therefore, in accordance with the substantive

plan provisions required in accounting for postretirement

benefits under GAAP, we do not account for the cap in the

value of our accumulated postretirement benefit obligation

(i.e., for GAAP purposes, we assumed the cap would be

waived for all future contract periods).

Plan Assets

Plan assets consist primarily of private and public equity,

government and corporate bonds, and real estate. The asset

allocations of the pension plans are maintained to meet

ERISA requirements. Any plan contributions, as determined

by ERISA regulations, are made to a pension trust for the

benefit of plan participants. We maintain VEBA trusts to

partially fund postretirement benefits; however, there are no

ERISA or regulatory requirements that these postretirement

benefit plans be funded annually.

The principal investment objectives are: to ensure the

availability of funds to pay pension and postretirement

benefits as they become due under a broad range of future

economic scenarios; to maximize long-term investment return

with an acceptable level of risk based on our pension and

postretirement obligations; and to be broadly diversified

across and within the capital markets to insulate asset values

against adverse experience in any one market. Each asset

class has a broadly diversified style. Substantial biases

toward any particular investing style or type of security are

sought to be avoided by managing the aggregation of all

accounts with portfolio benchmarks. Asset and benefit

obligation forecasting studies are conducted periodically,

generally every two to three years, or when significant

changes have occurred in market conditions, benefits,

participant demographics or funded status. Decisions

regarding investment policy are made with an understanding

of the effect of asset allocation on funded status, future

contributions and projected expenses. The current asset

allocation policy for the pension plan is based on a study

completed during 2007. The asset allocation policy for the

VEBA assets is based on our legacy operations, and the

pre-acquisition allocation policies of ATTC and BellSouth.

It is our intention to complete an asset allocation study

during 2008.

postretirement benefit obligation of $2,492. For the year

ended December 31, 2006, we increased our discount rate

by 0.25%, resulting in a decrease in our pension plan benefit

obligation of $1,040 and a decrease in our postretirement

benefit obligation of $1,030. Should actual experience

differ from actuarial assumptions, the projected pension

benefit obligation and net pension cost and accumulated

postretirement benefit obligation and postretirement benefit

cost would be affected in future years.

Expected Long-Term Rate of Return Our expected

long-term rate of return on plan assets of 8.50% for 2008 and

2007 reflects the average rate of earnings expected on the

funds invested, or to be invested, to provide for the benefits

included in the projected benefit obligations. We consider

many factors that include, but are not limited to, historical

returns on plan assets, current market information on

long-term returns (e.g., long-term bond rates) and current and

target asset allocations between asset categories. The target

asset allocation is determined based on consultations with

external investment advisors. This assumption, which is based

on our long-term expectations of market returns in future

years, is one of the most significant of the weighted-average

assumptions used to determine our actuarial estimates of

pension and postretirement benefit expense. If all other

factors were to remain unchanged, we expect that a 1%

decrease in the expected long-term rate of return would

cause 2008 combined pension and postretirement cost to

increase $814 over 2007.

Composite Rate of Compensation Increase Our expected

composite rate of compensation increase of 4% reflects the

long-term average rate of salary increases.

Health Care Cost Trend Our health care cost trend

assumptions are developed based on historical cost data, the

near-term outlook and an assessment of likely long-term

trends. Additionally, to recognize the disproportionate growth

in prescription drug costs, we have developed separate trend

assumptions for medical and prescription drugs. In addition to

the health care cost trend, we assume an annual 3% growth

in administrative expenses and an annual 3% growth in

dental claims. Due to benefit design changes in recent years

(e.g., increased co-pays and deductibles for prescription drugs

and certain medical services), we continue to experience

better than expected claims experience. The following table

provides our assumed average health care cost trend based

on the demographics of plan participants.

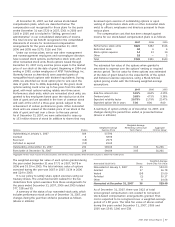

2008 2007

Health care cost trend rate assumed

for current year

Retirees 64 and under 5.76% 6.43%

Retirees 65 and over 6.36% 7.50%

Rate to which the cost trend is assumed

to decline (the ultimate trend rate) 5.00% 5.00%

Year that rate reaches the

ultimate trend rate 2010 2010