AT&T Uverse 2007 Annual Report Download - page 42

Download and view the complete annual report

Please find page 42 of the 2007 AT&T Uverse annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

|

|

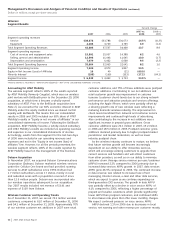

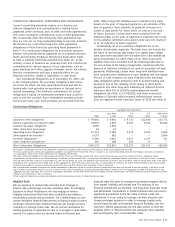

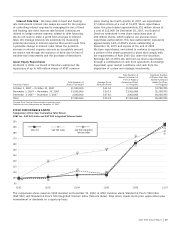

Management’s Discussion and Analysis of Financial Condition and Results of Operations (continued)

Dollars in millions except per share amounts

40

| 2007 AT&T Annual Report

order that would adopt the Joint Board’s recommendation to

cap all competitive ETC high-cost funding. If the FCC adopts

such an order, we anticipate that our company-specific cap on

high-cost support will be replaced with that industrywide cap.

Wireline

Video Service Order In March 2007, the FCC issued an

order adopting rules to implement the Cable Act’s prohibition

against local franchising authorities unreasonably refusing

to award competitive franchises for the delivery of cable

services, which it found had created unreasonable barriers to

entry that impede the goals of increasing competition and

promoting broadband deployment. This order should facilitate

our entry into the video market by reducing or removing

entry barriers posed by municipalities that have refused us

permission to use our existing right-of-ways to deploy or

activate our U-verse-related services and products. This order

does not preempt state laws that streamline the franchising

process by, for example, establishing state-wide cable

franchises. Such laws have been enacted in over half of

the states in which we operate.

Video Program Access Order In October 2007, the FCC

released an order and Further Notice of Proposed Rule Making

addressing video programming issues. The order extends

for five years the exclusive contract prohibition of the

Communications Act, which bans exclusive contracts for

satellite cable programming and satellite broadcast

programming between vertically integrated programming

vendors and cable operators. The order also improves the

FCC’s program access complaint procedures by strengthening

the discovery rules and requiring production of information

necessary to adjudicate a complaint.

Special Access In January 2005, the FCC commenced a

broad examination of the regulatory framework applicable to

interstate special access services provided by price-capped

local exchange carriers. In a July 2007 notice, the FCC invited

interested parties to update the record in that proceeding in

light of industry developments since 2005. If the FCC were

to modify this regulatory framework (such as by mandating

further reductions in special access rates), it might negatively

impact our operating results.

Broadband Forbearance Order In October 2007, the

FCC adopted an order eliminating some regulations and

certain “Computer Inquiry” rules previously applicable to

optical and packet-switched broadband transmission services

provided by our operating companies. Consequently, our

operating companies will no longer be subject to, among

other things, the FCC’s tariff filing requirements or price

cap rules for Frame Relay, ATM, Ethernet, Remote Network

Access, SONET, Optical Network or Wave-based broadband

services. This order gives us substantial flexibility to offer

individually tailored contractual arrangements that better

meet our customers’ needs while enabling us to reduce

costs and operate more efficiently.

Long-Distance Non-Dominance Order In August 2007,

the FCC adopted an order granting regulatory relief to AT&T,

Verizon Communications Inc. (Verizon) and Qwest Communi-

cations International Inc. and their independent incumbent

local exchange carrier affiliates (e.g., AT&T Connecticut).

This relief allows us to provide interstate long-distance

services free from both structural separation requirements

and dominant carrier regulation (e.g., tariffing and price cap

requirements), subject to certain limited conditions. As a result

of the FCC’s order, our business units will be able to integrate

functions across organizations and jointly plan business

operations more efficiently than previously possible. We

anticipate that this relief will lower our administrative costs

and improve our responsiveness to customers. In addition,

the FCC eliminated the equal access scripting requirement,

which had required AT&T’s customer service representatives

to inform new local telephone service customers of the

availability of long-distance service from other carriers and

to read a list of such carriers to the customer upon request.

State Regulation A summary of significant 2007 state

regulatory developments follows.

Video Service Legislation A number of states in which

we operate have adopted legislation or issued clarifying

opinions that will make it easier for telecommunications

companies to offer video service.

California High Cost Fund In June 2006, the California

Public Utilities Commission (CPUC) opened a rulemaking to

review the California High Cost Fund B (CHCF-B). The CHCF-B

program was established in 1996 and was designed to

support universal service goals by ensuring that basic

telephone service remains affordable in high-cost areas

within the service territories of the state’s major incumbent

local exchange carriers, such as our AT&T subsidiaries. In

September 2007, the CPUC adopted a decision that changed

how the CHCF-B was calculated, which we estimate will

reduce our payments from the CHCF-B by approximately

$160 in 2008 and $260 in 2009. In the same decision, the

CPUC stated that AT&T and other carriers could recover lost

payments from the fund by exercising pricing flexibility to

increase rates for services other than the basic residential

rate (such as bundles), authorized an increase in the basic

residential rate by the Consumer Price Index in 2008 and a

lifting of the existing rate cap on the basic residential rate in

2009. In a December 2007 decision in the same proceeding,

the CPUC established a $100 California Advanced Services

Fund to encourage the deployment of broadband facilities

to unserved and underserved areas of California to become

effective sometime in 2008. We are unable at this time

to determine the extent to which AT&T might be able to

qualify for payments from this fund.

COMPETITION

Competition continues to increase for telecommunications

and information services. Technological advances have

expanded the types and uses of services and products

available. In addition, lack of regulation of comparable

alternatives (e.g., cable, wireless and VoIP providers) has

lowered costs for alternative communications service

providers. As a result, we face heightened competition

as well as some new opportunities in significant portions

of our business.

Wireless

We face substantial and increasing competition in all aspects

of the wireless communications industry. Under current FCC

rules, six or more PCS licensees, two cellular licensees and