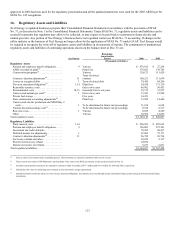

Xcel Energy 2006 Annual Report Download - page 120

Download and view the complete annual report

Please find page 120 of the 2006 Xcel Energy annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

110 -

111

111 -

112

112 -

113

113 -

114

114 -

115

115 -

116

116 -

117

117 -

118

118 -

119

119 -

120

120 -

121

121 -

122

122 -

123

123 -

124

124 -

125

125 -

126

126 -

127

127 -

128

128 -

129

129 -

130

130 -

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

|

|

110

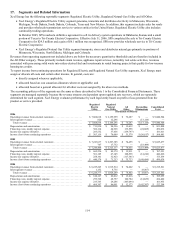

dismissal on the pleadings, which was heard on Aug. 16, 2006. In November 2006, the court issued an order denying NSP-

Minnesota’s motion. On Nov. 28, 2006, pursuant to a motion by NSP-Minnesota, the court certified the issues raised in NSP-

Minnesota’s original motion as important and doubtful. This certification permits NSP-Minnesota to file an appeal, and it has done so.

Comer vs. Xcel Energy Inc. et al. — On April 25, 2006, Xcel Energy received notice of a purported class action lawsuit filed in U.S.

District Court for the Southern District of Mississippi. The lawsuit names more than 45 oil, chemical and utility companies, including

Xcel Energy, as defendants and alleges that defendants’ CO2 “were a proximate and direct cause of the increase in the destructive

capacity of Hurricane Katrina.” Plaintiffs allege in support of their claim, several legal theories, including negligence and public and

private nuisance and seek damages related to the loss resulting from the hurricane. Xcel Energy believes this lawsuit is without merit

and intends to vigorously defend itself against these claims. On July 19, 2006, Xcel Energy filed a motion to dismiss the lawsuit in its

entirety.

Qwest vs. Xcel Energy Inc. — On June 24, 2004, an employee of PSCo, was injured when a pole, owned by Qwest malfunctioned.

The employee is seeking damages of approximately $7 million. On Sept. 6, 2005, an action against Qwest relating to incident was

filed in Denver District Court by the employee. On April 18, 2006, Qwest filed a third party complaint against PSCo based on terms in

a joint pole use agreement between Qwest and PSCo. Pursuant to this agreement, Qwest has asserted that PSCo had an affirmative

duty to properly train and instruct its employees on pole safety, including testing the pole for soundness before climbing. PSCo filed a

counterclaim on May 15, 2006, against Qwest asserting Qwest had a duty to PSCo and an obligation under the contract to maintain its

poles in a safe and serviceable condition. This case is still in the discovery phase and set for a 7 day jury trial beginning May 14, 2007.

Other Contingencies

Tax Matters — In April 2004, Xcel Energy filed a lawsuit against the U.S. government in the U.S. District Court for the District of

Minnesota to establish its right to deduct the interest expense that had accrued during tax years 1993 and 1994 on policy loans related

to the COLI policies.

After Xcel Energy filed this suit, the IRS sent two statutory notices of deficiency of tax, penalty and interest for 1995 through 1999.

Xcel Energy has filed U.S. Tax Court petitions challenging those notices. Xcel Energy anticipates the dispute relating to its interest

expense deductions will be resolved in the refund suit that is pending in the Minnesota Federal District Court and the Tax Court

petitions will be held in abeyance pending the outcome of the refund litigation. In the third quarter of 2006, Xcel Energy also received

a statutory notice of deficiency from the IRS for tax years 2000 through 2002 and timely filed a Tax Court petition challenging the

denial of the COLI interest expense deductions for those years.

On Oct. 12, 2005, the district court denied Xcel Energy’s motion for summary judgment on the grounds that there were disputed

issues of material fact that required a trial for resolution. At the same time, the district court denied the government’s motion for

summary judgment that was based on its contention that PSCo had lacked an insurable interest in the lives of the employees insured

under the COLI policies. However, the district court granted Xcel Energy’s motion for partial summary judgment on the grounds that

PSCo did have the requisite insurable interest.

On May 5, 2006, Xcel Energy filed a second motion for summary judgment. On Aug. 18, 2006, the U.S. government filed a second

motion for summary judgment. On Feb. 14, 2007, the Magistrate Judge issued his Report and Recommendation (R&R) to the Judge

concerning both motions. In his R&R the Magistrate Judge recommends both motions be denied due to fact issues in dispute. Both

parties will have an opportunity to file objections by March 5, 2007 to the Magistrate Judge’s recommendations. The Judge will then

have broad authority to, among other things, accept or reject the recommendations in whole or in part. If both sides’ motions are

ultimately denied, a trial is set to begin on July 24, 2007.

Xcel Energy believes that the tax deduction for interest expense on the COLI policy loans is in full compliance with the tax law.

Accordingly, PSRI has not recorded any provision for income tax or related interest or penalties, and has continued to take deductions

for interest expense on policy loans on its income tax returns for subsequent years. The litigation could require several years to reach

final resolution. Defense of Xcel Energy’s position may require significant cash outlays, which may or may not be recoverable in a

court proceeding. The ultimate resolution of this matter is uncertain and could have a material adverse effect on Xcel Energy’s

financial position, results of operations and cash flows.

Should the IRS ultimately prevail on this issue, tax and interest payable through Dec. 31, 2006, would reduce earnings by an estimated

$421 million. Xcel Energy has received formal notification that the IRS will seek penalties. If penalties (plus associated interest) also

are included, the total exposure through Dec. 31, 2006, is approximately $499 million. In addition, Xcel Energy’s annual earnings for

2007 would be reduced by approximately $49 million, after tax, or 11 cents per share, if COLI interest expense deductions were no

longer available.

Energy Efficiency and Renewables Law — On March 17, 2006, Governor Doyle signed into law 2005 Wisconsin Act 141 containing

the Governor’s Task Force recommendations on energy efficiency and renewables. The bill sets a statewide renewable portfolio

standard (RPS) of 10 percent by 2015 and revises the funding mechanism and administrative responsibilities for the state’s energy

efficiency program.

Two rulemaking dockets were subsequently initiated at the PSCW to provide the regulatory framework for administering this statute.

Docket 1-AC-220 will create Wisconsin Administrative Code PSC Chapter 137 to establish a structure under which energy utilities