XM Radio 1999 Annual Report Download - page 46

Download and view the complete annual report

Please find page 46 of the 1999 XM Radio annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56

|

|

44 XM RADiO

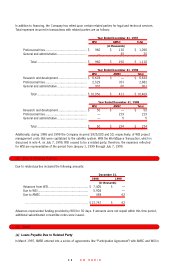

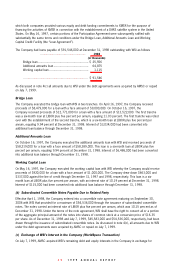

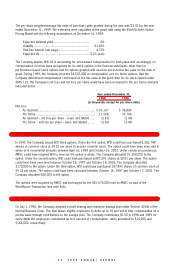

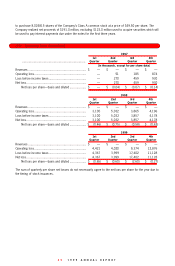

(9) Interest Cost

The Company capitalizes a portion of interest cost as a component of the cost of the FCC license and satellite

system under construction. The following is a summary of interest cost incurred during December 31, 1997, 1998

and 1999, and for the period from December 15, 1992 (date of inception) to December 31, 1999:

December 15, 1992

(date of inception) to

1997 1998 1999 December 31, 1999

(in thousands)

Interest cost capitalization.......................................... $1,901 $ 11,824 $ 15,343 $ 29,068

Interest cost charged to expense................................ 549 — 9,120 9,669

Total interest cost incurred ................................ $2,450 $ 11,824 $ 24,463 $ 38,737

Interest costs incurred prior to the award of the license were expensed in 1997. During 1999, the Company

exceeded its capitalization threshold by $3,600,000 and incurred a charge to interest of $5,520,000 for the

beneficial conversion feature of the new AMSC note.

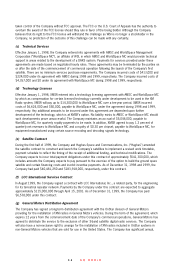

(10) Income Taxes

For the period from December 15, 1992 (date of inception) to October 8, 1999, the Company filed consolidated

federal and state tax returns with its majority stockholder AMSC. The Company generated net operating losses and

other deferred tax benefits that were not utilized by AMSC. As no formal tax sharing agreement has been finalized,

the Company was not compensated for the net operating losses. Had the Company filed on a stand-alone basis for

the three-year period ending December 31, 1999, the Company’s tax provision would be as follows:

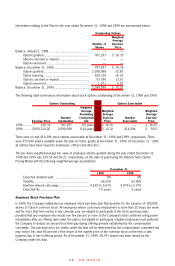

Taxes on income included in the statements of operations consists of the following:

December 31,

1997 1998 1999

(in thousands)

Current taxes:

Federal................................................................. $ — $ — $ —

State . .................................................................. — — —

Total current taxes ........................................ — — —

Deferred taxes:

Federal................................................................. — — —

State . .................................................................. — — —

Total deferred taxes ...................................... — — —

Total tax expense (benefit) ............................. $ — $ — $ —

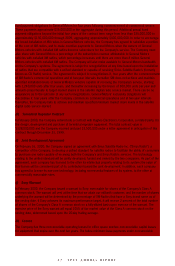

A reconciliation of the statutory tax expense, assuming all income is taxed at the statutory rate applicable to the

income and the actual tax expense is as follows:

December 31,

1997 1998 1999

(in thousands)

Income before taxes on income, as reported in the statements of income .. $ (1,659) $(16,167) $(36,896)

Theoretical tax on the above amount at 35%.............................................. (581) (5,658) (12,914)

State tax, net of federal benefit ................................................................. (165) (1,605) 701

Increase in taxes resulting from permanent differences, net ........................ — 31 2,120

Adjustments arising from differences in the basis of measurement for tax

purposes and financial reporting purposes and other ........................... — — 13,252

Change in valuation allowance ................................................................... 746 7,232 (3,159)

Taxes on income for the reported year ...................................................... $ — $ — $ —