TCF Bank 2003 Annual Report Download - page 42

Download and view the complete annual report

Please find page 42 of the 2003 TCF Bank annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

|

|

40 TCF Financial Corporation and Subsidiaries

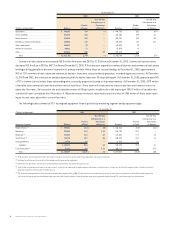

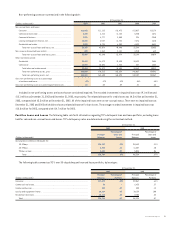

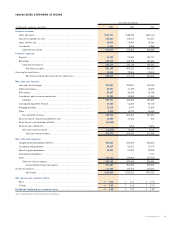

Potential problem loans and leases are summarized as follows:

At December 31, Change

(Dollars in thousands) 2003 2002 $%

Consumer . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . $– $ 4,500 $ (4,500) (100.0)%

Commercial real estate . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 20,279 30,132 (9,853) (32.7)

Commercial business . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 12,721 33,408 (20,687) (61.9)

Leasing and equipment finance . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 15,094 15,314 (220) (1.4)

Total . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . $48,094 $ 83,354 $(35,260) (42.3)

TCF’s over 30-day delinquency on total commercial real estate

decreased to less than .01% at December 31, 2003 from .37% at

December 31, 2002. The decline in delinquencies in the commercial

real estate portfolio during 2003 was primarily due to one customer

who brought their loans current in the first quarter of 2003. TCF’s

over 30-day delinquency on total leasing and equipment finance

decreased to .93% at December 31, 2003 from 1% at December 31,

2002. Included in delinquent leasing and equipment finance at

December 31, 2003 are $654 thousand of leases that have been funded

on a non-recourse basis by third-party financial institutions. At

December 31, 2002, there were no delinquent leases that have been

funded on a non-recourse basis by third-party financial institutions.

Potential Problem Loans and Leases In addition to non-

performing assets, there were $48.1 million of loans and leases at

December 31, 2003, for which management has concerns regarding

the ability of the borrowers to meet existing repayment terms,

compared with $83.4 million at December 31, 2002. These loans and

leases are primarily classified for regulatory purposes as substandard

and reflect the distinct possibility, but not probability, that the

Company will not be able to collect all amounts due according to the

contractual terms of the loan or lease agreement. Although these

loans and leases have been identified as potential problem loans

and leases, they may never become non-performing. Additionally,

these loans and leases are generally secured by commercial real

estate or assets, thus reducing the potential for loss should they

become non-performing. Potential problem loans and leases are

considered in the determination of the adequacy of the allowance

for loan and lease losses. At December 31, 2003, commercial business

potential problem loans were down $20.7 million from December 31,

2002 primarily due to paydowns received. Commercial real estate

potential problem loans totaled $20.3 million at December 31, 2003,

and were down $9.9 million from December 31, 2002, primarily due to

paydowns received and improvement in the regulatory classification

on certain loans. Leasing and equipment finance potential problem

loans include $1.1 million and $1.8 million funded on a non-recourse

basis at December 31, 2003 and 2002, respectively.

Liquidity Management TCF manages its liquidity position to

ensure that the funding needs of depositors and borrowers are met

promptly and in a cost-effective manner. Asset liquidity arises from

the ability to convert assets to cash as well as from the maturity of

assets. Liability liquidity results from the ability of TCF to attract a

diversity of funding sources to promptly meet funding requirements.

Deposits are the primary source of TCF’s funds for use in lending

and for other general business purposes. In addition to deposits, TCF

derives funds primarily from loan and lease repayments and proceeds

from the discounting of leases and borrowings. Deposit inflows and

outflows are significantly influenced by general interest rates, money

market conditions, competition for funds, customer service and

other factors. TCF’s deposit inflows and outflows have been and will

continue to be affected by these factors. Borrowings may be used

to compensate for reductions in normal sources of funds, such as

deposit inflows at less than projected levels, net deposit outflows

or to support expanded activities. Historically, TCF has borrowed

primarily from the FHLB, from institutional sources under repurchase

agreements and, to a lesser extent, from other sources. At

December 31, 2003, TCF had over $2.4 billion in unused capacity

under these funding sources, which could be used to meet future

liquidity needs. See “Borrowings.”

Potential sources of liquidity for TCF Financial Corporation

(parent company only) include cash dividends from TCF’s wholly

owned bank subsidiary, issuance of equity securities and borrowings

under a $105 million line of credit. TCF’s National Bank’s ability to

pay dividends or make other capital distributions to TCF is restricted

by regulation and may require regulatory approval. Undistributed

earnings and profits at December 31, 2003 includes approximately

$134.4 million for which no provision for federal income tax has

been made. This amount represents earnings appropriated to bad

debt reserves and deducted for federal income tax purposes, and is

generally not available for payment of cash dividends or other dis-

tributions to shareholders without incurring an income tax liability

based on the amount of earnings removed and current tax rates.