Porsche 2006 Annual Report Download - page 139

Download and view the complete annual report

Please find page 139 of the 2006 Porsche annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

129 -

130

130 -

131

131 -

132

132 -

133

133 -

134

134 -

135

135 -

136

136 -

137

137 -

138

138 -

139

139 -

140

140 -

141

141 -

142

142 -

143

143 -

144

144 -

145

145 -

146

146 -

147

147 -

148

148 -

149

149 -

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

|

|

137

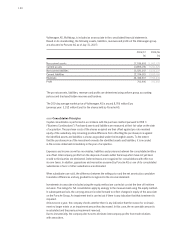

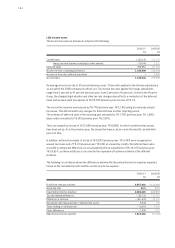

Pension provisions

The provisions for pensions and similar obligations are determined using the projected unit credit method.

This method considers not only the pensions and future claims known on the balance sheet date but also

future anticipated increases in salaries and pensions. If pension obligations are reinsured using plan assets

they are disclosed on a net basis.

The calculation is based on actuarial assumptions about biometric data. The company uses the corridor

rule to measure the pension commitments and determine the pension expenses. Actuarial gains and

losses are not taken into account provided they do not exceed ten percent of the commitment or ten

percent of the fair value of the existing plan assets. The amount in excess of the corridor is distributed

over the average residual service period of the active workforce and recorded in profit or loss.

Past service cost is recognized on a straight-line basis over the average period until the benefits become

vested. If the benefits are already vested immediately following the introduction of, or changes to, a

pension plan, past service cost is recognized immediately in profit or loss.

Service cost is disclosed in personnel expenses while the interest portion of the addition to the provision

and income from plan assets is recorded in the financial result. The interest rate used to discount pro-

visions is determined on the basis of the return on long-term high-quality corporate bonds on the balance

sheet date.

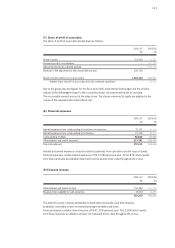

Other provisions

Other provisions are set up if there is a current legal or constructive obligation to third parties which is

expected to lead to a future outflow of resources that can be estimated reliably.

Provisions for warranty claims are set up taking account of the past or estimated future claims pattern.

Non-current provisions are stated at their settlement amount discounted to balance sheet date. The

interest rate used is a pre-tax rate that reflects current market assessments of the time value of money

and the risks specific to the liability. The interest expense resulting from the write-up is recognized in

financial expenses.

Income and expenses

Income is generally recognized to the extent that it is probable that the economic benefits will flow

to the Group and the income can be reliably measured.

Income from the sale of products is generally not recognized until the point in time when the significant

opportunities and risks associated with ownership of the goods and products being sold is transferred

to the buyer. Income is reported net of discounts, customer bonuses and rebates.

In the case of long-term construction costs income is recognized in accordance with the degree of

completion. Interest income is recognized as interest accrues.

Dividend income is recognized when the Group’s right to receive the payment is established.

Production-related expenses are recognized upon delivery or utilization of the service, while all other

expenses are recognized as an expense as incurred. The same applies for non-capitalizable development

costs. Provisions for warranty claims are recognized at the time of sale of the products. Interest and other

borrowing costs are recorded as an expense in the same period. Interest expenses incurred for financial

services are disclosed under cost of materials.