NVIDIA 2009 Annual Report Download - page 57

Download and view the complete annual report

Please find page 57 of the 2009 NVIDIA annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

|

|

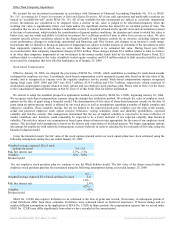

On January 29, 2007, we adopted FASB Interpretation No. 48, or FIN 48, Accounting for Uncertainty in Income Taxes, issued in

July 2006. FIN 48 applies to all tax positions related to income taxes subject to SFAS No. 109. Under FIN 48 we recognize the benefit

from a tax position only if it is more-likely-than-not that the position would be sustained upon audit based solely on the technical

merits of the tax position. The cumulative effect of adoption of FIN 48 did not result in a material adjustment to our tax liability for

unrecognized income tax benefits. Our policy to include interest and penalties related to unrecognized tax benefits as a component of

income tax expense did not change as a result of implementing the FIN 48. Please refer to Note 13 of these Notes to the Consolidated

Financial Statements in Part IV, Item 15 of this Form 10-K for additional information.

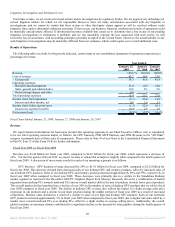

Goodwill

Our impairment review process compares the fair value of the reporting unit in which the goodwill resides to its carrying value.

We determined that our reporting units are equivalent to our operating segments or components of an operating segment for the

purposes of completing our Statement of Financial Accounting Standards No. 142, or SFAS No. 142, Goodwill and Other Intangible

Assets, impairment test. We utilize a two-step approach to testing goodwill for impairment. The first step tests for possible

impairment by applying a fair value-based test. In computing fair value of our reporting units, we use estimates of future revenues,

costs and cash flows from such units. The second step, if necessary, measures the amount of such impairment by applying fair

value-based tests to individual assets and liabilities. Goodwill is subject to our annual impairment test during the fourth quarter of our

fiscal year, or earlier if indicators of potential impairment exist, using a fair value-based approach. We completed our most recent

annual impairment test during the fourth quarter of fiscal year 2009 and concluded that there was no impairment. This assessment is

based upon a discounted cash flow analysis and analysis of our market capitalization. The estimate of cash flow is based upon, among

other things, certain assumptions about expected future operating performance such as revenue growth rates and operating margins

used to calculate projected future cash flows, risk-adjusted discount rates, future economic and market conditions, and determination

of appropriate market comparables. Our estimates of discounted cash flows may differ from actual cash flows due to, among other

things, economic conditions, changes to our business model or changes in operating performance. Additionally, certain estimates of

discounted cash flows involve businesses with limited financial history and developing revenue models, which increase the risk of

differences between the projected and actual performance. Significant differences between these estimates and actual cash flows could

materially affect our future financial results. These factors increase the risk of differences between projected and actual performance

that could impact future estimates of fair value of all reporting units. In addition, determining the number of reporting units and the

fair value of a reporting unit requires us to make judgments and involves the use of significant estimates and assumptions. We also

make judgments and assumptions in allocating assets and liabilities to each of our reporting units. We base our fair value estimates on

assumptions we believe to be reasonable but that are unpredictable and inherently uncertain. The long-term financial forecast

represents the best estimate that we have at this time and we believe that its underlying assumptions are reasonable. However, actual

performance in the near-term and longer-term could be materially different from these forecasts, which could impact future estimates

of fair value of our reporting units and may result in a charge to earnings in future periods due to the potential for a write-down of

goodwill in connection with such tests.

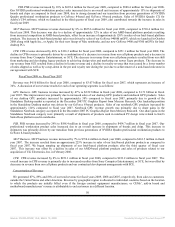

Cash Equivalents and Marketable Securities

Fair Value

In the current market environment, the assessment of the fair value of debt instruments can be difficult and subjective. The volume

of trading activity of certain debt instruments has declined, and the rapid changes occurring in today’s financial markets can lead to

changes in the fair value of financial instruments in relatively short periods of time. Statement of Financial Accounting Standards No.

157, or SFAS No. 157, Fair Value Measurements, establishes three levels of inputs that may be used to measure fair value. Please

refer to Note 17 of the Notes to the Consolidated Financial Statements in Part IV, Item 15 of this Form 10-K. We measure our cash

equivalents and marketable securities at fair value. The fair values of our financial assets and liabilities are determined using quoted

market prices of identical assets or quoted market prices of similar assets from active markets. Level 1 valuations are obtained from

real-time quotes for transactions in active exchange markets involving identical assets. Level 2 valuations are obtained from quoted

market prices in active markets involving similar assets. Level 3 valuations are based on unobservable inputs to the valuation

methodology and include our own data about assumptions market participants would use in pricing the asset or liability based on the

best information available under the circumstances. Each level of input has different levels of subjectivity and difficulty involved in

determining fair value. While most of our cash equivalents and marketable securities are valued based on Level 2 inputs, the valuation

of our holdings of the Reserve International Liquidity Fund, Ltd., or International Reserve Fund are classified as a Level 3 input due to

the inherent subjectivity and the significant judgment involved in its valuation. Total financial assets at fair value classified within

Level 3 were 3.7% of total assets on our Consolidated Balance Sheet as of January 25, 2009.

47

Source: NVIDIA CORP, 10-K, March 13, 2009 Powered by Morningstar® Document Research℠