Seagate 2002 Annual Report Download - page 74

Download and view the complete annual report

Please find page 74 of the 2002 Seagate annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

|

|

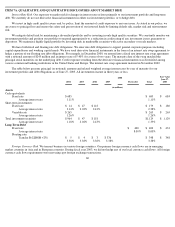

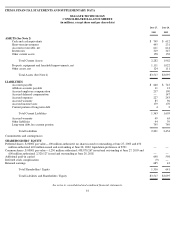

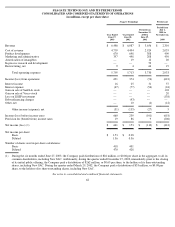

SEAGATE TECHNOLOGY AND ITS PREDECESSOR

NOTES TO CONSOLIDATED AND COMBINED FINANCIAL STATEMENTS—(CONTINUED)

Critical Accounting Policies and Use of Estimates —The preparation of financial statements in conformity with accounting principles

generally accepted in the United States requires management to make estimates and assumptions that affect the amounts reported in the

financial statements and accompanying notes. Actual results could differ materially from those estimates.

The Company establishes certain distributor and original equipment manufacturer sales programs aimed at increasing customer demand.

These programs are typically related to a distributor’s level of sales, order size, advertising or point of sale activity or an OEM’s level of sale

activity or agreed upon rebate programs. The Company provides for these obligations at the time that revenue is recorded based on estimated

requirements. These estimates are based on various factors, including estimated future price erosion, distributor sell-through levels, program

participation and customer claim submittals. Significant variations in any of these factors could have a material effect on the Company’s

operating results.

The Company’s warranty provision considers estimated product failure rates, trends and estimated repair or replacement costs. The

Company uses a statistical model to help the Company with its estimates and the Company exercises considerable judgment in determining the

underlying estimates. Should actual experience in any future period differ significantly from its estimates, or should the rate of future product

technological advancements fail to keep pace with the past, the Company’s future results of operations could be materially affected. The actual

results with regard to warranty expenditures could have a material adverse effect on the Company if the actual rate of unit failure or the cost to

repair a unit is greater than that which the Company has used in estimating the warranty expense accrual.

The Company’s recording of deferred tax assets each period depends primarily on the Company’s ability to generate current and future

taxable income in the United States. Each period the Company evaluates the need for a valuation allowance for the deferred tax assets and

adjusts the valuation allowance so that net deferred tax assets are recorded only to the extent the Company concludes it is more likely than not

that the assets will be realized.

The Company also has other key accounting policies and accounting estimates relating to uncollectible customer accounts and valuation

of inventory. The Company believes that these other accounting policies and other accounting estimates either do not generally require it to

make estimates and judgments that are as difficult or as subjective, or it is less likely that they would have a material impact on its reported

results of operations for a given period.

Basis of Consolidation

—The consolidated financial statements include the accounts of the Company and all its wholly-owned subsidiaries,

after eliminations of intercompany transactions and balances.

The Company operates and reports financial results on a fiscal year of 52 or 53 weeks ending on the Friday closest to June 30.

Accordingly, fiscal year 2001 comprised 52 weeks for the combined Company and Predecessor and ended on June 29, 2001. Fiscal years 2002

and 2003 both comprised 52 weeks and ended on June 28, 2002 and June 27, 2003, respectively. All references to years in these notes to

consolidated financial statements represent fiscal years unless otherwise noted. Fiscal year 2004 will be 53 weeks and will end on July 2, 2004.

Reclassifications —In fiscal year 2001, certain costs aggregating $10 million for the period from November 23, 2000 to June 29, 2001

and $72 million for the period from July 1, 2000 to November 22, 2000, associated with: (1) searching for or evaluating product or process

alternatives: (2) modifying the formulation or design of products or processes; and (3) activities required to advance the design of products that

were previously classified by the Predecessor in cost of revenue were reclassified to product development.

Foreign Currency Remeasurement and Translation —The U.S. dollar is the functional currency for most of the Company’s foreign

operations. Gains and losses on the remeasurement into U.S. dollars of amounts denominated in foreign currencies are included in net income

(loss) for those operations whose functional currency is the U.S. dollar and translation adjustments are included in other comprehensive income

(loss) and as accumulated other comprehensive income (loss), a separate component of shareholders’ equity (business equity for the

Predecessor), for those operations whose functional currency is the local currency.

Derivative Financial Instruments —The Company applies the requirements of Statement of Financial Accounting Standards (“SFAS”)

No. 133,

“Accounting for Derivative Instruments and Hedging Activities” (“SFAS 133”). The standard requires that all derivatives be recorded

on the balance sheet at fair value and establishes criteria for designation and effectiveness of hedging relationships.

68