Regions Bank 2011 Annual Report Download - page 202

Download and view the complete annual report

Please find page 202 of the 2011 Regions Bank annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

192 -

193

193 -

194

194 -

195

195 -

196

196 -

197

197 -

198

198 -

199

199 -

200

200 -

201

201 -

202

202 -

203

203 -

204

204 -

205

205 -

206

206 -

207

207 -

208

208 -

209

209 -

210

210 -

211

211 -

212

212 -

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

|

|

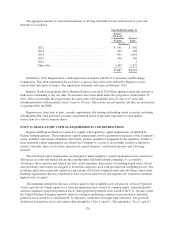

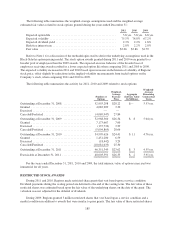

The aggregate amount of contractual maturities of all long-term debt in each of the next five years and

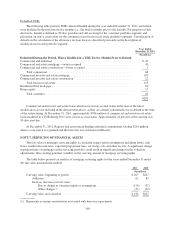

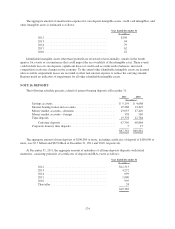

thereafter is as follows:

Year Ended December 31

Regions

Financial

Corporation

(Parent)

Regions

Bank

(In millions)

2012 .......................................... $ 951 $ 902

2013 .......................................... 250 498

2014 .......................................... 695 1,001

2015 .......................................... 496 348

2016 .......................................... — 2

Thereafter ...................................... 1,495 1,472

$3,887 $4,223

In February 2010, Regions filed a shelf registration statement with the U.S. Securities and Exchange

Commission. This shelf registration does not have a capacity limit and can be utilized by Regions to issue

various debt and equity securities. The registration statement will expire in February 2013.

Regions’ Bank Note program allows Regions Bank to issue up to $20 billion aggregate principal amount of

bank notes outstanding at any one time. No issuances have been made under this program as of December 31,

2011. Notes issued under the program may be senior notes with maturities from 30 days to 15 years and

subordinated notes with maturities from 5 years to 30 years. These notes are not deposits and they are not insured

or guaranteed by the FDIC.

Regions may, from time to time, consider opportunistically retiring outstanding issued securities, including

subordinated debt, trust preferred securities and preferred shares in privately negotiated or open market

transactions for cash or common shares.

NOTE 13. REGULATORY CAPITAL REQUIREMENTS AND RESTRICTIONS

Regions and Regions Bank are required to comply with regulatory capital requirements established by

Federal banking agencies. These regulatory capital requirements involve quantitative measures of the Company’s

assets, liabilities and certain off-balance sheet items, and also qualitative judgments by the regulators. Failure to

meet minimum capital requirements can subject the Company to a series of increasingly restrictive regulatory

actions. Currently, there are two basic measures of capital adequacy: a risk-based measure and a leverage

measure.

The risk-based capital requirements are designed to make regulatory capital requirements more sensitive to

differences in credit and market risk profiles among banks and bank holding companies, to account for

off-balance sheet exposure and interest rate risk, and to minimize disincentives for holding liquid assets. Assets

and off-balance sheet items are assigned to broad risk categories, each with specified risk-weighting factors. The

resulting capital ratios represent capital as a percentage of total risk-weighted assets and off-balance sheet items.

Banking organizations that are considered to have excessive interest rate risk exposure are required to maintain

higher levels of capital.

The minimum standard for the ratio of total capital to risk-weighted assets is 8 percent. At least 50 percent

of that capital level (which equates to a 4 percent minimum) must consist of common equity, undivided profits

and non-cumulative perpetual preferred stock, senior perpetual preferred stock issued to the U.S. Treasury under

the Capital Purchase Program, minority interests relating to qualifying common or noncumulative perpetual

preferred stock issued by a consolidated U.S. depository institution or foreign bank subsidiary, less goodwill,

disallowed deferred tax assets and certain other intangibles (“Tier 1 capital”). The remainder (“Tier 2 capital”)

178