Redbox 2005 Annual Report Download - page 29

Download and view the complete annual report

Please find page 29 of the 2005 Redbox annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

19 -

20

20 -

21

21 -

22

22 -

23

23 -

24

24 -

25

25 -

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

|

|

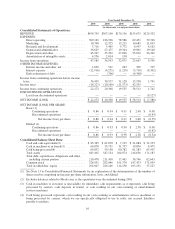

On December 1, 2005, we invested $20.0 million to obtain a 47.3% interest in Redbox. We are accounting

for our ownership under the equity method in our consolidated financial statements. Our 47.3% interest in this

investment includes a conditional consideration agreement to contribute an additional $12.0 million if Redbox

achieves certain targets within a one year period.

On August 5, 2005, we entered into a credit agreement to provide DVDXpress with a $4.5 million credit

facility. Loans made pursuant to the credit agreement are secured by a first security interest in substantially all of

DVDXpress’ assets as well as a pledge of their capital stock. Interest on the unpaid balance of the loan will bear

interest at an annual rate equal to LIBOR plus three percent. As of December 31, 2005, DVDXpress has drawn

down $3.5 million on this credit facility. Additionally, on December 7, 2005 we signed an asset purchase option

agreement that allows Coinstar to purchase substantially all of DVDXpress’ business assets and liabilities in

exchange for any outstanding debt and accrued interest on the credit facility plus $10,000 and contingent

consideration of up to $3.5 million based on achievement of specific conditions. Effective December 7, 2005, we

have consolidated the fair value of DVDXpress’ financial results into our consolidated financial statements in

accordance with FASB Interpretation No. 46 (revised December 2003), Consolidation of Variable Interest

Entities (“FIN 46R”).

On July 7, 2004, we entered into a senior secured credit facility to finance our acquisition of ACMI. This

facility provided for advances totaling up to $310.0 million, consisting of a $60.0 million revolving credit facility

and a $250.0 million term loan facility. Fees for this facility of approximately $5.7 million are being amortized

over the life of the revolving line of credit and the term loan which are 5 years and 7 years, respectively. Loans

under this facility are secured by a first security interest in substantially all of our assets and the assets of our

subsidiaries, as well as a pledge of our subsidiaries’ capital stock. The credit facility matures on July 7, 2011. As

of December 31, 2005, our original term loan balance of $250.0 million had been reduced to $205.8 million.

Advances under this credit facility may be made as either base rate loans (the higher of the Prime Rate or

Federal Funds Effective Rate) or LIBOR rate loans at our election. Applicable interest rates are based upon either

the LIBOR or base rate plus an applicable margin dependent upon a consolidated leverage ratio of outstanding

indebtedness to EBITDA (to be calculated in accordance with the terms specified in the credit agreement). Our

consolidated leverage ratios are based upon either LIBOR plus 200 basis points or the base rate plus 100 basis

points. At December 31, 2005, our interest rate on this facility was 6.1%. On January 7, 2006, due to increases in

the LIBOR rate, our interest rate was adjusted to 6.55%.

The credit facility contains standard negative covenants and restrictions on actions by us including, without

limitation, restrictions on indebtedness, liens, fundamental changes or dispositions of our assets, payments of

dividends or common stock repurchases, capital expenditures, foreign investments, acquisitions, sale and

leaseback transactions and swap agreements, among other restrictions. In addition, the credit agreement requires

that we meet certain financial covenants, ratios and tests, including maintaining a maximum consolidated

leverage ratio and a minimum interest coverage ratio, as defined in the agreement. As of December 31, 2005, we

were in compliance with all covenants.

Quarterly principal payments on the term loan of $0.5 million terminate on March 31, 2011. The remaining

principal balance of $194.8 million will be due July 7, 2011, the maturity date of the facility. Commitment fees

on the unused portion of the facility, currently 50 basis points, may vary and are based on our consolidated

leverage ratio.

On September 23, 2004, we purchased an interest rate cap and sold an interest rate floor at zero net cost,

which protects us against certain interest rate fluctuations of the LIBOR rate, on $125.0 million of our variable

rate debt under our credit facility. The interest rate cap and floor became effective on October 7, 2004 and

expires after three years on October 9, 2007. The interest rate cap and floor consists of a LIBOR ceiling of 5.18%

and a LIBOR floor that steps up in each of the three years beginning October 7, 2004, 2005 and 2006. The

LIBOR floor rates are 1.85%, 2.25% and 2.75% for each of the respective three-year periods. Under this interest

25