Qantas 2009 Annual Report Download - page 91

Download and view the complete annual report

Please find page 91 of the 2009 Qantas annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

86 -

87

87 -

88

88 -

89

89 -

90

90 -

91

91 -

92

92 -

93

93 -

94

94 -

95

95 -

96

96 -

97

97 -

98

98 -

99

99 -

100

100 -

101

101 -

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

|

|

89 Qantas Annual Report 2009

Notes to the Financial Statements

for the year ended 30 June 2009

1. Statement of Significant Accounting Policies

Qantas Airways Limited (Qantas) is a company limited by shares,

incorporated in Australia whose shares are publicly traded on the

Australian Stock Exchange (ASX) and which is subject to the operation of

the Qantas Sale Act as described in the Corporate Governance Statement.

The consolidated Financial Report of Qantas for the year ended 30 June

2009 comprises Qantas and its controlled entities (together referred to as

the Qantas Group) and the Qantas Group’s interest in associates and jointly

controlled entities.

The Financial Report of Qantas for the year ended 30 June 2009 was

authorised for issue in accordance with a resolution of the Directors on

31 August 2009.

(A) STATEMENT OF COMPLIANCE

The Financial Report is a general purpose financial report which has been

prepared in accordance with Australian Accounting Standards (AASBs)

adopted by the Australian Accounting Standards Board and the

Corporations Act 2001. The Financial Report also complies with

International Financial Reporting Standards (IFRSs) and interpretations

adopted by the International Accounting Standards Board.

(B) BASIS OF PREPARATION

The Financial Report is presented in Australian dollars and has been

prepared on the basis of historical costs except in accordance with relevant

accounting policies where assets and liabilities are stated at their fair

values. Assets classified as held for sale are stated at the lower of carrying

amount and fair value less costs to sell.

Qantas is a company of the kind referred to in Australian Securities and

Investments Commission (ASIC) Class Order 98/100 dated 10 July 1998

(updated by CO 05/641 effective 28 July 2005 and CO 06/51 effective

31 January 2006) and in accordance with the Class Order, amounts in the

Financial Report have been rounded to the nearest million dollars, unless

otherwise stated.

The accounting policies set out below have been consistently applied to

all periods presented in the consolidated Financial Report.

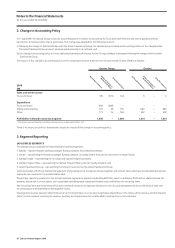

The following standards, amendments to standards and interpretations

have been identified as those which may impact Qantas in the period of

initial application. They are available for early adoption at 30 June 2009,

but have not been applied in preparing this financial report.

•RevisedAASB3BusinessCombinations(2008)incorporatesthe

following changes that are likely to be relevant to the Qantas

Group’s operations:

– contingent consideration will be measured at fair value, with

subsequent changes therein recognised in profit or loss;

– transaction costs, other than share and debt issue costs, will be

expensed as incurred;

– any pre-existing interest in the acquiree will be measured at either

fair value, or at its proportionate interest in the identifiable assets

and liabilities of the acquiree, on a transaction-by-transaction basis.

Revised AASB 3, which becomes mandatory for the Qantas Group’s

30 June 2010 financial statements, will be applied prospectively and

therefore there will be no impact on prior periods.

•AmendedAASB127ConsolidatedandSeparateFinancialStatements

(2008) requires accounting for changes in ownership interests by the

Group in a subsidiary, while maintaining control, to be recognised as

an equity transaction. When the Group loses control of a subsidiary,

any interest retained in the former subsidiary will be measured at fair

value with the gain or loss recognised in profit or loss. The Qantas

Group has not yet determined the effect of the amendments to AASB

127, which becomes mandatory for the Qantas Group’s 30 June 2010

financial statements.

•AASB8OperatingSegmentsintroducesthe‘managementapproach’to

segment reporting. AASB 8, which becomes mandatory for the Qantas

Group’s 30 June 2010 financial statements, will require a change in the

presentation on and disclosure of segment information based on the

internal reports regularly reviewed by the Qantas Group’s Chief

Operating Decision Maker in order to assess each segment’s performance

and to allocate resources to them. Currently, the Qantas Group presents

segment information in respect of its business and geographical

segments. Under the management approach, it is anticipated that

the segments disclosed will match the business segments in the

current disclosures.

•RevisedAASB101PresentationofFinancialStatements(2007)and

consequential amendments in AASB 2009-6 Amendments to Australian

Accounting Standards, introduces the term total comprehensive income,

which represents changes in equity during a period other than those

changes resulting from transactions with owners in their capacity as

owners. Total comprehensive income may be presented in either a single

statement of comprehensive income (effectively combining both the

income statement and all non-owner changes in equity in a single

statement) or, in an income statement and a separate statement of

comprehensive income. Revised A ASB 101, which becomes mandatory

for the Qantas Group’s 30 June 2010 financial statements, is expected to

have an impact on the presentation of the Qantas Group’s financial

statements with respect to non-owner changes in equity.

•AASB2008-1AmendmentstoAustralianAccountingStandard–Share-

based Payments: Vesting Conditions and Cancellations clarifies the

definition of vesting conditions, introduces the concept of non-vesting

conditions, requires non-vesting conditions to be reflected in grant-date

fair value and provides the accounting treatment for non-vesting

conditions and cancellations. The amendments to AASB 2 Share-based

Payment will become mandatory for the Qantas Group’s 30 June 2010

financial statements, with retrospective applications. The Qantas Group

has not yet determined the potential impact of the amendment.

•AASB2008-5AmendmentstoAustralianAccountingStandardsarising

from the Annual Improvements Project and 2008-6 Further

Amendments to Australian Accounting Standards arising from the

Annual Improvements Project, AASB 2009-4 Amendments to Australian

Accounting Standards arising from the Annual Improvements Project and

AASB 2009-5 Further Amendments to Australian Accounting Standards

arising from the Annual Improvements Project affect various AASBs

resulting in minor changes for presentation, disclosure, recognition and

measurement purposes. The amendments, which become mandatory for

the Qantas Group’s 30 June 2010 financial statements, except for AASB

2009-5 which becomes mandatory for the Qantas Group’s 30 June 2011

financial statements, are not expected to have any impact on the

financial statements.

•AASB2008-7AmendmentstoAccountingStandards–Costofan

Investment in a Subsidiary, Jointly Controlled Entity or Associate changes

the recognition and measurement of dividends received as income and

addresses the accounting of a newly formed parent entity in the separate

financial statements. The amendments become mandatory for the

Qantas Group’s 30 June 2010 financial statements. The Qantas Group

has not yet determined the potential effect of the amendments.

•AASB2008-8AmendmentstoAustralianAccountingStandards–

Eligible Hedge Items clarifies the effect of using options as hedging

instruments and the circumstances in which inflation risk can be hedged.

The amendments become mandatory for the Qantas Group’s 30 June

2010 financial statements, with retrospective application. The Qantas

Group has not yet determined the potential effect of the amendments.