Proctor and Gamble 1999 Annual Report Download - page 20

Download and view the complete annual report

Please find page 20 of the 1999 Proctor and Gamble annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

10 -

11

11 -

12

12 -

13

13 -

14

14 -

15

15 -

16

16 -

17

17 -

18

18 -

19

19 -

20

20 -

21

21 -

22

22 -

23

23 -

24

24 -

25

25 -

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

|

|

FINANCIAL REVIEW (CONTINUED)

16

The Procter & Gamble Company and Subsidiaries

Total debt was up $1.33 billion to $9.38 bil-

lion, due to the issuance of commercial paper and

long-term debt to fund share repurchases.

Long-term borrowing available under the

Company’s shelf registration statement filed in

1995, as amended in July 1997, was $1.18 billion

at June 30, 1999. Additionally, the Company has

the ability to issue commercial paper at favorable

rates, and to access general bank financing.

The following pages provide perspective on

the Company’s geographic operating segments.

Geographic segments exclude items that are not

included in measuring business performance, most

notably certain financing and employee benefit

costs, goodwill amortization, corporate elimina-

tions, certain asset write-downs and costs related

to the Company’s Organization 2005 and simpli-

fication and standardization programs.

NORTH AMERICA REGION

The North America region delivered record

results for the fiscal year, spurred by initiative

activity and share growth.

Net sales for the year were $18.98 billion,

an increase of 3% from the prior year level of

$18.46 billion, on broad-based unit volume

growth of 2%. Net sales in 1998 increased 5%

over 1997, on 4% unit volume growth.

Net earnings for the region were up 10% to

$2.71 billion. The region achieved earnings

growth through volume gains, continued focus

on cost control, pricing and value-added ini-

tiatives, particularly in laundry and cleaning

products and in paper. Prior year net earnings

were $2.47 billion, which represented a 10%

increase over 1997. Net earnings margin for the

region was 14.3%, compared to 13.4% and

12.8% in 1998 and 1997, respectively.

The laundry and cleaning sector led the

region’s current year volume progress, generating

5% unit volume growth versus the prior year. The

reformulation of Tide for sanitization and clean

rinse benefits, the launch of Febreze fabric

refresher and strong base business performance

drove volume gains and increased share. Febreze,

introduced late in fiscal 1998, exceeded expecta-

tions, becoming one of the Company’s most

successful brands in terms of introductory year

sales. Laundry and cleaning also performed well

on earnings, delivering half the region’s earnings

improvement behind the introduction of pre-

mium products, pricing and cost savings. In the

prior year, the sector was also a strong contributor,

driving volume and earnings gains.

The paper sector also provided solid volume

and earnings growth, achieving a 2% increase in

unit volume compared to a strong base year.

Tissue and towel posted gains on strength in the

base business, as did feminine protection, behind

the integration of the Tambrands acquisition,

and diapers, behind initiatives. The paper sector

improved sales and earnings ahead of volume, on

the strength of its pricing program and cost

savings, while still investing in initiatives. In 1998,

paper led the region in volume and earnings

progress. Prior year operating results were driven

by the feminine protection business, behind the

acquisition of Tambrands; initiative programs in

diapers; and tissue and towel capacity increases

and pricing strategies.

The health care sector posted a 3% increase

in unit volume versus the prior year. While all

categories delivered positive volume results, phar-

maceuticals made the strongest contribution by

increasing share on all major brands. The sector

attained excellent earnings progress behind the

shift toward higher-margin pharmaceutical sales

and pricing, mitigated by increased support for

upcoming initiative launches. In 1998, the sector’s

unit volume fell slightly, as improved volume in

pharmaceuticals only partially offset oral care

declines related to heavy competition. Prior year

earnings declined over 1997 due to a continued

investment in research and development, primarily

in pharmaceuticals, and in marketing support to

combat competition in oral care. The sector’s high

level of investment in research and development

has resulted in a strong pipeline of new phar-

maceutical products, while setting the stage for

innovations in other health care products in the

years to come.

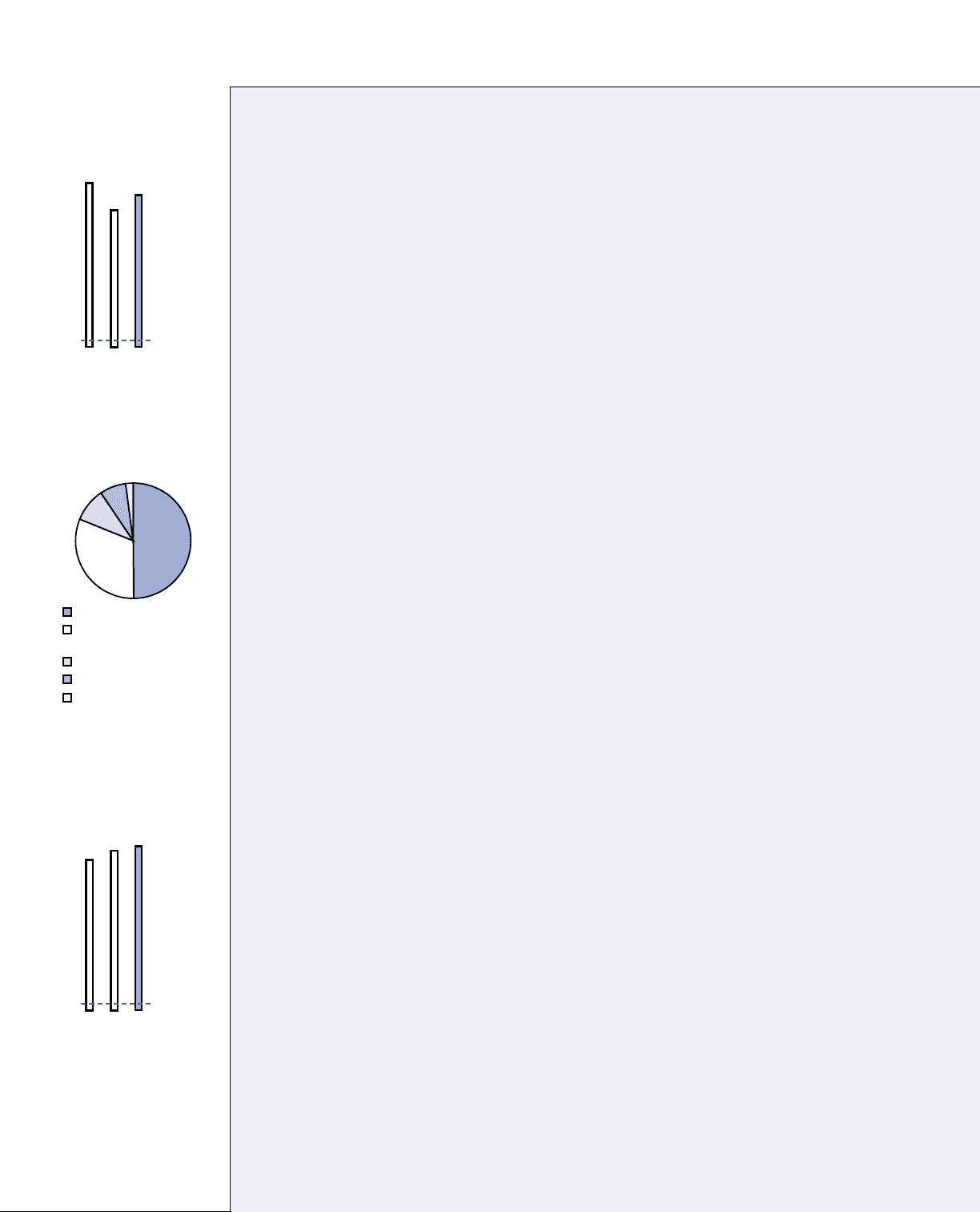

5.9

4.9

5.5

’97 ’98 ’99

OPERATING CASH FLOW

Billions of Dollars

North America 19.0

Europe, Middle East

and Africa 11.9

Asia 3.6

Latin America 2.8

Corporate & Other 0.8

1999 NET SALES BY

GEOGRAPHIC REGION

Billions of Dollars

17.6

18.5

19.0

’97 ’98 ’99

NORTH AMERICA

NET SALES

Billions of Dollars