LG 1999 Annual Report Download - page 30

Download and view the complete annual report

Please find page 30 of the 1999 LG annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

20 -

21

21 -

22

22 -

23

23 -

24

24 -

25

25 -

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

|

|

8

2

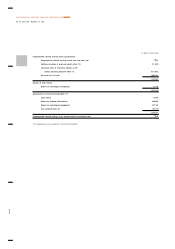

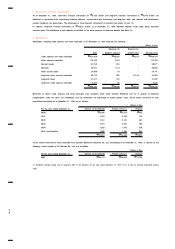

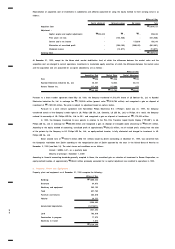

for the amortization of discounts or premiums (amortized cost). Declines in the fair value of debt securities which are anticipated to be

permanent are recorded in current operations. Subsequent recoveries are also recorded in current operations up to the amortized cost

of the investment.

Other investments in debt securities are carried at fair value. Temporary differences between fair value and amortized cost are

accounted for in the capital adjustment account. Declines in fair value which are anticipated to be permanent are recorded in current

operations after eliminating any previously recorded capital adjustment for temporary changes. Subsequent recoveries or other future

changes in fair value are recorded in the capital adjustment account.

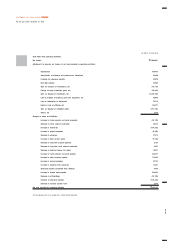

Allowance for Doubtful Accounts -

The Company provides an allowance for doubtful accounts and notes receivable based on the aggregate estimated collectibility of the accounts

and notes receivable.

Inventories -

Inventories are stated at the lower of cost or market, cost being determined using the weighted average method, except for materials in transit

which are determined using the specific identification method.

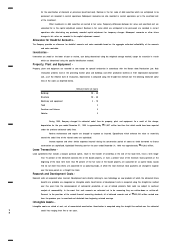

Property, Plant and Equipment -

Property, plant and equipment are recorded at cost except for upward revaluation in accordance with the Korean Asset Revaluation Law. Such

revaluation presents land at the prevailing market price and buildings and other production facilities at their depreciated replacement

cost, as of the effective date of revaluation. Depreciation is computed using the straight-line method over the following estimated useful

lives of the assets as described below.

Estimated Useful Life (years)

Buildings 20 - 40

Structures 20 - 40

Machinery and equipment 5 - 10

Tools 5

Furniture and fixtures 5

Vehicles 5

During 1999, Company changed its estimated useful lives for property, plant and equipment. As a result of this change,

depreciation for the year ended December 31, 1999 is approximately

₩

12,657 million less than that which would have been reported

under the previous estimated useful lives.

Routine maintenance and repairs are charged to expense as incurred. Expenditures which enhance the value or materially

extend the useful lives of the related assets are capitalized.

Interest expense and other similar expenses incurred during the construction period of assets on funds borrowed to finance

construction are capitalized. Capitalized financing cost for the year ended December 31, 1999 was approximately

₩

11,982 million.

Lease Transactions -

Lease agreements that include a bargain purchase option, result in the transfer of ownership at the end of the lease term, have a term longer

than 75 percent of the estimated economic life of the leased property, or have a present value of the minimum lease payments at the

beginning of the lease term more than 90 percent of the fair value of the leased property are accounted for as capital leases. Leases

that do not meet this criteria are accounted for as operating leases, of which the total minimum lease payments are charged to expense

over the lease period on a straight line basis.

Research and Development Costs -

Research costs are expensed when incurred. Development costs directly relating to new technology on new products of which the estimated future

benefits are probable are recognized as intangible assets. Amortization of development costs is computed using the straight-line method

over five years from the commencement of commercial production or use of related products. Such costs are subject to continual

analysis of recoverability. In the event that such amounts are estimated not to be recovering they are written-down or written-off.

Pursuant to the provision of the revised financial accounting standards, all of deferred research cost of

₩

425,582 million carried over

from the previous year is amortized and deducted from beginning retained earnings.

Intangible Assets -

Intangible assets are stated at cost, net of accumulated amortization. Amortization is computed using the straight-line method over the estimated

useful lives ranging from five to ten years.