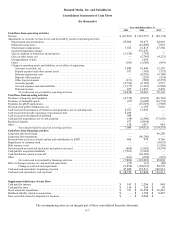

Enom 2015 Annual Report Download - page 77

Download and view the complete annual report

Please find page 77 of the 2015 Enom annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

86 -

87

87 -

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

|

|

F-13

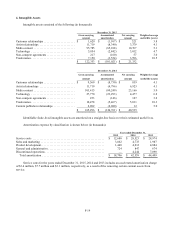

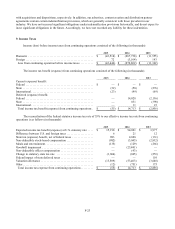

Intangible Assets — Media Content

We capitalize the direct costs incurred to acquire our media content that is determined to embody a probable future

economic benefit. Costs are recognized as finite-lived intangible assets based on their acquisition cost to us. All costs

incurred to deploy and publish content are expensed as incurred, including the costs incurred for the ongoing

maintenance of websites on which our content resides. We generally acquire content when our internal systems and

processes provide reasonable assurance that, given predicted consumer and advertiser demand relative to our

predetermined cost to acquire the content, the content unit will generate revenue over its useful life that exceeds the cost

of acquisition. In determining whether content embodies a probable future economic benefit required for asset

capitalization, we make judgments and estimates including the forecasted number of visits and the advertising rates that

the content will generate. These estimates and judgments take into consideration various inherent uncertainties including,

but not limited to, total expected visits over the content’s useful life; the fact that our content creation and distribution

model is evolving and may be impacted by competition and technological advancements; our ability to expand existing

and enter into new distribution channels and applications for our content; and whether we will be able to generate similar

economic returns from content in the future. Management has reviewed, and intends to regularly review, the operating

performance of content in determining probable future economic benefits of our content.

Capitalized media content is amortized on a straight-line basis over its useful life, which is typically five years,

representing our estimate of when the underlying economic benefits are expected to be realized and based on our

estimates of the projected cash flows from advertising revenue expected to be generated by the deployment of such

content. These estimates are based on our plans and projections, comparison of the economic returns generated by our

content with content of comparable quality and an analysis of historical cash flows generated by that content to date.

We continue to perform evaluations of our existing content library to identify potential improvements in our

content creation and distribution platform. As a result of these evaluations, we elected to remove certain content units

from our content library, resulting in $3.4 million, $7.7 million and $3.1 million of related accelerated amortization

expense in the years ended December 31, 2015, 2014 and 2013, respectively.

Intangibles Assets — Acquired in Business Combinations

We perform valuations of assets acquired and liabilities assumed on each acquisition accounted for as a business

combination and allocate the purchase price of each acquired business to our respective net tangible and intangible

assets. Acquired intangible assets include: trade names, non-compete agreements, owned website names, artist

relationships, customer relationships, technology, media content, and content publisher relationships. We determine the

appropriate useful life by performing an analysis of expected cash flows based on historical experience of the acquired

businesses. Intangible assets are amortized over their estimated useful lives using the straight-line method which

approximates the pattern in which the economic benefits are consumed.

Long-lived Assets

We evaluate the recoverability of our long-lived tangible and intangible assets with finite useful lives for

impairment when events or changes in circumstances indicate that the carrying amount of an asset group may not be

recoverable. Such trigger events or changes in circumstances may include: a significant decrease in the market price of a

long-lived asset, a significant adverse change in the extent or manner in which a long-lived asset is being used, a

significant adverse change in legal factors or in the business climate, including those resulting from technology

advancements in the industry, the impact of competition or other factors that could affect the value of a long-lived asset,

a significant adverse deterioration in the amount of revenue or cash flows we expect to generate from an asset group, an

accumulation of costs significantly in excess of the amount originally expected for the acquisition or development of a

long-lived asset, current or future operating or cash flow losses that demonstrate continuing losses associated with the

use of a long-lived asset, or a current expectation that, more likely than not, a long-lived asset will be sold or otherwise

disposed of significantly before the end of its previously estimated useful life. We perform impairment testing at the

asset group level that represents the lowest level for which identifiable cash flows are largely independent of the cash

flows of other assets and liabilities. If events or changes in circumstances indicate that the carrying amount of an asset

group may not be recoverable and the expected undiscounted future cash flows attributable to the asset group are less