CVS 2004 Annual Report Download - page 42

Download and view the complete annual report

Please find page 42 of the 2004 CVS annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52

|

|

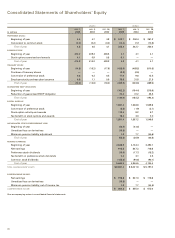

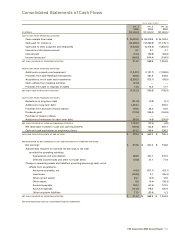

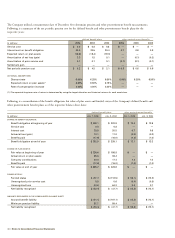

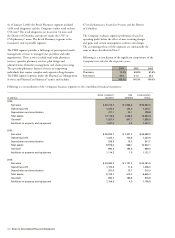

40 | Notes to Consolidated Financial Statements

The Company utilized a measurement date of December 31 to determine pension and other postretirement benefit measurements.

Following is a summary of the net periodic pension cost for the defined benefit and other postretirement benefit plans for the

respective years:

defined benefit plans other postretirement benefits

In millions 2004 2003 2002 2004 2003 2002

Service cost $ 0.9 $ 0.8 $ 0.8 $ — $ — $ —

Interest cost on benefit obligation 20.5 20.5 20.4 0.7 0.8 0.9

Expected return on plan assets (18.6) (18.4) (19.3) — — —

Amortization of net loss (gain) 3.3 1.5 0.1 — (0.1) (0.2)

Amortization of prior service cost 0.1 0.1 0.1 (0.1) (0.1) (0.1)

Settlement gain — — — — — —

Net periodic pension cost $ 6.2 $ 4.5 $ 2.1 $ 0.6 $ 0.6 $ 0.6

ACTUARIAL ASSUMPTIONS:

Discount rate 6.00% 6.25% 6.50% 6.00% 6.25% 6.50%

Expected return on plan assets(1) 8.50% 8.50% 8.75% — — —

Rate of compensation increase 4.00% 4.00% 4.00% — — —

(1) The expected long-term rate of return is determined by using the target allocation and historical returns for each asset class.

Following is a reconciliation of the benefit obligation, fair value of plan assets and funded status of the Company’s defined benefit and

other postretirement benefit plans as of the respective balance sheet dates:

defined benefit plans other postretirement benefits

In millions JAN.1, 2005 JAN.3, 2004 JAN.1, 2005 JAN.3, 2004

CHANGE IN BENEFIT OBLIGATION:

Benefit obligation at beginning of year $339.1 $322.8 $13.3 $ 13.8

Service cost 0.8 0.8 — —

Interest cost 20.5 20.5 0.7 0.8

Actuarial loss (gain) 10.1 11.0 (0.5) (0.3)

Benefits paid (17.6) (16.0) (1.4) (1.0)

Benefit obligation at end of year $352.9 $339.1 $12.1 $13.3

CHANGE IN PLAN ASSETS:

Fair value at beginning of year $ 226.6 $ 186.8 $ — $ —

Actual return on plan assets 25.8 38.4 — —

Company contributions 20.4 17.4 1.4 1.0

Benefits paid (17.6) (16.0) (1.4) (1.0)

Fair value at end of year $ 255.2 $ 226.6 $ — $ —

FUNDED STATUS:

Funded status $ (97.7) $ (112.5) $ (12.1) $ (13.3)

Unrecognized prior service cost 0.5 0.6 (0.4) (0.5)

Unrecognized loss 63.8 64.2 0.3 0.7

Net liability recognized $ (33.4) $ (47.7) $ (12.2) $ (13.1)

AMOUNTS RECOGNIZED IN THE CONSOLIDATED BALANCE SHEET:

Accrued benefit liability $ (91.1) $ (107.1) $ (12.2) $ (13.1)

Minimum pension liability 57.7 59.4 — —

Net liabilityrecognized $ (33.4) $ (47.7) $ (12.2) $ (13.1)