CVS 2004 Annual Report Download - page 40

Download and view the complete annual report

Please find page 40 of the 2004 CVS annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

-

52

|

|

straight-line basis over the term of the lease. In addition to

minimum rental payments, certain leases require additional

payments based on sales volume, as well as reimbursements for

real estate taxes, maintenance and insurance.

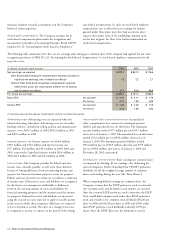

Following is a summary of the Company’s net rental expense

for operating leases for the respective years:

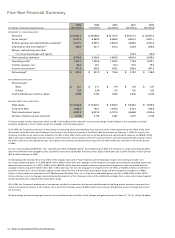

In millions 2004 2003 2002

Minimum rentals $ 1,020.6 $ 838.4 $ 790.4

Contingent rentals 61.7 62.0 65.6

1,082.3 900.4 856.0

Less: sublease income (14.0) (10.1) (9.3)

$ 1,068.3 $ 890.3 $ 846.7

Following is a summary of the future minimum lease payments

under capital and operating leases as of January 1, 2005:

CAPITAL OPERATING

In millions LEASES LEASES

2005 $ 0.2 $ 1,181.3

2006 0.2 1,120.8

2007 0.2 1,060.0

2008 0.2 1,008.1

2009 0.1 972.8

Thereafter 0.2 9,997.1

1.1 $ 15,340.1

Less: imputed interest (0.3)

Present value of capital lease obligations $ 0.8

The Company finances a portion of its store development

program through sale-leaseback transactions. The properties

are sold at net book value and the resulting leases qualify and

are accounted for as operating leases. The Company does not

have any retained or contingent interests in the stores nor does

the Company provide any guarantees, other than a corporate

level guarantee of lease payments, in connection with the

sale-leasebacks. Proceeds from sale-leaseback transactions

totaled $496.6 million in 2004, $487.8 million in 2003 and

$448.8 million in 2002. The operating leases that resulted

from these transactions are included in the above table.

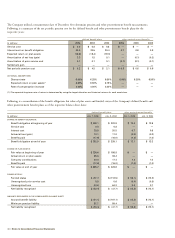

6 ²

²Employee stock ownership plan

The Company sponsors a defined contribution Employee Stock

Ownership Plan (the “ESOP”) that covers full-time employees

with at least one year of service.

In 1989, the ESOP Trust issued and sold $357.5 million of

20-year, 8.52% notes due December 31, 2008 (the “ESOP Notes”).

The proceeds from the ESOP Notes were used to purchase

6.7 million shares of Series One ESOP Convertible Preference

Stock (the “ESOP Preference Stock”) from the Company. Since

the ESOP Notes are guaranteed by the Company, the outstanding

balance is reflected as long-term debt and a corresponding

guaranteed ESOP obligation is reflected in shareholders’ equity

in the accompanying consolidated balance sheets.

Each share of ESOP Preference Stock has a guaranteed

minimum liquidation value of $53.45, is convertible into

2.314 shares of common stock and is entitled to receive an

annual dividend of $3.90 per share. The ESOP Trust uses the

dividends received and contributions from the Company to

repay the ESOP Notes. As the ESOP Notes are repaid, ESOP

Preference Stock is allocated to participants based on (i) the

ratio of each year’s debt service payment to total current and

future debt service payments multiplied by (ii) the number

of unallocated shares of ESOP Preference Stock in the plan.

As of January 1, 2005, 4.3 million shares of ESOP Preference

Stock were outstanding, of which 2.8 million shares were

allocated to participants and the remaining 1.5 million shares

were held in the ESOP Trust for future allocations.

Annual ESOP expense recognized is equal to (i) the interest

incurred on the ESOP Notes plus (ii) the higher of (a) the

principal repayments or (b) the cost of the shares allocated,

less (iii) the dividends paid. Similarly, the guaranteed ESOP

obligation is reduced by the higher of (i) the principal payments

or (ii) the cost of shares allocated.

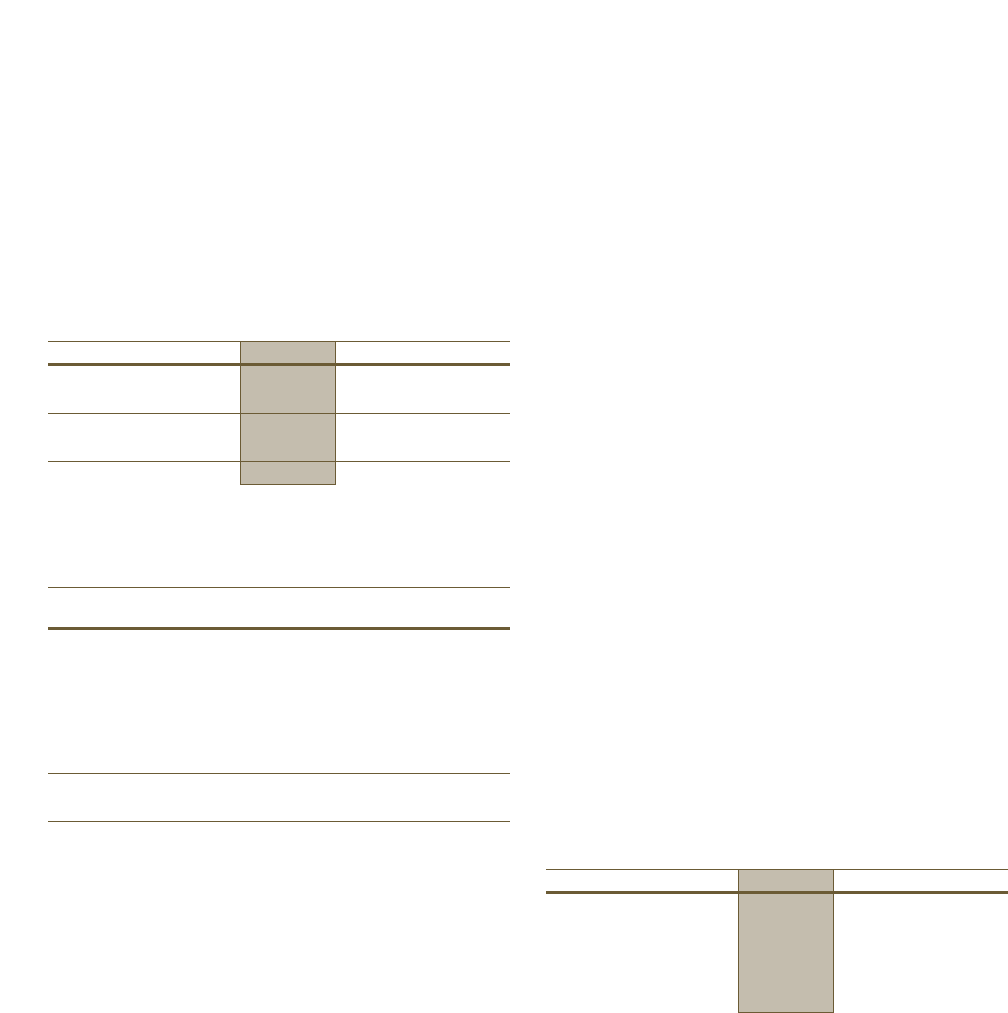

Following is a summary of the ESOP activity for the

respective years:

In millions 2004 2003 2002

ESOP expense recognized $ 19.5 $ 30.1 $ 26.0

Dividends paid 16.6 17.7 18.3

Cash contributions 19.5 30.1 26.0

Interest payments 13.9 16.6 18.7

ESOP shares allocated 0.3 0.4 0.4

7 ²

²Pension plans and other

postretirement benefits

Defined contribution plans

The Company sponsors a voluntary 401(k) Savings Plan that

covers substantially all employees who meet plan eligibility

requirements. The Company makes matching contributions

consistent with the provisions of the plan. At the participant’s

option, account balances, including the Company’s matching

contribution, can be moved without restriction among various

investment options, including the Company’s common stock.

The Company also maintains a nonqualified, unfunded

Deferred Compensation Plan for certain key employees. This

plan provides participants the opportunity to defer portions of

their compensation and receive matching contributions that they

would have otherwise received under the 401(k) Savings Plan

if not for certain restrictions and limitations under the Internal

38 | Notes to Consolidated Financial Statements