CVS 2004 Annual Report Download - page 39

Download and view the complete annual report

Please find page 39 of the 2004 CVS annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

-

51

-

52

|

|

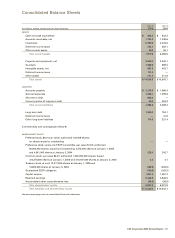

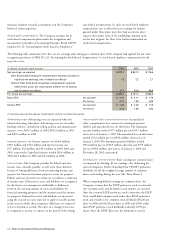

The amortization expense for these intangible assets totaled

$95.9 million in 2004, $63.2 million in 2003 and $53.3 million

in 2002. The anticipated annual amortization expense for

these intangible assets is $124.7 million in 2005, $118.8 million

in 2006, $113.3 million in 2007, $104.7 million in 2008 and

$96.2 million in 2009.

4 ²

²Borrowing and credit agreements

Following is a summary of the Company’s borrowings as of the

respective balance sheet dates:

JAN. 1, JAN. 3,

In millions 2005 2004

Commercial paper $ 885.6 $ —

5.5% senior notes due 2004 — 300.0

5.625% senior notes due 2006 300.0 300.0

3.875 % senior notes due 2007 300.0 300.0

4.0% senior notes due 2009 650.0 —

4.875% senior notes due 2014 550.0 —

8.52% ESOP notes due 2008(1) 140.9 163.2

Mortgage notes payable 14.8 12.2

Capital lease obligations 0.8 0.9

2,842.1 1,076.3

Less:

Short-term debt (885.6) —

Current portion of long-term debt (30.6) (323.2)

$ 1,925.9 $ 753.1

(1) See Note 6 for further information about the Company’s ESOP Plan.

In connection with our commercial paper program, the

Company maintains a $650 million, five-year unsecured

back-up credit facility, which expires on May 21, 2006, and

a $675 million, 364-day unsecured back-up credit facility,

which expires on June 10, 2005. In addition, the Company

maintains a $675 million, five-year unsecured backup credit

facility, which expires on June 11, 2009. The credit facilities allow

for borrowings at various rates depending on the Company’s

public debt ratings and require the Company to pay a quarterly

facility fee of 0.8%, regardless of usage. As of January 1, 2005,

the Company had no outstanding borrowings against the credit

facilities. The weighted average interest rate for short-term debt

was 1.8% as of January 1, 2005 and there were no outstanding

short-term borrowings as of January 3, 2004.

In September 2004, the Company issued $650 million

of 4.0% unsecured senior notes due September 15, 2009 and

$550 million of 4.875% unsecured senior notes due September

15, 2014 (collectively the “Notes”). The Notes pay interest

semi-annually and may be redeemed at any time, in whole

or in part at a defined redemption price plus accrued interest.

Net proceeds from the Notes were used to repay a portion

of the outstanding commercial paper issued to finance the

acquisition of the Acquired Businesses.

To manage a portion of the risk associated with potential

changes in market interest rates, the Company entered into

Treasury-Lock Contracts (the “Contracts”) with total notional

amounts of $600 million. The Company settled these Contracts

during the third quarter of 2004 in conjunction with the

placement of the long-term financing at a loss of $32.8 million.

The Company accounts for derivatives in accordance with

SFAS No. 133, “Accounting for Derivative Instruments and

Hedging Activities” as modified by SFAS No. 138, “Accounting

for Derivative Instruments and Certain Hedging Activities,”

which requires the resulting loss to be recorded in shareholders’

equity as a component of accumulated other comprehensive

loss. This unrealized loss will be amortized as a component of

interest expense, over the life of the related long-term financing.

As of January 1, 2005, the Company had no freestanding

derivatives in place.

The Credit Facilities and unsecured senior notes contain

customary restrictive financial and operating covenants. The

covenants do not materially affect the Company’s financial or

operating flexibility.

The aggregate maturities of long-term debt for each of the five

years subsequent to January 1, 2005 are $30.6 million in 2005,

$335.0 million in 2006, $341.7 million in 2007, $45.6 million in

2008 and $651.3 million in 2009.

5 ²

²Leases

The Company leases most of its retail locations and eight of

its distribution centers under non-cancelable operating leases,

whose initial terms typically range from 15 to 25 years, along

with options that permit renewals for additional periods. The

Company also leases certain equipment and other assets under

non-cancelable operating leases, whose initial terms typically

range from 3 to 10 years. The Company recently conformed its

accounting for operating leases and leasehold improvements to

the views expressed by the Office of the Chief Accountant of the

Securities and Exchange Commission to the American Institute

of Certified Public Accountants on February 7, 2005. As a result,

the Company recorded a $65.9 million non-cash pre-tax ($40.5

million after-tax) adjustment to total operating expenses, which

represents the cumulative effect of the adjustment for a period

of approximately 20 years (the “Lease Adjustment”). Since the

effect of the Lease Adjustment was not material to any previously

reported fiscal year, the cumulative effect was recorded in

the fourth quarter of 2004. Minimum rent is expensed on a

CVS Corporation 2004 Annual Report | 37