CVS 2004 Annual Report Download - page 23

Download and view the complete annual report

Please find page 23 of the 2004 CVS annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

13 -

14

14 -

15

15 -

16

16 -

17

17 -

18

18 -

19

19 -

20

20 -

21

21 -

22

22 -

23

23 -

24

24 -

25

25 -

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

|

|

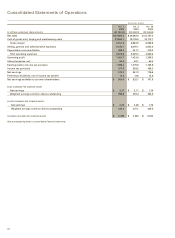

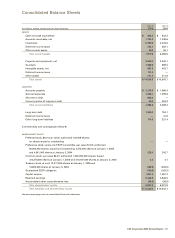

Following is a summary of our store development activity for the

respective years:

2004 2003 2002

Total stores

(beginning of year) 4,179 4,087 4,191

New and acquired stores 1,397 150 174

Closed stores (201) (58) (278)

Total stores (end of year) 5,375 4,179 4,087

Relocated stores(1) 96 125 92

(1) Relocated stores are not included in new or closed store totals.

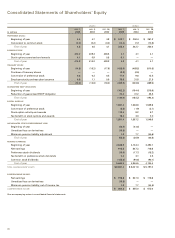

Net cash provided by financing activities increased to $1,798.2

million in 2004. This compares to net cash used in financing

activities of $72.5 million in 2003 and $4.9 million in 2002.

The increase in net cash provided by financing activities during

2004 was primarily due to the financing of the acquisition

of the Acquired Businesses, including the issuance of the Notes

(defined below), during the third quarter of 2004. The increase

was offset, in part, by the repayment of the $300 million 5.5%

unsecured senior notes, which matured during the first quarter

of 2004. Our net debt (i.e., our total debt less our cash and cash

equivalents), increased to $2,449.8 million, compared to $233.1

million in 2003 and $412.7 million in 2002. During 2004, we

paid common stock dividends totaling $105.6 million or $0.265

percommon share. In January 2005, our Board of Directors

authorized a 9% increase in our common stock dividend to

$0.290 per share for 2005.

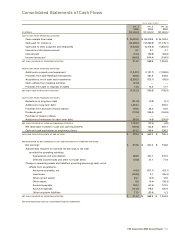

We believe that our current cash on hand, cash provided by

operations and sale-leaseback transactions, together with our

ability to obtain additional short-term and long-term financing,

will be sufficient to cover our working capital needs, capital

expenditures, debt service and dividend requirements for at

least the next several years.

We had $885.6 million of commercial paper outstanding at a

weighted average interest rate of 1.8% as of January 1, 2005. In

connection with our commercial paper program, we maintain a

$650 million, five-year unsecured back-up credit facility, which

expires on May 21, 2006, and a $675 million, 364-day unsecured

back-up credit facility, which expires on June 10, 2005. In

addition, we maintain a $675 million, five-year unsecured

backup credit facility, which expires on June 11, 2009. The credit

facilities allow for borrowings at various rates depending on our

public debt rating. As of January 1, 2005, we had no outstanding

borrowings against the credit facilities.

On September 14, 2004, we issued $650 million of 4.0%

unsecured senior notes due September 15, 2009 and $550

million of 4.875% unsecured senior notes due September 15,

2014 (collectively the “Notes”). The Notes pay interest

semi-annually and may be redeemed at any time, in whole or

inpart at a defined redemption price plus accrued interest. Net

proceeds from the Notes were used to repay a portion of the

outstanding commercial paper issued to finance the acquisition

ofthe Acquired Businesses. To manage a portion of the risk

associated with potential changes in market interest rates, during

the second quarter of 2004 we entered into Treasury-Lock

Contracts (the “Contracts”) with total notional amounts of $600

million. The Contracts settled in conjunction with the placement

of the long-term financing. As of January 1, 2005, we had no

freestanding derivatives in place.

Our credit facilities and unsecured senior notes contain customary

restrictive financial and operating covenants. These covenants

do not include a requirement for the acceleration of our debt

maturities in the event of a downgrade in our credit rating. We

do not believe that the restrictions contained in these covenants

materially affect our financial or operating flexibility.

Our liquidity is based, in part, on maintaining investment-grade

debt ratings. As of January 1, 2005, our long-term debt was

rated “A3” by Moody’s and “A-” by Standard & Poor’s, and our

commercial paper program was rated “P-2” by Moody’s and

“A-2” by Standard & Poor’s, each on a stable outlook. In assessing

our credit strength, we believe that both Moody’s and Standard

&Poor’s considered, among other things, our capital structure

and financial policies as well as our consolidated balance sheet,

the acquisition ofthe Acquired Businesses and other financial

information. Our debt ratings have a direct impact on our

future borrowing costs, access to capital markets and new

store operating lease costs.

OFF-BALANCE SHEET ARRANGEMENTS

Other than inconnection with executing operating leases,

we do not participate in transactions that generate relationships

with unconsolidated entities or financial partnerships, including

variable interest entities, nor do we have or guarantee any

off-balance sheet debt. We finance a portion of our new

store development through sale-leaseback transactions, which

involves selling stores to unrelated parties at net book value and

then leasing the stores back under leases that qualify and are

accounted for as operating leases. We do not have any retained

or contingent interests in the stores nor do we provide any

guarantees, other than a corporate level guarantee of the lease

payments, in connection with the sale-leasebacks. In accordance

with generally accepted accounting principles, our operating

leases are not reflected in our consolidated balance sheet.

Between 1991 and 1997, we sold or spun off a number of

subsidiaries, including Bob’s Stores, Linens ’n Things, Marshalls,

Kay-Bee Toys, Wilsons, This End Up and Footstar. In many

cases, when a former subsidiary leased a store, we provided a

corporate level guarantee of the store’s lease obligations. When

the subsidiaries were disposed of, the guarantees remained in

CVS Corporation 2004 Annual Report |21