Brother International 2008 Annual Report Download - page 25

Download and view the complete annual report

Please find page 25 of the 2008 Brother International annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

15 -

16

16 -

17

17 -

18

18 -

19

19 -

20

20 -

21

21 -

22

22 -

23

23 -

24

24 -

25

25 -

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

|

|

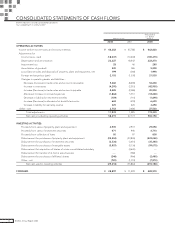

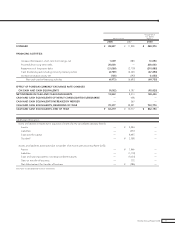

23Brother Annual Report 2008

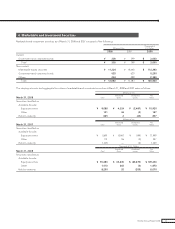

(19) Foreign Currency Financial Statements

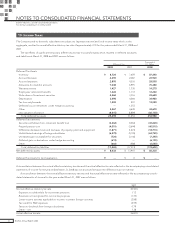

The balance sheet accounts of the consolidated foreign subsidiaries are translated into Japanese yen at the current

exchange rate as of the balance sheet date except for equity, which is translated at the historical rate.

Differences arising from such translation are shown as “Foreign currency translation adjustments” in a separate

component of the equity and included in minority interests.

Revenue and expense accounts of consolidated foreign subsidiaries are translated into Japanese yen at the average

exchange rate during the year.

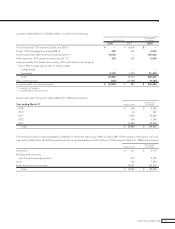

(20) Derivative and Hedging Activities

The Group uses derivative financial instruments to manage its exposures to fluctuations in foreign exchange and inter-

est rates. Foreign exchange forward contracts, interest rate swaps and currency option contracts are utilized by the

Group to reduce foreign currency exchange and interest rate risks. The Group does not enter into derivatives for trad-

ing or speculative purposes.

Derivative financial instruments and foreign currency transactions are classified and accounted for as follows:

a) all derivatives are recognized as either assets or liabilities and measured at fair value, and gains or losses on deriva-

tive transactions are recognized in the consolidated statements of income and

b) for derivatives used for hedging purposes, if derivatives qualify for hedge accounting because of high correlation and

effectiveness between the hedging instruments and the hedged items, gains or losses on derivatives are deferred

until maturity of the hedged transactions.

Foreign currency contracts and currency option contracts employed to hedge foreign exchange exposures are mea-

sured at fair value and unrealized gains (losses) are recognized in income.

Foreign currency forward contracts and currency option contracts used to hedge forecasted (or committed) transac-

tions are also measured at fair value but the unrealized gains (losses) are deferred until the underlying hedged transac-

tions are completed.

The interest rate swaps that qualify for hedge accounting and meet specific matching criteria are not remeasured at

market value but the differential paid or received under the swap agreements are recognized and included in interest

expense or income.

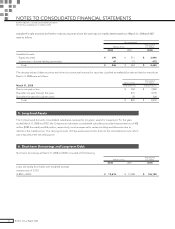

(21) Per Share Information

Basic net income per share is computed by dividing net income available to common shareholders by the weighted

average number of common shares outstanding for the period, retroactively adjusted for stock splits.

Diluted net income per share reflects the potential dilution that could occur if securities were exercised. Diluted net

income per share of common stock assumes full exercise of outstanding warrants at the beginning of the year (or at the

time of issuance).

Cash dividends per share presented in the accompanying consolidated statements of income are dividends applic-

able to the respective years including dividends to be paid after the end of the year.

(22) New Accounting Pronouncements

Lease Accounting

On March 30, 2007, the ASBJ issued ASBJ Statement No.13, “Accounting Standard for Lease Transactions”, which

revised the existing accounting standard for lease transactions issued on June 17, 1993. The revised accounting stan-

dard for lease transactions is effective for fiscal years beginning on or after April 1, 2008 with early adoption permitted

for fiscal years beginning on or after April 1, 2007.

Under the existing accounting standard, finance leases that deem to transfer ownership of the leased property to

the lessee are to be capitalized, however, other finance leases are permitted to be accounted for as operating lease

transactions if certain “as if capitalized” information is disclosed in the note to the lessee’s financial statements. The

revised accounting standard requires that all finance lease transactions should be capitalized.

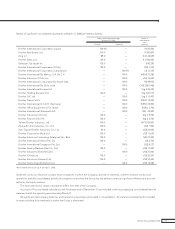

Unification of Accounting Policies Applied to Foreign Subsidiaries for the Consolidated Financial Statements

Under Japanese GAAP, a company currently can use the financial statements of foreign subsidiaries which are prepared