Brother International 2007 Annual Report Download - page 26

Download and view the complete annual report

Please find page 26 of the 2007 Brother International annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

16 -

17

17 -

18

18 -

19

19 -

20

20 -

21

21 -

22

22 -

23

23 -

24

24 -

25

25 -

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

|

|

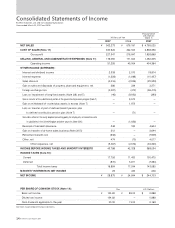

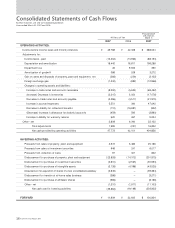

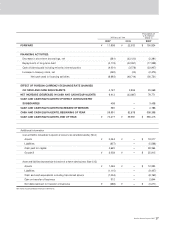

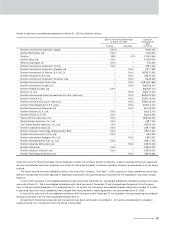

24 Brother Annual Report 2007

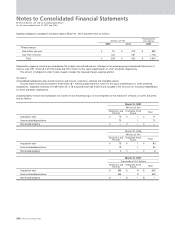

Notes to Consolidated Financial Statements

Brother Industries, Ltd. and Consolidated Subsidiaries

For the Years ended March 31, 2007 and 2006

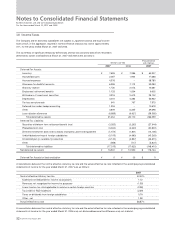

(24) New Accounting Pronouncements

Lease Accounting

On M arch 30, 2007, the ASBJ issued ASBJ Statement No.13, "Accounting Standard for Lease

Transactions", which revised the existing accounting standard for lease transactions issued on

June 17, 1993.

Under the existing accounting standard, finance leases that deem to transfer ow nership of

the leased property to the lessee are to be capitalized, how ever, other finance leases are permitted

to be accounted for as operating lease transactions if certain “ as if capitalized” information is

disclosed in the note to the lessee's financial statements.

The revised accounting standard requires that all finance lease transactions should be capitalized.

The revised accounting standard for lease transactions is effective for fiscal years beginning on or

after April 1, 2008 w ith early adoption permitted for fiscal years beginning on or after April 1, 2007.

Unification of Accounting Policies Applied to Foreign Subsidiaries for the Consolidated

Financial Statements

Under Japanese GAAP, a company currently can use the financial statements of foreign sub-

sidiaries which are prepared in accordance with generally accepted accounting principles in their

respective jurisdictions for its consolidation process unless they are clearly unreasonable. On

May 17, 2006, the ASBJ issued ASBJ Practical Issues Task Force (PITF) No.18, “ Practical Solution

on Unification of Accounting Policies Applied to Foreign Subsidiaries for the Consolidated Financial

Statements.” The new task force prescribes: 1) the accounting policies and procedures applied to

a parent company and its subsidiaries for similar transactions and events under similar circum-

stances should in principle be unified for the preparation of the consolidated financial statements,

2) financial statements prepared by foreign subsidiaries in accordance w ith either International

Financial Reporting Standards or the generally accepted accounting principles in the United States

tentatively may be used for the consolidation process, 3) how ever, the follow ing items should be

adjusted in the consolidation process so that net income is accounted for in accordance w ith

Japanese GAAP unless they are not material;

(1) Amortization of goodw ill

(2) Actuarial gains and losses of defined benefit plans recognized outside profit or loss

(3) Capitalization of intangible assets arising from development phases

(4) Fair value measurement of investment properties, and the revaluation model for

property, plant and equipment, and intangible assets

(5) Retrospective application when accounting policies are changed

(6) Accounting for net income attributable to a minority interest

The new task force is effective for fiscal years beginning on or after April 1, 2008 w ith early adoption

permitted.

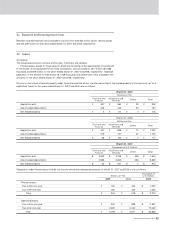

3. Business Combination

On July 1, 2006, the Group acquired 100% of shares of JAX Inc. (“ JAX” ). JAX engages in netw ork

karaoke business w hich was curved out from Taito Corporation. This acquisition was made to

expand market share by strengthening competitiveness through reinforcement of marketing and

product lines. The results of operations of JAX are included in the accompanying consolidated

financial statements of income from the date of the acquisition.

The Company accounted for this business combination by the purchase method of accounting.

The acquisition cost w as ¥ 4,645 million ($ 39,364 thousand) w hich was all paid in cash. The total

cost of acquisition has been allocated to the assets acquired and the liabilities assumed based on

their respective fair values. The fair values of assets acquired and liabilities assumed at the acqui-

sition date were disclosed as additional information in the accompanying consolidated statements

of cash flow s.