Brother International 2007 Annual Report Download - page 23

Download and view the complete annual report

Please find page 23 of the 2007 Brother International annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

13 -

14

14 -

15

15 -

16

16 -

17

17 -

18

18 -

19

19 -

20

20 -

21

21 -

22

22 -

23

23 -

24

24 -

25

25 -

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

|

|

21

Brother Annual Report 2007

of fixed assets as of April 1, 2005.

The Company and its domestic subsidiaries review its long-lived assets for impairment

whenever events or changes in circumstance indicate the carrying amount of an asset or asset

group may not be recoverable. An impairment loss w ould be recognized if the carrying amount of

an asset or asset group exceeds the sum of the undiscounted future cash flows expected to

result from the continued use and eventual disposition of the asset or asset group. The impairment

loss w ould be measured as the amount by which the carrying amount of the asset exceeds its

recoverable amount, which is the higher of the discounted cash flows from the continued use and

eventual disposition of the asset or the net selling price at disposition.

(9) Bond Issue Cost

Bond issue costs are charged to income as incurred.

(10) Research and Development Costs

Research and development costs are charged to income as incurred.

(11) Leases

Finance leases that do not transfer ow nership of the leased property to the lessee are primarily

accounted for as rental transactions. Under Japanese accounting standards for leases, finance

leases that are deemed to transfer ow nership of the leased property to the lessee are to be

capitalized, w hile other finance leases are permitted to be accounted for as operating lease trans-

actions if certain "as if capitalized" information is disclosed in the notes to the lessee's financial

statements.

(12) Warranty Reserve

The Group provided a warranty reserve for repair service to cover all repair expenses based on the

past w arranty experience regardless of w arranty period.

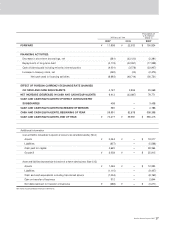

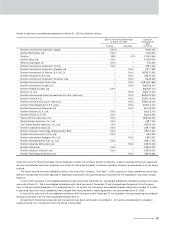

Warranty reserve included in accrued expense w as ¥ 7,603 million ($ 64,432 thousand) and

¥ 7,197 million at M arch 31, 2007 and 2006, respectively.

(13) Income Taxes

The provision for current income taxes is computed based on the pretax income included in the

consolidated statements of income. The asset and liability approach is used to recognize deferred

tax assets and liabilities for the expected future tax consequences of temporary differences

betw een the carrying amounts and the tax bases of assets and liabilities. Deferred taxes are

measured by applying currently enacted tax law s to the temporary differences.

(14) Liability for Retirement Benefits

(i) Em ployees' Retirem ent Benefits

-

The Company has a contributory funded pension plan

covering substantially all of its employees. Certain consolidated subsidiaries have non-contributory

funded pension plans or unfunded retirement benefit plans. Also, certain foreign subsidiaries

have defined benefit pension plans and defined contribution pension plans.

The Company and certain consolidated subsidiaries account for the liability for retirement

benefits based on projected benefit obligations and plan assets at the balance sheet date.

Certain small subsidiaries apply the simplified method to state the liability at the amount which

would be paid if employees retired less plan assets at the balance sheet date.

Effective April 1, 2005, consolidated subsidiaries in the United Kingdom and other countries

adopted a new accounting standard for employee benefits. The new local accounting standard

requires to evaluate pension obligation and plan assets at fair value, w hich resulted in a

transitional loss for the year w hen the new standard w as adopted. The effect of adoption of

the new accounting standard was to decrease in retirement benefit by ¥ 988 million and to

increase operating profit by the same amount for the year ended M arch 31, 2006. In addition,

these consolidated subsidiaries recognized a loss of ¥ 1,636 million for the full amount of

transitional obligation for employees' retirement benefits which w as included in the other

expenses in the accompanying consolidated statements of income.

(ii) Retirem ent Benefits for Directors and Corporate Auditors

-

Prior to June 23, 2006, the

Company provided retirement allowances for directors and corporate auditors. Retirement

allowances for directors and corporate auditors w ere recorded to state the liability w hich

would be paid if they retired at each balance sheet date. The retirement benefits for directors

and corporate auditors w ere paid upon the approval of the shareholders' meeting.