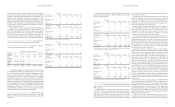

Abercrombie & Fitch 2006 Annual Report Download - page 16

Download and view the complete annual report

Please find page 16 of the 2006 Abercrombie & Fitch annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

6 -

7

7 -

8

8 -

9

9 -

10

10 -

11

11 -

12

12 -

13

13 -

14

14 -

15

15 -

16

16 -

17

17 -

18

18 -

19

19 -

20

20 -

21

21 -

22

22 -

23

23 -

24

24

|

|

Abercrombie &Fitch

31

appropriate, for changes in store quantities or replacement cost. This pol-

icy approximates the expense that would have been recognized under gen-

erally accepted accounting principles (“GAAP”). Store supply categories

are classified as current or non-current based on their estimated useful

lives. Packaging is expensed as used. Current store supplies were $20.0

million and $16.1 million at February 3, 2007 and January 28, 2006,

respectively. Non-current store supplies were $20.6 million at both

February 3, 2007 and January 28, 2006.

PROPERTY AND EQUIPMENT Depreciation and amortization

of property and equipment are computed for financial reporting pur-

poses on a straight-line basis, using service lives ranging principally

from 30 years for buildings, the lesser of ten years or the life of the lease

for leasehold improvements and three to ten years for other property

and equipment. The cost of assets sold or retired and the related accu-

mulated depreciation or amortization are removed from the accounts

with any resulting gain or loss included in net income. Maintenance

and repairs are charged to expense as incurred. Major renewals and

betterments that extend service lives are capitalized.

Long-lived assets are reviewed at the store level periodically for

impairment or whenever events or changes in circumstances indicate

that full recoverability of net assets through future cash flows is in

question. Factors used in the evaluation include, but are not limited to,

management’s plans for future operations, recent operating results and

projected cash flows. The Company incurred impairment charges of

approximately $0.3 million for both Fiscal 2006 and Fiscal 2005.

INCOME TAXES Income taxes are calculated in accordance with

SFAS No. 109, “Accounting for Income Taxes,” which requires the use of

the asset and liability method. Deferred tax assets and liabilities are rec-

ognized based on the difference between the financial statement carrying

amounts of existing assets and liabilities and their respective tax bases.

Deferred tax assets and liabilities are measured using current enacted tax

rates in effect in the years in which those temporary differences are

expected to reverse. Inherent in the measurement of deferred balances are

certain judgments and interpretations of enacted tax law and published

guidance with respect to applicability to the Company’s operations. A

valuation allowance has been provided for losses related to the start-up

costs associated with operations in foreign countries. No other valuation

allowances have been provided for deferred tax assets because manage-

ment believes that it is more likely than not that the full amount of the

net deferred tax assets will be realized in the future. The effective tax rate

utilized by the Company reflects management’s judgment of the expected

tax liabilities within the various taxing jurisdictions.

FOREIGN CURRENCY TRANSLATION Some of the Company’s

international operations use local currencies as the functional currency.

In accordance with SFAS No. 52, “Foreign Currency Translation”, assets

and liabilities denominated in foreign currencies were translated into U.S.

dollars (the reporting currency) at the exchange rate prevailing at the

balance sheet date. Revenues and expenses denominated in foreign cur-

rencies were translated into U.S. dollars at the monthly average exchange

rate for the period. Gains and losses resulting from foreign currency trans-

$4.6 million and $5.0 million, respectively, of the marketable securities

were invested in dividend received deduction.

The Company established an irrevocable rabbi trust during the third

quarter of Fiscal 2006, the purpose is to be a source of funds to match

respective funding obligations to participants in the Abercrombie &

Fitch Nonqualified Savings and Supplemental Retirement Plan and

the Chief Executive Officer Supplemental Executive Retirement Plan.

As of February 3, 2007, total assets related to the Rabbi Trust were

$33.5 million, which included $18.3 million of available-for-sale

securities and $15.3 million related to the cash surrender value of trust

owned life insurance policies. The Rabbi Trust assets are consolidated

in accordance with Emerging Issues Task Force 97-14 (“EITF 97-14”)

and recorded at fair value in other assets on the Consolidated Balance

Sheet and were restricted as to their use as noted above.

CREDIT CARD RECEIVABLES As part of the normal course of

business, the Company has approximately two to three days of sales

transactions outstanding with its third-party credit card vendors at any

point. The Company classifies these outstanding balances as receivables.

INVENTORIES Inventories are principally valued at the lower of

average cost or market utilizing the retail method. The Company

determines market value as the anticipated future selling price of the

merchandise less a normal margin. Therefore, an initial markup is

applied to inventory at cost in order to establish a cost-to-retail ratio.

Permanent markdowns, when taken, reduce both the retail and cost

components of inventory on hand so as to maintain the already

established cost-to-retail relationship.

The fiscal year is comprised of two principal selling seasons: Spring

(the first and second quarters) and Fall (the third and fourth quarters).

The Company classifies its inventory into three categories: spring fash-

ion, fall fashion and basic. The Company reduces inventory valuation

at the end of the first and third quarters to reserve for projected inven-

tory markdowns required to sell through the current season inventory

prior to the beginning of the following season. Additionally, the

Company reduces inventory at season end by recording a markdown

reserve that represents the estimated future anticipated selling price

decreases necessary to sell through the remaining carryover fashion

inventory for the season just passed. Further, as part of inventory val-

uation, inventory shrinkage estimates, based on historical trends from

actual physical inventories, are made that reduce the inventory value

for lost or stolen items. The Company performs physical inventories

throughout the year and adjusts the shrink reserve accordingly.

The markdown reserve was $6.8 million, $10.0 million and $6.6

million at February 3, 2007, January 28, 2006 and January 29, 2005, respec-

tively. The shrink reserve was $7.7 million, $3.8 million and $2.9 million

at February 3, 2007, January 28, 2006 and January 29, 2005, respectively.

STORE SUPPLIES The initial inventory of supplies for new stores

including, but not limited to, hangers, signage, security tags and point-of-

sale supplies are capitalized at the store opening date. In lieu of amortiz-

ing the initial balances over their estimated useful lives, the Company

expenses all subsequent replacements and adjusts the initial balance, as

Abercrombie &Fitch

30

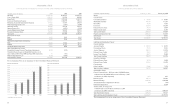

1. BASIS OF PRESENTATION Abercrombie & Fitch Co. (“A&F”),

through its wholly-owned subsidiaries (collectively, A&F and its whol-

ly-owned subsidiaries are referred to as “Abercrombie & Fitch” or the

“Company”), is a specialty retailer of high-quality, casual apparel for

men, women and kids with an active, youthful lifestyle. The business

was established in 1892.

The accompanying consolidated financial statements include the

historical financial statements of, and transactions applicable to, A&F

and its wholly-owned subsidiaries and reflect the assets, liabilities,

results of operations and cash flows on a historical cost basis.

The Company’s fiscal year ends on the Saturday closest to January 31,

typically resulting in a fifty-two week year, but occasionally giving rise to

an additional week, resulting in a fifty-three week year. Fiscal years are

designated in the financial statements and notes by the calendar year in

which the fiscal year commences. All references herein to “Fiscal 2006”

represent the results of the 53-week fiscal year ended February 3, 2007;

to “Fiscal 2005” represent the 52-week fiscal year ended January 28, 2006;

and to “Fiscal 2004” represent the 52-week fiscal year ended January 29,

2005. In addition, all references herein to “Fiscal 2007” represent the 52-

week fiscal year that will end on February 2, 2008.

RECLASSIFICATIONS Certain amounts have been reclassified to

conform with the current year presentation. The Company periodical-

ly acquires shares of its Class A Common Stock, par value $0.01 per

share (“Common Stock”) under various Board of Directors authorized

share buy-back plans. The shares acquired are held as treasury stock

and are not retired. The Company utilizes the treasury stock when

issuing shares for stock option exercises and restricted stock unit vest-

ings. In accordance with the Accounting Principles Board (“APB”)

Opinion No. 6, “Status of Accounting Research Bulletins,” “gains” on

sales of treasury stock not previously accounted for as constructively

retired should be credited to paid-in capital; “losses” may be charged to

paid-in capital to the extent of previous net “gains” from sales or retire-

ments of the same class of stock, otherwise to retained earnings. On the

Consolidated Balance Sheet for the year ended January 28, 2006, the

Company reclassified cumulative treasury stock “losses” of $67.6 mil-

lion to retained earnings that were previously netted against paid-in

capital. On the Consolidated Statements of Shareholders’ Equity for

the year ended January 31, 2004, the Company reclassified cumulative

treasury stock “losses” of $20.1 million to retained earnings that were

previously netted against paid-in capital. In addition, on the

Consolidated Statements of Shareholders’ Equity for the years ended

January 29, 2005 and January 28, 2006, the Company reclassified treas-

ury stock “losses” of $16.2 million and $31.3 million, respectively, to

retained earnings that were previously netted against paid-in capital.

Amounts reclassified did not have an effect on the Company’s results

of operations or Consolidated Statements of Cash Flows.

SEGMENT REPORTING In accordance with Statement of

Financial Accounting Standards (“SFAS”) No. 131, “Disclosures

about Segments of an Enterprise and Related Information,” the

Company determined its operating segments on the same basis that

it uses to evaluate performance internally. The operating segments

identified by the Company, Abercrombie & Fitch, abercrombie,

Hollister and RUEHL, have been aggregated and are reported as one

reportable financial segment. The Company aggregates its operating

segments because they meet the aggregation criteria set forth in para-

graph 17 of SFAS No. 131. The Company believes its operating segments

may be aggregated for financial reporting purposes because they are

similar in each of the following areas: class of consumer, economic

characteristics, nature of products, nature of production processes

and distribution methods. Revenues relating to the Company’s inter-

national sales in Fiscal 2006 were not material and are not reported

separately from domestic revenues.

2. SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES

PRINCIPLES OF CONSOLIDATION

The consolidated financial

statements include the accounts of A&F and its subsidiaries. All intercom-

pany balances and transactions have been eliminated in consolidation.

CASH AND EQUIVALENTS Cash and equivalents include amounts

on deposit with financial institutions and investments with original

maturities of less than 90 days. Outstanding checks at year-end are

reclassified in the balance sheet from cash to be reflected as liabilities.

INVESTMENTS Investments with original maturities greater than 90

days are accounted for in accordance with SFAS No. 115, “Accounting for

Certain Investments in Debt and Equity Securities,” and are classified

accordingly by the Company at the time of purchase. At February 3,

2007, the Company’s investments in marketable securities consisted pri-

marily of investment grade municipal notes and bonds and investment

grade auction rate securities, all classified as available-for-sale and report-

ed at fair value based on the market, with maturities that could range

from one month to 40 years.

The Company began investing in municipal notes and bonds

during Fiscal 2005. These investments have early redemption provisions

at predetermined prices. For the fiscal years ended February 3, 2007 and

January 28, 2006, there were no realized gains or losses. Net unrealized

holding losses were approximately $0.7 million for both the fiscal years

ended February 3, 2007 and January 28, 2006.

For the Company’s investments in auction rate securities, the inter-

est rates reset through an auction process at predetermined periods

ranging from seven to 49 days. Due to the frequent nature of the reset

feature, the investment’s market price approximates its fair value; there-

fore, there are no realized or unrealized gains or losses associated with

these marketable securities.

The Company held approximately $447.8 million and $411.2 mil-

lion in marketable securities as of February 3, 2007 and January 28,

2006, respectively.

As of February 3, 2007 and January 28, 2006, approximately $346.1

million and $285.4 million, respectively, of marketable securities were

invested in auction rate securities. As of February 3, 2007 and January

28, 2006, approximately $97.1 million and $120.8 million, respec-

tively, of marketable securities were invested in municipal notes and

bonds. As of February 3, 2007 and January 28, 2006, approximately

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS