Abercrombie & Fitch 2006 Annual Report Download - page 12

Download and view the complete annual report

Please find page 12 of the 2006 Abercrombie & Fitch annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

2 -

3

3 -

4

4 -

5

5 -

6

6 -

7

7 -

8

8 -

9

9 -

10

10 -

11

11 -

12

12 -

13

13 -

14

14 -

15

15 -

16

16 -

17

17 -

18

18 -

19

19 -

20

20 -

21

21 -

22

22 -

23

-

24

|

|

the outcome of various issues. Management may also use outside

legal advice to assist in the estimating process. However, the ultimate

outcome of various legal issues could be different than management

estimates, and adjustments may be required. The Company accrues

for its legal obligations for outstanding bills, expected defense costs and,

if appropriate, settlements. Accruals are made for personnel, general

litigation and intellectual property cases.

EQUITY COMPENSATION EXPENSE Prior to January 29,

2006, the Company reported share-based compensation through the

disclosure-only requirements of SFAS No. 123, “Accounting for Stock-

Based Compensation,” as amended by SFAS No. 148, “Accounting for

Stock-Based Compensation–Transition and Disclosure–an Amendment

of FASB No. 123,” but elected to measure compensation expense using

the intrinsic value method in accordance with APB Opinion No. 25,

“Accounting for Stock Issued to Employees,” for which no expense was

recognized for stock options if the exercise price was equal to the market

value of the underlying Common Stock on the date of grant, and

provided the required pro forma disclosures in accordance with SFAS

No. 123, “Accounting for Stock-Based Compensation”(“SFAS No. 123”),

as amended.

Effective January 29, 2006, the Company adopted the provisions of

SFAS No.123(R) which requires stock options to be accounted for

under the fair value method and requires the use of an option-pricing

model for estimating fair value. Accordingly, share-based compensa-

tion is measured at the grant date, based on the fair value of the award.

The Company’s equity compensation expense related to stock

options is estimated using the Black-Scholes option-pricing model to

determine the fair value of the stock option grants, which requires the

Company to estimate the expected term of the stock option grants and

expected future stock price volatility over the term. The term repre-

sents the expected period of time the Company believes the options will

be outstanding based on historical information. Estimates of expected

future stock price volatility are based on the historic volatility of the

Company’s stock for the period equal to the expected term of the stock

option. The Company calculates the historic volatility as the annu-

alized standard deviation of the differences in the natural logarithms

of the weekly stock closing price, adjusted for stock splits.

The fair value calculation under the Black-Scholes valuation

model is particularly sensitive to changes in the term and volatility

assumptions. Increases in term or volatility will result in a higher fair

valuation of stock option grants. Assuming all other assumptions dis-

closed in Note 4 of the Notes to the Consolidated Financial

Statements, “Share Based Compensation,” being equal, a 10% increase

in term will yield a 5% increase in the Black-Scholes valuation, while

a 10% increase in volatility will yield a 7% increase in the Black-

Scholes valuation. The Company believes that changes in term and

volatility would not have a material effect on the Company’s results

since the number of stock options granted during the periods pre-

sented was not material.

RECENTLY ISSUED ACCOUNTING PRONOUNCEMENTS

In July 2006, the FASB released Interpretation No. 48, “Accounting for

capitalized. Long-lived assets are reviewed at the store level period-

ically for impairment or whenever events or changes in circumstances

indicate that full recoverability of net assets through future cash flows

is in question. Factors used in the evaluation include, but are not lim-

ited to, management’s plans for future operations, recent operating

results and projected cash flow.

INCOME TAXES Income taxes are calculated in accordance with

SFAS No. 109, “Accounting for Income Taxes,” which requires the use

of the asset and liability method. Deferred tax assets and liabilities are

recognized based on the difference between the financial statement car-

rying amounts of existing assets and liabilities and their respective

tax bases. Deferred tax assets and liabilities are measured using cur-

rent enacted tax rates in effect for the years in which those temporary

differences are expected to reverse. Inherent in the measurement of

deferred balances are certain judgments and interpretations of enacted

tax law and published guidance with respect to applicability to the

Company’s operations. A valuation allowance has been provided for

losses related to the start-up costs associated with operations in foreign

countries. No other valuation allowances have been provided for

deferred tax assets because management believes that it is more likely

than not that the full amount of the net deferred tax assets will be real-

ized in the future. The effective tax rate utilized by the Company

reflects management’s judgment of the expected tax liabilities within

the various taxing jurisdictions.

The provision for income taxes is based on the current estimate of

the annual effective tax rate adjusted to reflect the tax impact of items

discrete to the quarter. The Company records tax expense or benefit

that does not relate to ordinary income in the current fiscal year dis-

cretely in the period in which it occurs pursuant to the requirements

of APB Opinion No. 28, “Interim Financial Reporting” and Financial

Accounting Standards Board issued Interpretation (“FIN”) 18,

“Accounting for Income Taxes in Interim Periods – an Interpretation of APB

Opinion No. 28.” Examples of such types of discrete items include, but

are not limited to, changes in estimates of the outcome of tax matters

related to prior years, provision-to-return adjustments, tax-exempt

income and the settlement of tax audits.

FOREIGN CURRENCY TRANSLATION Some of the Company’s

international operations use local currencies as the functional currency.

In accordance with SFAS No. 52, “Foreign Currency Translation”, assets and

liabilities denominated in foreign currencies were translated into U.S. dol-

lars (the reporting currency) at the exchange rate prevailing at the balance

sheet date. Revenues and expenses denominated in foreign currencies were

translated into U.S. dollars at the monthly average exchange rate for the

period. Gains and losses resulting from foreign currency transactions are

included in the results of operations, whereas related translation adjust-

ments are reported as an element of other comprehensive income in

accordance with SFAS No. 130, “Reporting Comprehensive Income.”

CONTINGENCIES In the normal course of business, the Company

must make continuing estimates of potential future legal obligations

and liabilities, which requires the use of management’s judgment on

Abercrombie &Fitch

23

Abercrombie &Fitch

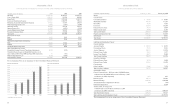

$130 to approximately $147. The Company expects the average

construction cost per square foot, net of construction allowances,

for new abercrombie stores to decrease from last year’s actual cost of

approximately $169 to approximately $164. The change from last

year’s estimates for Hollister and abercrombie were driven by a number

of factors, including store location, construction material pricing,

landlord allowance levels, and furniture and fixture additions. During

Fiscal 2007, the Company expects average construction cost per square

foot, net of construction allowances, for new non-flagship Abercrombie

& Fitch stores to be approximately $115 and for new RUEHL stores

to be approximately $274 per square foot, net of construction

allowances. The Company believes that the construction costs for

Abercrombie & Fitch and RUEHL stores in Fiscal 2006 were not

representative of the costs the Company expects to incur in Fiscal 2007

and therefore comparisons with these numbers would not be mean-

ingful. The Company expects initial inventory purchases for the stores

to average approximately $0.4 million, $0.2 million, $0.3 million and

$0.5 million per store for Abercrombie & Fitch, abercrombie, Hollister

and RUEHL, respectively.

The Company expects that substantially all future capital expendi-

tures will be funded with cash from operations. In addition, the Company

has $250 million available (less outstanding letters of credit) under its

Amended Credit Agreement to support operations.

CRITICAL ACCOUNTING POLICIES AND ESTIMATES

The Company’s discussion and analysis of its financial condition and

results of operations are based upon the Company’s consolidated

financial statements, which have been prepared in accordance with

accounting principles generally accepted in the United States

(“GAAP”). The preparation of these financial statements requires

the Company to make estimates and assumptions that affect the

reported amounts of assets, liabilities, revenues and expenses. Since

actual results may differ from those estimates, the Company revises its

estimates and assumptions as new information becomes available.

The Company’s significant accounting policies can be found in the

Notes to Consolidated Financial Statements (see Note 2 of the Notes

to Consolidated Financial Statements). The Company believes that the

following policies are most critical to the portrayal of the Company’s

financial condition and results of operations.

REVENUE RECOGNITION The Company recognizes retail sales

at the time the customer takes possession of the merchandise and

purchases are paid for, primarily with either cash or credit card.

Direct-to-consumer sales are recorded upon customer receipt of

merchandise. Amounts relating to shipping and handling billed to

customers in a sale transaction are classified as revenue and the related

direct shipping and handling costs are classified as stores and distri-

bution expense. Associate discounts are classified as a reduction of

revenue. The Company reserves for sales returns through estimates

based on historical experience and various other assumptions that

management believes to be reasonable. The Company’s gift cards do

not expire or lose value over periods of inactivity. The Company

accounts for gift cards by recognizing a liability at the time a gift card

is sold. The liability remains on the Company’s books until the ear-

lier of redemption (recognized as revenue) or when the Company

determines the likelihood of redemption is remote (recognized as

other operating income). The Company determines the probability of

the gift card being redeemed to be remote based on historical redemp-

tion patterns and at these times recognizes the remaining balance as

other operating income. At February 3, 2007 and January 28, 2006, the

gift card liability on the Company’s Consolidated Balance Sheet was

$65.0 million and $53.2 million, respectively.

The Company is not required by law to escheat the value of unre-

deemed gift cards to the states in which it operates. During Fiscal 2006,

Fiscal 2005 and Fiscal 2004, the Company recognized other operating

income for adjustments to the gift card liability of $5.2 million, $2.4 mil-

lion and $4.3 million, respectively.

INVENTORY VALUATION Inventories are principally valued at

the lower of average cost or market utilizing the retail method. The

Company determines market value as the anticipated future selling

price of the merchandise less a normal margin. An initial markup is

applied to inventory at cost in order to establish a cost-to-retail ratio.

Permanent markdowns, when taken, reduce both the retail and cost

components of inventory on hand so as to maintain the already estab-

lished cost-to-retail relationship. At first and third fiscal quarter end,

the Company reduces inventory value by recording a markdown

reserve that represents the estimated future anticipated selling price

decreases necessary to sell-through the current season inventory. At

second and fourth fiscal quarter end, the Company reduces inventory

value by recording a markdown reserve that represents the estimated

future selling price decreases necessary to sell-through any remaining

carryover inventory from the season just passed.

Additionally, as part of inventory valuation, an inventory shrink

estimate is made each period that reduces the value of inventory for lost

or stolen items. The Company performs physical inventories through-

out the year and adjusts the shrink reserve accordingly.

Inherent in the retail method calculation are certain significant

judgments and estimates including, among others, markdowns and

shrinkage, which could significantly impact the ending inventory

valuation at cost as well as the resulting gross margins. An increase or

decrease in the inventory shrink estimate of 10% would not have a

material impact on the Company’s results of operations. Management

believes this inventory valuation method is appropriate since it pre-

serves the cost-to-retail relationship in ending inventory.

PROPERTY AND EQUIPMENT Depreciation and amortiza-

tion of property and equipment are computed for financial reporting

purposes on a straight-line basis, using service lives ranging principally

from 30 years for buildings, the lesser of ten years or the life of the lease

for leasehold improvements and three to ten years for other property

and equipment. The cost of assets sold or retired and the related

accumulated depreciation or amortization are removed from the

accounts with any resulting gain or loss included in net income.

Maintenance and repairs are charged to expense as incurred. Major

remodels and improvements that extend service lives of the assets are

22