Seagate 2002 Annual Report Download - page 61

Download and view the complete annual report

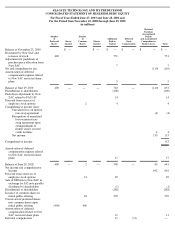

Please find page 61 of the 2002 Seagate annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

|

|

Risks Related to Our Common Shares

Control by Our Sponsor Group—Because our sponsor group, through its ownership of New SAC, will continue to hold a controlling

interest in us, the influence of our public shareholders over significant corporate actions will be limited.

After the secondary public offering of our common shares by New SAC in July 2003, affiliates of Silver Lake Partners, Texas Pacific

Group, August Capital, J.P. Morgan Partners, LLC and investment partnerships affiliated with Goldman, Sachs & Co. indirectly own

approximately 20.0%, 14.2%, 7.3%, 4.2% and 1.4%, respectively, of our outstanding common shares through their ownership of New SAC.

The sponsors’ ownership of New SAC and New SAC’s and the sponsors’ ownership of us is the subject of shareholders agreements and other

arrangements that result in the sponsors’

acting as a group with respect to all matters submitted to our shareholders. As a result, the members of

our sponsor group will continue to have the power to:

•

control all matters submitted to our shareholders;

•

elect our directors; and

Also, New SAC is not prohibited from selling a controlling interest in us to a third party.

Accordingly, our ability to engage in significant transactions, such as a merger, acquisition or liquidation, is limited without the consent

of members of our sponsor group. Conflicts of interest could arise between us and our sponsor group, and any conflict of interest may be

resolved in a manner that does not favor us. The members of our sponsor group may continue to retain control of us for the foreseeable future

and may decide not to enter into a transaction in which you would receive consideration for your common shares that is much higher than the

cost to you or the then-current market price of those shares. In addition, the members of our sponsor group could elect to sell a controlling

interest in us and you may receive less than the then-current fair market value or the price you paid for your shares. Any decision regarding

their ownership of us that members of our sponsor group may make at some future time will be in their absolute discretion.

Future Sales—Additional sales of our common shares by New SAC, our sponsors or our employees or issuances by us in connection

with future acquisitions or otherwise could cause the price of our common shares to decline.

•

exercise control over our business, policies and affairs.

If New SAC or – after any distribution to our sponsors of our shares by New SAC – our sponsors sell a substantial number of our

common shares in the future, the market price of our common shares could decline. The perception among investors that these sales may occur

could produce the same effect. New SAC and our sponsors have rights, subject to specified conditions, to require us to file registration

statements covering common shares or to include common shares in registration statements that we may file. By exercising their registration

rights and selling a large number of common shares, New SAC or any of the sponsors could cause the price of our common shares to decline.

Furthermore, if we were to include common shares in a registration statement initiated by us, those additional shares could impair our ability to

raise needed capital by depressing the price at which we could sell our common shares.

One component of our business strategy is to make acquisitions. In the event of any future acquisitions, we could issue additional

common shares, which would have the effect of diluting your percentage ownership of the common shares and could cause the price of our

common shares to decline.

56