Reebok 2011 Annual Report Download - page 188

Download and view the complete annual report

Please find page 188 of the 2011 Reebok annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

178 -

179

179 -

180

180 -

181

181 -

182

182 -

183

183 -

184

184 -

185

185 -

186

186 -

187

187 -

188

188 -

189

189 -

190

190 -

191

191 -

192

192 -

193

193 -

194

194 -

195

195 -

196

196 -

197

197 -

198

198 -

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

|

|

adidas Group

2011 Annual Report

CONSOLIDATED FINANCIAL STATEMENTS

04.8 Notes

184

2011

184

2011

04.8

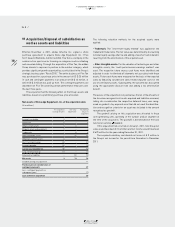

Inventories

Merchandise and finished goods are valued at the lower of cost or

net realisable value, which is the estimated selling price in the ordi-

nary course of business less the estimated costs of completion and

the estimated costs necessary to make the sale. Costs are determined

using a standard valuation method: the “average cost method”. Costs

of finished goods include cost of raw materials, direct labour and the

components of the manufacturing overheads which can reasonably

be attributed. The allocation of overheads is based on the planned

average utilisation. The net realisable value allowances are computed

consistently throughout the Group based on the age and expected

future sales of the items on hand.

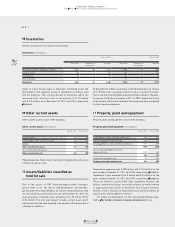

Assets/liabilities classified as held for sale

Primarily non-current assets and liabilities expected to be recov-

ered principally through sale rather than through continuing use are

classified as held for sale. These are measured at the lower of their

carrying amount and fair value less costs to sell. A potential gain or

loss is offset against the carrying amount of the assets and liabilities

classified as held for sale. Assets classified as held for sale are not

depreciated.

Property, plant and equipment

Property, plant and equipment are measured at amortised cost. This

comprises any costs directly attributable to bringing the asset to the

condition necessary for it to be capable of operating in the manner

intended by Management less accumulated depreciation (except for

land and construction in progress) and accumulated impairment

losses. Depreciation is recognised over the estimated useful life

utilising the “straight-line method” and taking into account any poten-

tial residual value, except where the “declining-balance method” is

more appropriate in light of the actual utilisation pattern. Parts of an

item of property, plant and equipment with a cost that is significant in

relation to the total cost of the item are depreciated separately.

Estimated useful lives are as follows:

Estimated useful lives of property, plant and equipment

Years

Buildings and leasehold improvements 5 – 50

Technical equipment and machinery as well as other equipment

and furniture and fixtures 2 – 10

Expenditures for repairs and maintenance are expensed as incurred.

Renewals and improvements are capitalised and depreciated separ-

ately, if the recognition criteria are met.

Impairment losses

If facts and circumstances indicate that non-current assets (e.g. prop-

erty, plant and equipment, intangible assets including goodwill and

certain financial assets) might be impaired, the recoverable amount

is determined. It is measured at the higher of its fair value less costs

to sell and value in use. An impairment loss is recognised in other

operating expenses if the carrying amount exceeds the recoverable

amount. If there is an impairment loss for a cash-generating unit, first

the carrying amount of any goodwill allocated to the cash-generating

unit is reduced, and subsequently the other non-current assets of the

unit are reduced pro rata on the basis of the carrying amount of each

asset in the unit.

Irrespective of whether there is an impairment indication, intan-

gible assets with an indefinite useful life and goodwill acquired in

business combinations are tested annually for impairment.

An impairment loss recognised in goodwill is not reversible. With

respect to all other impaired assets, an impairment loss recognised

in prior periods is reversed affecting the income statement if there

has been a change in the estimates used to determine the recoverable

amount. An impairment loss is reversed only to the extent that the

asset’s carrying amount does not exceed the carrying amount that

would have been determined (net of depreciation or amortisation) if

no impairment loss had been recognised.

Leases

Under finance lease arrangements, the substantial risks and rewards

associated with an asset are transferred to the lessee. At the beginning

of the lease arrangement, the respective asset and a corresponding

liability are recognised at the fair value of the asset or, if lower, the

net present value of the minimum lease payments. For subsequent

measurement, minimum lease payments are apportioned between

the finance expense and the reduction of the outstanding liability. The

finance expense is allocated to each period during the lease term so as

to produce a constant periodic interest rate on the remaining balance

of the liability. In addition, depreciation and any impairment losses for

the associated assets are recognised. Depreciation is performed over

the lease term or, if shorter, over the useful life of the asset.

Under operating lease agreements, rent expenses are recognised

on a straight-line basis over the term of the lease.